Exam 21: Accounting for State and Local Governmental Units - Proprietary and Fiduciary Funds

Exam 1: Business Combinations36 Questions

Exam 2: Stock Investments - Investor Accounting and Reporting41 Questions

Exam 3: An Introduction to Consolidated Financial Statements39 Questions

Exam 4: Consolidated Techniques and Procedures38 Questions

Exam 5: Intercompany Profit Transactions Inventories40 Questions

Exam 6: Intercompany Profit Transactions Plant Assets39 Questions

Exam 7: Intercompany Profit Transactions Bonds40 Questions

Exam 8: Consolidations - Changes in Ownership Interests37 Questions

Exam 9: Indirect and Mutual Holdings37 Questions

Exam 10: Subsidiary Preferred Stock, Consolidated Earnings Per Share, and Consolidated Income Taxation36 Questions

Exam 11: Consolidation Theories, Push-Down Accounting, and Corporate Joint Ventures41 Questions

Exam 12: Derivatives and Foreign Currency: Concepts and Common Transactions40 Questions

Exam 13: Accounting for Derivatives and Hedging Activities40 Questions

Exam 14: Foreign Currency Financial Statements39 Questions

Exam 15: Segment and Interim Financial Reporting40 Questions

Exam 16: Partnerships - Formation, Operations, and Changes in Ownership Interests40 Questions

Exam 17: Partnership Liquidation40 Questions

Exam 18: Corporate Liquidations and Reorganizations40 Questions

Exam 19: An Introduction to Accounting for State and Local Governmental Units38 Questions

Exam 20: Accounting for State and Local Governmental Units - Governmental Funds37 Questions

Exam 21: Accounting for State and Local Governmental Units - Proprietary and Fiduciary Funds39 Questions

Exam 22: Accounting for Not-For-Profit Organizations39 Questions

Exam 23: Estates and Trusts38 Questions

Select questions type

A trust fund was created to assist local students in financial need. The following transactions occurred in the trust.

1. The committee forming the fund was able to raise $700,000 and invested the funds so that the principal would remain indefinitely, and the earnings would be used to aid needy students.

2. During the year, the fund earned $65,000 interest. Earnings remain invested in the trust until withdrawn to distribute, so the interest was invested.

3. $50,000 of the investments were sold, withdrawn, and distributed to provide scholarships.

4. The fund-raising committee contributed an additional $200,000 cash to the fund. This cash was deposited into the account and invested.

5. Interest earned but not yet deposited into the investment account was accrued at $17,000.

Required:

Prepare the necessary journal entries for each of the above transactions for the trust fund.

Free

(Essay)

4.8/5  (45)

(45)

Correct Answer: Verified

Verified

Enterprise funds are accounted for in a manner similar to

Free

(Multiple Choice)

4.8/5 (39)

Correct Answer:Verified

A

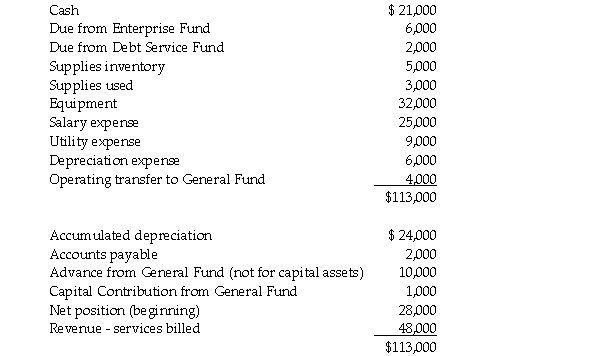

An adjusted trial balance is provided below for the Dade County copy services department at June 30, 2014.

Required:

1. Prepare a statement of revenues, expenses and changes in net position for the copy services department for the year ended June 30, 2014.

2. Prepare a statement of net position for the copy services department at June 30, 2014. Assume all assets are not externally or internally restricted.

Required:

1. Prepare a statement of revenues, expenses and changes in net position for the copy services department for the year ended June 30, 2014.

2. Prepare a statement of net position for the copy services department at June 30, 2014. Assume all assets are not externally or internally restricted.

Free

(Essay)

4.9/5 (45)

Correct Answer:Verified

The City of Sill established an Internal Service Fund to provide cleaning services to all city offices and departments. The following transactions took place with respect to this event.

1. The General Fund contributed cash of $49,000 to the Internal Service Fund. The General Fund provided a $10,000 loan to the Internal Service Fund.

2. On January 1, 2014, the Internal Service Fund acquired a floor waxing machine for cash of $5,000. It has a 5 year life with no salvage value, and the city uses straight-line depreciation on their assets.

3. The cleaning services department billed other government agencies and departments $226,000 and collected $187,000.

4. The cleaning services department incurred and paid the following expenses: cleaning personnel wages, $65,000; payroll taxes, $10,000; cleaning supplies, $13,000; and office rental and utilities, $77,000. The cleaning services department also repaid the general fund for the loan.

5. The cleaning services department prepared the journal entry to depreciate their assets for the year ending December 31, 2014.

Required:

Prepare the necessary journal entries for each of the above transactions for the Internal Service Fund.

(Essay)

4.9/5 (40)

Thoroughgood County has a municipal golf course and tennis club which is funded by the membership fees it charges. The club also has 6% bonds outstanding amounting to $20,000,000 on which it pays interest semi-annually. The club had the following transactions.

1. An addition to the golf clubhouse was added for $2,000,000, funded out of operations.

2. The following expenses were incurred and paid: $80,000 wages; $10,000 payroll taxes; $45,000 water bill; and $12,000 equipment repair.

3. Interest on the bonds was paid amounting to $600,000.

4. $5,000,000 of operating cash excess was repaid to the general fund for a previous loan.

5. Depreciation of $500,000 was recorded for the buildings.

Required:

Prepare the necessary journal entries for each of the above transactions for the Enterprise Fund.

(Essay)

4.8/5 (32)

GASB requires ________ method(s) for the cash flow statement for proprietary funds.

(Multiple Choice)

4.8/5 (35)

The City's municipal golf course had the following transactions.

1. Received a beautification(operating) grant from the state for $600,000. Received cash of $600,000.

2. Incurred and paid qualifying expenses under the state grant program in (1) above of $280,000.

3. Incurred and paid construction costs on an uncompleted clubhouse for $1,200,000.

4. Received $1,000,000 cash from a grant to assist with construction costs for the clubhouse.

Required:

Given that the golf course is operated based on user fees for upkeep, prepare the necessary journal entries for each of these transactions.

(Essay)

4.8/5 (44)

Journalize the following municipal zoo transactions in the Lackluster County Enterprise Fund:

1. The zoo issued $1,000,000 of 5% revenue bonds at 99 on July 1, 2014 (an interest payment date). The bond proceeds are to be used for a new polar bear exhibit and the issue will mature in 20 years. Interest is paid on January 1 and July 1.

2. Depreciation for the year-ended December 31, 2014 included $175,000 for buildings and $105,000 for outdoor exhibit areas.

3. The zoo paid $800,000 in construction costs for the new exhibit. The exhibit is still under construction.

4. Interest on the revenue bonds was accrued at year-end, December 31, 2014. Straight-line amortization is used for bond discounts and premiums.

(Essay)

4.8/5 (36)

The fixed assets and long-term liabilities associated with Proprietary Funds are reported on the

(Multiple Choice)

4.9/5 (28)

Prepare journal entries in an Internal Service Fund of Union County to record each of the following transactions.

1. Purchased equipment on September 1, 2014 by paying $25,000 down and borrowing $100,000 on a 6%, 2-year note.

2. In 2014, billed General Fund $620,000 for services provided. Billings to the Enterprise Fund totaled $165,000. All billings were collected by December 31, 2014 except for $100,000 charged to the General Fund.

3. Accrued year-end adjustments at December 31, 2014 for interest expense and depreciation. The useful life of the equipment is 5 years with no salvage value.

(Essay)

4.9/5 (35)

Journalize the following utility transactions in the Quest County Enterprise Fund:

1. Billings to external customers $1,600,000; billings to Quest County governmental funds $130,000.

2. Collected refundable deposits from new customers $10,000.

3. Collected 95% of all billings by fiscal year-end.

4. Refunded $4,000 in deposits to former customers.

5. Unbilled services to outside customers at year-end $14,000.

(Essay)

4.7/5 (38)

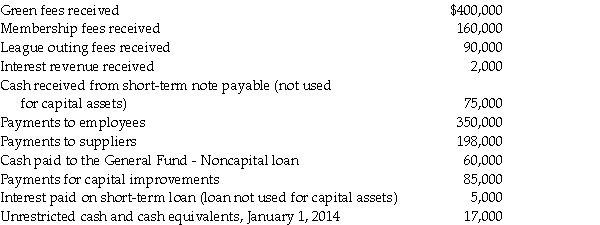

Based upon the cash flow information provided below for the year ended December 31, 2014, prepare a cash flow statement for the Bloomfield Municipal Golf Course, an enterprise fund.

(Essay)

4.8/5 (49)

Proprietary funds are required to prepare financial statements that include:

A. Statement of Activities

B. Statement of Revenues, Expenditures and Changes in Fund Balance

C. Balance Sheet

D. Statement of Cash Flows

E. Statement of Net Position

F. Statement of Revenues, Expenses and Changes in Net Position

(Multiple Choice)

4.8/5 (37)

The four cash flow categories required in an Enterprise Fund's Statement of Cash Flows are listed below and assigned a letter code.

A) Cash flows from operating activities

B) Cash flows from noncapital financing activities

C) Cash flows from capital and related financing activities

D) Cash flows from investing activities

Required:

Use the correct letter code to indicate where each of the following ten items associated with an Enterprise Fund should be reported in the Statement of Cash Flows.

1. An enterprise fund's fixed asset was sold for cash.

2. Cash paid to suppliers for goods.

3. Paid principal, $100,000, and interest, $5,000, on a mortgage.

4. Cash proceeds from sale of investments, $65,000.

5. Cash paid for new equipment, $18,000.

6. Cash received from the general fund; restricted to cover part of the cost of plant expansion, $900,000.

7. Cash received from another fund as a 6-month loan for the sole purpose of financing purchase of equipment, $47,000.

8. Cash proceeds from issuing bonds for an enterprise fund's construction project.

9. Cash paid to employees for salaries.

10. Cash received from interest earned on investments.

(Essay)

4.9/5 (33)

What is a significant difference for agency funds when compared to governmental funds?

(Multiple Choice)

4.8/5 (37)

An enterprise fund collects $100,000 cash for customer deposits to insure timely payment for services. What journal entry did the enterprise fund prepare?

(Multiple Choice)

4.7/5 (35)

The financial statements of proprietary funds are similar to business enterprises with the exception that proprietary funds do not

(Multiple Choice)

4.8/5 (37)

The following transactions relate to a municipal golf course and tennis club, financed with debt secured by membership fees.

1. The General Fund loaned $25,000,000 cash to the Enterprise Fund. The note is not interest-bearing.

2. The municipal golf course and tennis club purchased land and constructed the facilities which totaled expenditures of $23,700,000.

3. Bonds were issued by the municipal golf course and tennis club for $20,000,000, par value of the bonds.

4. Membership fees were billed in the amount of $4,800,000. $4,200,000 was collected.

5. $5,000,000 was repaid to the general fund, with the anticipation of repaying $5,000,000 more per year for the next four years.

Required:

Prepare the necessary journal entries for each of the above transactions for the Enterprise Fund.

(Essay)

4.8/5 (38)

Interest payments on loans outstanding that do not relate to acquiring, constructing or improving capital assets are classified as ________ on the cash flow statement for an Enterprise Fund.

(Multiple Choice)

4.9/5 (43)

In a Statement of Cash Flows for a proprietary fund, what are the primary categories of cash flow activities?

(Multiple Choice)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)