Exam 5: Interest Rate Risk Measurement: The Repricing Model

Exam 1: Why Are Financial Institutions Special68 Questions

Exam 2: The Financial Service Industry: Depository Institutions78 Questions

Exam 3: The Financial Service Industry: Other Financial Institutions68 Questions

Exam 4: Risks of Financial Institutions76 Questions

Exam 5: Interest Rate Risk Measurement: The Repricing Model78 Questions

Exam 6: Interest Rate Risk Measurement: the Duration Model73 Questions

Exam 7: Managing Interest Rate Risk Using Off-Balance-Sheet Instruments75 Questions

Exam 8: Managing Interest Rate Risk Using Securitisation75 Questions

Exam 9: Market Risk61 Questions

Exam 10: Credit Risk I: Individual Loan Risk75 Questions

Exam 11: Credit Risk II: Loan Portfolio and Concentration Risk76 Questions

Exam 12: Sovereign Risk76 Questions

Exam 13: Foreign Exchange Risk77 Questions

Exam 14: Liquidity Risk76 Questions

Exam 15: Liability and Liquidity Management77 Questions

Exam 16: Off-Balance-Sheet Activities75 Questions

Exam 17: Technology and Other Operational Risks77 Questions

Exam 18: Capital Management and Adequacy76 Questions

Select questions type

The cumulative repricing gap position of an FI for a given extended time period is the sum of the repricing gap values for the individual time periods that make up the extended time period.

(True/False)

4.9/5  (35)

(35)

If the spread between rate-sensitive assets and rate-sensitive liabilities increases for a bank, future changes in interest rates will lead to an increase in net interest income.

(True/False)

4.9/5 (30)

Consider the following repricing buckets and gaps: Repricing bucket Assets Liabilities Gaps 1 day \ 50000 \ 120000 -\ 70000 1 day to 3 months \ 100000 \ 70000 \ 30000 3 to 6 months \ 100000 \ 100000 \ 0 6 to 12 months \ 250000 \ 80000 \ 170000 1 to 5 years \ 75000 \ 130000 -\ 55000 Over 5 years \ 25000 \ 100000 -\ 75000 What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is an increase of 100 basis points?

(Multiple Choice)

4.8/5 (44)

Outline what is meant by the CGAP effect and explain the relationship between interest rate changes and changes in net interest income.Specifically, indicate whether a FI would wish to hold a negative or positive CGAP and under which interest rate conditions.

(Essay)

4.8/5 (25)

Consider the following information to answer the question: Assets Amount Rate Liabilities Amount Rate Rate \ 35000000 10\% Rate \ 40000000 8\% Sensitive Sensitive Fixed rate \ 21000000 9\% Fixed rate \ 12000000 7\% Non-earning \ 4000000 Equity \ 8000000 What will be the FI's net interest income at year-end if interest rates do not change?

(Multiple Choice)

4.8/5 (35)

Convexity is the major problem associated with the repricing gap.

(True/False)

4.9/5 (36)

The cumulative gap over the whole balance sheet by definition:

(Multiple Choice)

4.9/5 (37)

An FI with a neutral repricing gap in its three to six month bucket is hedged against any interest rate changes at all points in time.

(True/False)

4.8/5 (45)

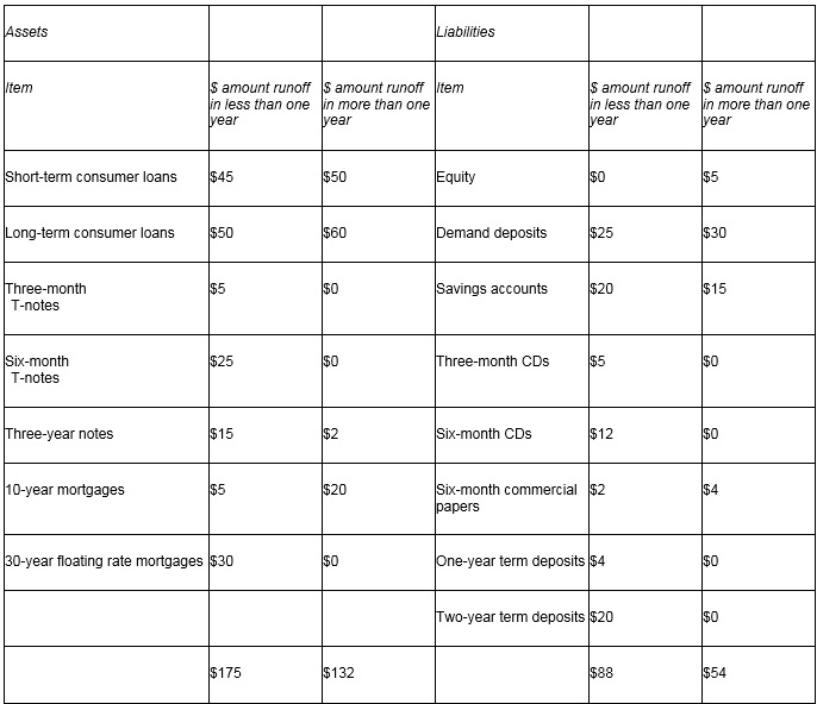

Consider the following table:  What is the one-year gap adjusted for runoffs?

What is the one-year gap adjusted for runoffs?

(Multiple Choice)

4.8/5 (43)

How do you interpret the position of an FI with a positive on-balance-sheet gap and a negative off-balance sheet gap?

(Multiple Choice)

4.7/5 (46)

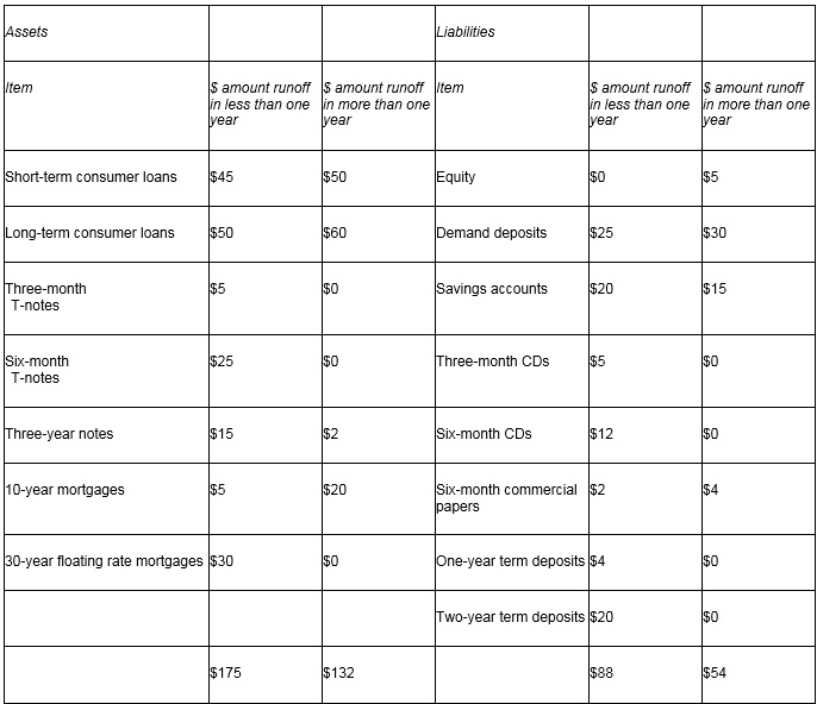

Consider the following table:  How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

How does a decrease in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

(Multiple Choice)

4.8/5 (43)

Interest rate spread is the difference between the earning assets interest rate and cash rate set by RBA.

(True/False)

4.9/5 (30)

In the last quarter ABC Bank reported the following repricing buckets: Repricing buckets Assets Liabilities 1 day \ 50 \ 100 1 day to 3 months \ 120 \ 25 3 months to 6 months \ 35 \ 100 6 months to 12 months \ 65 \ 75 1 year to 5 years \ 70 \ 40 Over 5 years \ 60 \ 60 Calculate the repricing gaps for each maturity bucket and the cumulative gaps

(Essay)

4.7/5 (33)

An FI with a negative gap of $20 million suffers a $0.2 million decrease in its net interest income if interest rates decrease by 1 per cent.

(True/False)

4.8/5 (45)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)