Exam 12: Intangible Assets and Goodwill

Criteria for capitalization of development costs

List the criteria that must be met before development costs of a project may be capitalized.

The six criteria that must be met are:

1. Technical feasibility of completing the intangible asset,

2. The entity's intention to complete it for use or sale,

3. The entity's ability to use or sell it,

4. Availability of technical, financial, and other resources needed to complete, use or sell it,

5. The way in which the future economic benefits will be received; including the existence of a market for the asset if it will be sold, or its usefulness to the entity if it will be used internally,

6. The ability to reliably measure the costs associated with and attributed to the intangible asset during its development.

Alternative treatments of goodwill after recognition

Once goodwill has been recognized in the accounts, there has been much disagreement over how it should be treated in subsequent periods. Discuss the alternative treatment approaches.

1. Charge goodwill off immediately to shareholders' equity. Goodwill is not an asset that is separable from the business itself and therefore should not be recognized as a separate asset. In addition, immediate expensing would be consistent with the expensing of costs of internally generated goodwill. As well, there is no rational method to amortize goodwill, due to the many uncertainties involved; therefore, financial statements will be more reliable if it is expensed.

2. Amortize goodwill over its useful life. Goodwill at the time of purchase erodes in value over time and therefore it should be charged to income over the estimated period in which it is expected to benefit the business.

3. Retain goodwill indefinitely at cost (i.e., do not amortize), unless impairment occurs. Current and future expenses help to maintain existing goodwill; therefore, it can have an indefinite life. Amortization of goodwill is entirely arbitrary and leads to distortions of net income.

Which of the following is NOT generally true of intangible assets and goodwill?

B

Cayman Corp. incurred $ 140,000 of basic research and $ 35,000 of development costs to develop a product for which a patent was granted on January 2, 2015. Legal fees and other costs associated with registration of the patent totalled $ 50,000. On March 31, 2020, Cayman paid $ 75,000 for legal fees in a successful defence of the patent. The total amount capitalized for the patent through March 31, 2020 should be

The steps involved in testing goodwill for impairment using ASPE do NOT include

Calculation of goodwill

Great Corporation is interested in purchasing Big World Company Ltd. The total of Big World's net income amounts over the past five years is $ 745,000. During one of those years, Big World reported a gain on discontinued operations of $ 93,000. The fair value of Big World's net identifiable assets is $ 684,000. A normal rate of return is 14%, and Great Corporation wants to capitalize excess earnings at 19%.

Instructions

Calculate the estimated value of goodwill.

The proper accounting for the costs incurred in creating computer software products that are to be sold, leased, or otherwise marketed to external parties, is to

On January 2, 2017, Albion Corp. purchased a patent for a new consumer product for $ 45,000. At the time of purchase, the patent was valid for 15 years. Due to the competitive nature of the product, however, the patent was estimated to have a useful life of only ten years. During 2020, the product was permanently removed from the market because of a potential health hazard. What amount should Albion recognize as an impairment loss for calendar 2020, assuming amortization has been recorded annually using the straight-line method with no residual value?

Intangible assets that have a finite life are amortized over a period NOT to exceed

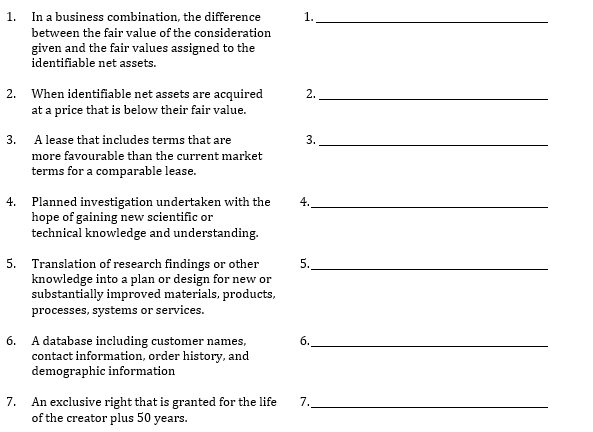

Terminology

In the space provided at right, write the word or phrase that is defined or indicated.

If a company constructs a laboratory building to be used as a research and development facility, the cost of the laboratory building is matched against earnings as

Calculating goodwill

Explain how the amount to be recognized as goodwill can be calculated. Can goodwill be sold? If so, how? Explain.

Capitalization versus expensing intangible-related costs

Identify whether the following costs would be expensed (E) or capitalized (C):

___ Lawyer fees related to the successful defence of a patent

___ Routine website maintenance

___ Costs incurred to register a company's name and trademark

___ Interest or borrowing costs related to an internally generated intangible

___ Lawyer fees related to the unsuccessful defence of a patent

Carrying value of patent

On July 1, 2017, Dominica Corp. purchased a patent from Surama Ltd. for $ 60,000. On July 1, 2020, Dominica paid $ 12,000 for successful litigation in defence of the patent. Dominica estimates that the useful life of the patent will be 15 years from the date of acquisition.

Prepare a calculation of the carrying value of the patent at December 31, 2020. Label all calculations.

Definitions

Provide clear, concise answers for the following:

1. What are intangible assets?

2. How are research costs accounted for?

3. How are development costs accounted for?

4. What are the two models that are used to measure intangible assets after initial acquisition?

5. What are the factors that should be considered when determining the useful life of limited-life intangible assets?

6. What are the major categories of intangible assets?

7. What are the two models that are used to account for the impairment of intangible assets?

Similar to impairment models and standards that apply to long-lived tangible assets, the rational entity impairment model applies also to

Goodwill is the excess of the purchase price of the acquired enterprise over the

The cost of purchasing patent rights for a product that might otherwise have seriously competed with one of the purchaser's patented products should be

Which of the following explains the rationale for using "normalized" earnings under the excess-earnings valuation approach?

During 2020, Elysium Inc. incurred the following costs: Researeh Expense...................................................................................$360,000

Routine design of tools, jigs, moulds, and dies......................................

Modification of the formulation of a process...........................................610,000

Development services performed by Orchard Corp. for Elysium .......... Assuming the 6 specific conditions have been demonstrated, in 2020, Elysium Corp. would report development costs of

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)