Exam 5: Interest Rate Risk Measurement: The Repricing Model

Exam 1: Why Are Financial Institutions Special68 Questions

Exam 2: The Financial Service Industry: Depository Institutions78 Questions

Exam 3: The Financial Service Industry: Other Financial Institutions68 Questions

Exam 4: Risks of Financial Institutions76 Questions

Exam 5: Interest Rate Risk Measurement: The Repricing Model78 Questions

Exam 6: Interest Rate Risk Measurement: the Duration Model73 Questions

Exam 7: Managing Interest Rate Risk Using Off-Balance-Sheet Instruments75 Questions

Exam 8: Managing Interest Rate Risk Using Securitisation75 Questions

Exam 9: Market Risk61 Questions

Exam 10: Credit Risk I: Individual Loan Risk75 Questions

Exam 11: Credit Risk II: Loan Portfolio and Concentration Risk76 Questions

Exam 12: Sovereign Risk76 Questions

Exam 13: Foreign Exchange Risk77 Questions

Exam 14: Liquidity Risk76 Questions

Exam 15: Liability and Liquidity Management77 Questions

Exam 16: Off-Balance-Sheet Activities75 Questions

Exam 17: Technology and Other Operational Risks77 Questions

Exam 18: Capital Management and Adequacy76 Questions

Select questions type

Which of the following is not a weakness of the repricing model to measure interest rate risk?

(Multiple Choice)

4.8/5  (47)

(47)

The liquidity premium theory of the term structure of interest rates:

(Multiple Choice)

4.7/5 (34)

An FI with a positive repricing gap expects interest rates to decrease.

(True/False)

4.8/5 (34)

Consider the following repricing buckets and gaps: Repricing bucket Assets Liabilities Gaps 1 day \ 50000 \ 120000 -\ 70000 1 day to 3 months \ 100000 \ 70000 \ 30000 3 to 6 months \ 100000 \ 100000 \ 0 6 to 12 months \ 250000 \ 80000 \ 170000 1 to 5 years \ 75000 \ 130000 -\ 55000 Over 5 years \ 25000 \ 100000 -\ 75000 What is the annualised change in the bank's future net interest income if the average rate change for assets and liabilities that can be repriced within one year is a decrease of 100 basis points?

(Multiple Choice)

4.8/5 (37)

Spread effect is periodic cash flow of interest and principal amortisation payments on long-term assets that can be reinvested at market rates.

(True/False)

4.9/5 (36)

Interest rate spread is the difference between the earning assets interest rate and the interest rate paid on interest-bearing liability.

(True/False)

4.7/5 (37)

What is meant by the 'runoff' problem and how can bank managers deal with this problem?

(Essay)

4.8/5 (41)

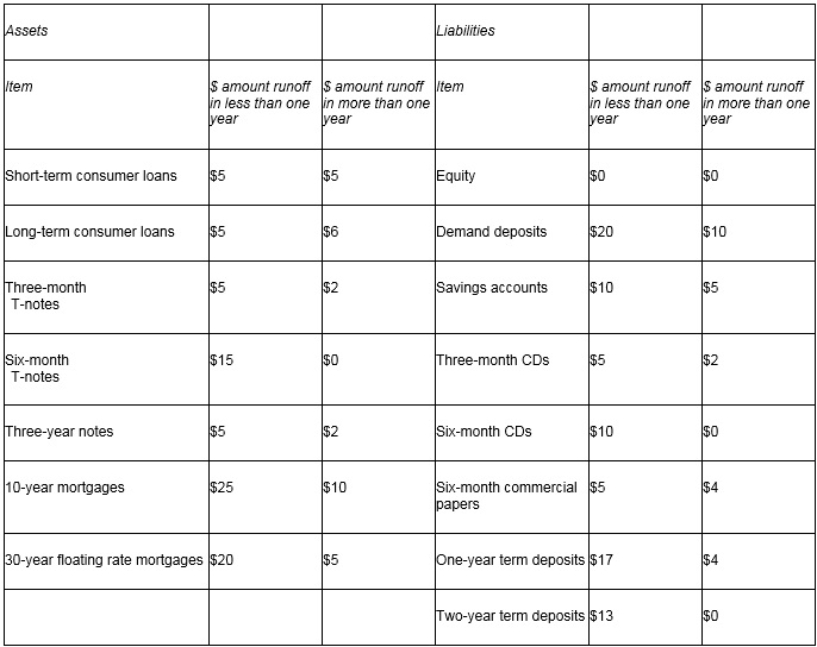

Consider the following table:  How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

How does an increase in the average one-year interest rate of 50 basis points affect the FI's future net interest income?

(Multiple Choice)

4.9/5 (38)

The bank has a positive repricing gap.Is it exposed to interest rate increases or decreases and why?

(Multiple Choice)

4.9/5 (41)

Which of the following is a weakness of the repricing model to measure interest rate risk?

(Multiple Choice)

5.0/5 (36)

Consider the following repricing buckets and gaps: Repricing bucket Assets Liabilities Gaps 1 day \ 50000 \ 120000 -\ 70000 1 day to 3 months \ 100000 \ 70000 \ 30000 3 to 6 months \ 100000 \ 100000 \ 0 6 to 12 months \ 250000 \ 80000 \ 170000 1 to 5 years \ 75000 \ 130000 -\ 55000 Over 5 years \ 25000 \ 100000 -\ 75000 What is the annualised change in the bank's future net interest income if the overnight interest rate decreased by 100 basis points?

(Multiple Choice)

4.8/5 (33)

CGAP effect is the relationship between changes in interest rates and changes in net interest income.

(True/False)

4.9/5 (43)

Consider the following repricing buckets and gaps: Repricing bucket Assets Liabilities Gaps 1 day \ 50000 \ 120000 -\ 70000 1 day to 3 months \ 100000 \ 70000 \ 30000 3 to 6 months \ 100000 \ 100000 \ 0 6 to 12 months \ 250000 \ 80000 \ 170000 1 to 5 years \ 75000 \ 130000 -\ 55000 Over 5 years \ 25000 \ 100000 -\ 75000 What is the annualised change in the bank's future net interest income if the overnight interest rate increased by 100 basis points?

(Multiple Choice)

4.8/5 (44)

How do you interpret the position of an FI with a negative on-balance-sheet gap and a positive off-balance-sheet gap?

(Multiple Choice)

4.9/5 (46)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)