Exam 5: Intercompany Profit Transactions - Inventories

Exam 1: Business Combinations46 Questions

Exam 2: Stock Investments - Investor Accounting and Reporting51 Questions

Exam 3: An Introduction to Consolidated Financial Statements50 Questions

Exam 4: Consolidated Techniques and Procedures50 Questions

Exam 5: Intercompany Profit Transactions - Inventories50 Questions

Exam 6: Intercompany Profit Transactions - Plant Assets50 Questions

Exam 7: Intercompany Profit Transactions - Bonds50 Questions

Exam 8: Consolidations - Changes in Ownership Interests50 Questions

Exam 9: Indirect and Mutual Holdings50 Questions

Exam 10: Subsidiary Preferred Stock, consolidated Earnings Per Share, and Consolidated Income Taxation50 Questions

Exam 11: Consolidation Theories, push-Down Accounting, and Corporate Joint Ventures55 Questions

Exam 12: Derivatives and Foreign Currency: Concepts and Common Transactions50 Questions

Exam 13: Accounting for Derivatives and Hedging Activities50 Questions

Exam 14: Foreign Currency Financial Statements50 Questions

Exam 15: Segment and Interim Financial Reporting50 Questions

Exam 16: Partnerships - Formation,operations,and Changes in Ownership Interests50 Questions

Exam 17: Partnership Liquidation50 Questions

Exam 18: Corporate Liquidations and Reorganizations50 Questions

Exam 19: An Introduction to Accounting for State and Local Governmental Units50 Questions

Exam 20: Accounting for State and Local Governmental Units - Governmental Funds48 Questions

Exam 21: Accounting for State and Local Governmental Units - Proprietary and Fiduciary Funds50 Questions

Exam 22: Accounting for Not-For-Profit Organizations50 Questions

Exam 23: Estates and Trusts50 Questions

Select questions type

Swamp Co.,a 55%-owned subsidiary of Pond Inc.,made the following entry to record a sale of merchandise to Pond:  All Swamp sales are at 125% of cost.One-fourth of this merchandise remained in the Pond's inventory at year-end.A working paper entry to eliminate unrealized profits from consolidated inventory would include a credit to Inventory in the amount of

All Swamp sales are at 125% of cost.One-fourth of this merchandise remained in the Pond's inventory at year-end.A working paper entry to eliminate unrealized profits from consolidated inventory would include a credit to Inventory in the amount of

(Multiple Choice)

4.8/5  (39)

(39)

A subsidiary's realized income is its reported net income adjusted for intercompany profits from upstream sales.

(True/False)

4.9/5 (30)

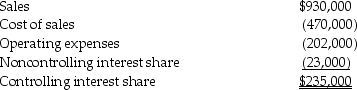

Pastern Industries has an 80% ownership stake in Sascon Incorporated.At the time of purchase,the book value of Sascon's assets and liabilities were equal to the fair value.The cost of the 80% investment was equal to 80% of the book value of Sascon's net assets.At the end of 2014,they issued the following consolidated income statement:

Shortly after the statements were issued,Pastern discovered that the 2014 intercompany sales transactions had not been properly eliminated in consolidation.In fact,Pastern had sold inventory that cost $80,000 to Sascon for $90,000,and Sascon had sold inventory that cost $50,000 to Pastern for $65,000.Half of the products from both transactions still remained in inventory at December 31,2014.

Required: Prepare a corrected income statement for Pastern and Subsidiary for 2014.

Shortly after the statements were issued,Pastern discovered that the 2014 intercompany sales transactions had not been properly eliminated in consolidation.In fact,Pastern had sold inventory that cost $80,000 to Sascon for $90,000,and Sascon had sold inventory that cost $50,000 to Pastern for $65,000.Half of the products from both transactions still remained in inventory at December 31,2014.

Required: Prepare a corrected income statement for Pastern and Subsidiary for 2014.

(Essay)

4.8/5 (30)

Salli Corporation regularly purchases merchandise from their 90% owner,Playtime Corporation.Playtime purchased the 90% interest at a cost equal to 90% of the book value of Salli's net assets.At the time of acquisition,the book values and fair values of Salli's assets and liabilities were equal.Playtime makes their sales to Salli at 120% of cost.In 2014,Salli reported net income of $460,000,and made purchases totaling $172,000 from Playtime.Although Salli had no inventory on hand at the beginning of 2014 that they had purchased from Playtime,at year end,they had $51,600 of this merchandise in inventory.

Required:

1.Determine the unrealized profit in Salli's inventory at December 31,2014.

2.Compute Playtime's income from Salli for 2014.

(Essay)

4.7/5 (39)

Use the following information to answer the question(s) below.

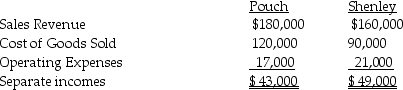

Pouch Corporation acquired an 80% interest in Shenley Corporation on January 1, 2014, when the book values of Shenley's assets and liabilities were equal to their fair values. The cost of the 80% interest was equal to 80% of the book value of Shenley's net assets. During 2014, Pouch sold merchandise that cost $70,000 to Shenley for $86,000. On December 31, 2014, three-fourths of the merchandise acquired from Pouch remained in Shenley's inventory. Separate incomes (investment income not included) of the two companies are as follows:

-What is Pouch's income from Shenley for 2014?

-What is Pouch's income from Shenley for 2014?

(Multiple Choice)

4.9/5 (31)

Shalles Corporation,an 80%-owned subsidiary of Pani Corporation,sold inventory items to its parent at a $48,000 profit in 2014.Pani resold one-third of this inventory to outside entities.Shalles reported net income of $200,000 for 2014.Noncontrolling interest share of consolidated net income that will appear in the income statement for 2014 is

(Multiple Choice)

4.8/5 (29)

Revenue is recognized when it is earned; therefore revenue earned for a consolidated entity occurs when there is a sale to outside entities.

(True/False)

4.7/5 (37)

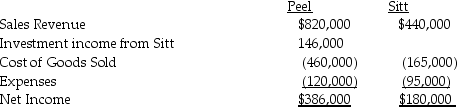

Peel Corporation acquired an 80% interest in Sitt Corporation at a cost equal to 80% of the book value of Sitt several years ago.At the time of purchase,the fair value and book value of Sitt's assets and liabilities were equal.Sitt purchases its entire inventory from Peel at 150% of Peel's cost.During 2014,Peel sold $190,000 of merchandise to Sitt.Sitt's beginning and ending inventories for 2014 were $72,000 and $66,000,respectively.Income statement information for both companies for 2014 is as follows:

Required:

Prepare a consolidated income statement for Peel Corporation and Subsidiary for 2014.

Required:

Prepare a consolidated income statement for Peel Corporation and Subsidiary for 2014.

(Essay)

4.9/5 (47)

Parent sales to its subsidiary increase parent sales,COGS and gross profit.

(True/False)

4.9/5 (30)

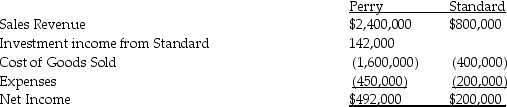

Perry Instruments International purchased 75% of the outstanding common stock of Standard Systems in 1997 when the book values and fair values of Standard's assets and liabilities were equal.The cost of Perry's investment was equal to 75% of the book value of Standard's net assets.Separate company income statements for Perry and Standard for the year ended December 31,2014 are summarized as follows:

During 2014,the companies began to manage their inventory differently,and worked together to keep their inventories low at each location.In doing so,they agreed to sell inventory to each other as needed at a markup of 10% of cost.Perry sold merchandise that cost $100,000 to Standard for $110,000,and Standard sold inventory that cost $80,000 to Perry for $88,000.Half of this merchandise remained in each company's inventory at December 31,2014.

Required:

Prepare a consolidated income statement for Perry Corporation and Subsidiary for 2014.

During 2014,the companies began to manage their inventory differently,and worked together to keep their inventories low at each location.In doing so,they agreed to sell inventory to each other as needed at a markup of 10% of cost.Perry sold merchandise that cost $100,000 to Standard for $110,000,and Standard sold inventory that cost $80,000 to Perry for $88,000.Half of this merchandise remained in each company's inventory at December 31,2014.

Required:

Prepare a consolidated income statement for Perry Corporation and Subsidiary for 2014.

(Essay)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)