Exam 20: Inventory Management, Just-In-Time, and Simplified Costing Methods

Exam 1: The Accountants Role in the Organization195 Questions

Exam 2: An Introduction to Cost Terms and Purposes224 Questions

Exam 3: Cost-Volume-Profit Analysis207 Questions

Exam 4: Job Costing199 Questions

Exam 5: Activity-Based Costing and Activity-Based Management175 Questions

Exam 6: Master Budget and Responsibility Accounting229 Questions

Exam 7: Flexible Budgets, Direct-Cost Variances, and Management Control180 Questions

Exam 8: Flexible Budgets, Overhead Cost Variances, and Management Control171 Questions

Exam 9: Inventory Costing and Capacity Analysis208 Questions

Exam 10: Determining How Costs Behave182 Questions

Exam 11: Decision Making and Relevant Information220 Questions

Exam 12: Pricing Decisions and Cost Management210 Questions

Exam 13: Strategy, Balanced Scorecard, and Strategic Profitability Analysis171 Questions

Exam 14: Cost Allocation, Customer-Profitability Analysis, and Sales-Variance Analysis170 Questions

Exam 15: Allocation of Support-Department Costs, Common Costs, and Revenues144 Questions

Exam 16: Cost Allocation: Joint Products and Byproducts125 Questions

Exam 17: Process Costing126 Questions

Exam 18: Spoilage, Rework, and Scrap125 Questions

Exam 19: Balanced Scorecard: Quality, Time, and the Theory of Constraints124 Questions

Exam 20: Inventory Management, Just-In-Time, and Simplified Costing Methods125 Questions

Exam 21: Capital Budgeting and Cost Analysis130 Questions

Exam 22: Management Control Systems, Transfer Pricing, and Multinational Considerations123 Questions

Exam 23: Performance Measurement, Compensation, and Multinational Considerations139 Questions

Select questions type

Lean accounting is a costing method that supports creating value for the customer by costing the entire value stream, NOT individual products or departments, thereby eliminating waste in the accounting process.

(True/False)

5.0/5  (38)

(38)

In a backflush-costing system, no record of work in process appears in the accounting records.

(True/False)

4.9/5 (36)

A trigger point refers to the inventory level at which a reorder is generated.

(True/False)

4.8/5 (40)

The time required to get equipment, tools, and materials ready to start production is referred to as:

(Multiple Choice)

4.7/5 (42)

Relevant opportunity cost of capital is the return forgone by investing capital in inventory rather than elsewhere.

(True/False)

4.9/5 (36)

The simplest version of the Economic Order Quantity model incorporates only ordering costs, carrying costs, and purchasing costs into the calculation.

(True/False)

4.8/5 (41)

The costs that result when features and characteristics of a product or service are NOT in conformance with the specifications are:

(Multiple Choice)

4.9/5 (34)

Answer the following questions using the information below:

The following information applies to Labs Plus, which supplies microscopes to laboratories throughout the country. Labs Plus purchases the microscopes from a manufacturer which has a reputation for very high quality in its manufacturing operation.

-What is the reorder point?

-What is the reorder point?

(Multiple Choice)

4.8/5 (32)

The costs that result when a company runs out of a particular item for which there is a customer demand are:

(Multiple Choice)

4.9/5 (39)

The "flush" in backflush refers to the fact that there are no variances in a backflush costing system using standard costs.

(True/False)

4.9/5 (37)

Just-in-time purchasing is guided solely by the economic order quantity.

(True/False)

4.8/5 (40)

A system that comprises a single database that collects data and feeds it into software applications supporting all of a company's business activities is known as a(n):

(Multiple Choice)

4.9/5 (41)

Costs of setting up a production run are analogous to ordering costs in the Economic Order Quantity (EOQ)model.

(True/False)

4.9/5 (26)

Answer the following questions using the information below:

The following information applies to Labs Plus, which supplies microscopes to laboratories throughout the country. Labs Plus purchases the microscopes from a manufacturer which has a reputation for very high quality in its manufacturing operation.

-What is the economic order quantity assuming each order was made at the economic-order-quantity amount?

-What is the economic order quantity assuming each order was made at the economic-order-quantity amount?

(Multiple Choice)

4.8/5 (29)

All inventory costs are available in financial accounting systems.

(True/False)

4.9/5 (38)

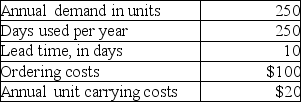

For supply item ABC, Andrews Company has been ordering 125 units based on the recommendation of the salesperson who calls on the company monthly. A new purchasing agent has been hired by the company who wants to start using the economic-order-quantity method and its supporting decision elements. She has gathered the following information:

Required:

Determine the EOQ, average inventory, orders per year, average daily demand, reorder point, annual ordering costs, and annual carrying costs.

Required:

Determine the EOQ, average inventory, orders per year, average daily demand, reorder point, annual ordering costs, and annual carrying costs.

(Essay)

4.8/5 (47)

Answer the following questions using the information below:

Owen-King Company sells optical equipment. Lens Company manufactures special glass lenses. Owen-King Company orders 5,200 lenses per year, 100 per week, at $20 per lens. Lens Company covers all shipping costs. Owen-King Company earns 30% on its cash investments. The purchase-order lead time is 2.5 weeks. Owen-King Company sells 125 lenses per week. The following data are available:

-What is the reorder point?

-What is the reorder point?

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)