Exam 10: Partnerships: Formation, Operation, and Basis

Exam 1: Understanding and Working With the Federal Tax Law74 Questions

Exam 2: Corporations: Introduction and Operating Rules113 Questions

Exam 3: Corporations: Special Situations109 Questions

Exam 4: Corporations: Organization and Capital Structure92 Questions

Exam 5: Corporations: Earnings Profits and Dividend Distributions130 Questions

Exam 6: Corporations: Redemptions and Liquidations115 Questions

Exam 7: Corporations: Reorganizations140 Questions

Exam 8: Consolidated Tax Returns175 Questions

Exam 9: Taxation of International Transactions177 Questions

Exam 10: Partnerships: Formation, Operation, and Basis135 Questions

Exam 11: Partnerships: Distributions, Transfer of Interests, and Terminations144 Questions

Exam 12: S: Corporations158 Questions

Exam 13: Comparative Forms of Doing Business170 Questions

Exam 14: Taxes on the Financial Statements87 Questions

Exam 15: Exempt Entities185 Questions

Exam 16: Multistate Corporate Taxation187 Questions

Exam 17: Tax Practice and Ethics174 Questions

Exam 18: The Federal Gift and Estate Taxes222 Questions

Exam 19: Family Tax Planning188 Questions

Exam 20: Income Taxation of Trusts and Estates183 Questions

Select questions type

In a limited liability company, all members are protected from all debts of the partnership unless they personally guaranteed the debt.

(True/False)

4.8/5  (43)

(43)

Emma's basis in her BBDE LLC interest is $60,000 at the beginning of the tax year. Her allocable share of LLC items are as follows: $20,000 of ordinary income, $2,000 tax-exempt interest income, and a $6,000 long-term capital gain. In addition, the LLC distributed $12,000 of cash to Emma during the year. Assuming the LLC had no liabilities at the beginning or the end of the year, Emma's ending basis in her LLC interest is $76,000.

(True/False)

4.8/5 (34)

Match each of the following statements with the terms below that provide the best definition.

a. Adjusted basis of each partnership asset.

b. Operating expenses incurred after entity is formed but before it begins doing business.

c. Each partner's basis in the partnership.

d. Reconciles book income to "taxable income."

e. Tax accounting election made by partnership.

f. Tax accounting calculation made by partner.

g. Tax accounting election made by partner.

h. Does not include liabilities.

i. Designed to prevent excessive deferral of taxation of partnership income.

j. Amount that may be received by partner for performance of services for the partnership.

k. Computation that determines the way recourse debt is shared.

l. Will eventually be allocated to partner making tax-free property contribution to partnership.

m. Partner's share of partnership items.

n. Must generally be satisfied by any allocation to the partners.

o. Justification for a tax year other than the required taxable year.

p. No correct match is provided.

-Partner's capital account

(Short Answer)

4.8/5 (42)

The MOP Partnership is involved in construction activities. Patricia has an adjusted basis for her partnership interest on January 1 of the current year of $600,000, consisting of the following:

During the year, the partnership has an operating loss of $1.2 million and distributes $60,000 of cash to Patricia. Partnership liabilities were the same at the end of the tax year, and the nonrecourse debt is not "qualified nonrecourse debt." If she owns a 60% share of partnership profits, capital, and losses, and is a material participant in the partnership, how much of her share of the operating loss can Patricia deduct? What Code provisions could cause a suspension of the loss? How would your answer change if MOP were an LLC and Patricia had not personally guaranteed any of the debt?

During the year, the partnership has an operating loss of $1.2 million and distributes $60,000 of cash to Patricia. Partnership liabilities were the same at the end of the tax year, and the nonrecourse debt is not "qualified nonrecourse debt." If she owns a 60% share of partnership profits, capital, and losses, and is a material participant in the partnership, how much of her share of the operating loss can Patricia deduct? What Code provisions could cause a suspension of the loss? How would your answer change if MOP were an LLC and Patricia had not personally guaranteed any of the debt?

(Essay)

4.8/5 (43)

Match each of the following statements with the terms below that provide the best definition.

a. Adjusted basis of each partnership asset.

b. Operating expenses incurred after entity is formed but before it begins doing business.

c. Each partner's basis in the partnership.

d. Reconciles book income to "taxable income."

e. Tax accounting election made by partnership.

f. Tax accounting calculation made by partner.

g. Tax accounting election made by partner.

h. Does not include liabilities.

i. Designed to prevent excessive deferral of taxation of partnership income.

j. Amount that may be received by partner for performance of services for the partnership.

k. Computation that determines the way recourse debt is shared.

l. Will eventually be allocated to partner making tax-free property contribution to partnership.

m. Partner's share of partnership items.

n. Must generally be satisfied by any allocation to the partners.

o. Justification for a tax year other than the required taxable year.

p. No correct match is provided.

-Schedule K-1

(Short Answer)

4.8/5 (40)

Ashley purchased her partnership interest from Lindsey on the first day of the current year for $40,000 cash. She received a $10,000 cash distribution from the partnership during the year, and her share of partnership income is $15,000. Her share of partnership liabilities on the last day of the partnership year is $20,000. Ashley's outside basis for her partnership interest at the end of the year is $45,000.

(True/False)

4.8/5 (36)

Carli contributes land to the newly formed CD Partnership in exchange for a 30% interest. The land has an adjusted basis and fair market value of $300,000 and is subject to a liability of $100,000, which the partnership assumes. None of this liability is repaid at year-end. At the end of the year, the partnership has trade accounts payable of $20,000. Assume all liabilities are allocated proportionately to the partners. Total partnership income for the year is $400,000. What is Carli's basis in her partnership interest at the end of the year?

(Essay)

4.8/5 (35)

Match each of the following statements with the terms below that provide the best definition.

a. Organizational choice of many large accounting firms.

b. Partner's percentage allocation of current operating income.

c. Might affect any two partners' tax liabilities in different ways.

d. Brokerage and registration fees incurred for promoting and marketing partnership interests.

e. Transfer of asset to partnership followed by immediate distribution of cash to partner.

f. Must have at least one general and one limited partner.

g. All partners are jointly and severally liable for entity debts.

h. Theory treating the partner and partnership as separate economic units.

i. Partner's basis in partnership interest after taxfree contribution of asset to partnership.

j. Partnership's basis in asset after taxfree contribution of asset to partnership.

k. Owners are "members."

l. Theory treating the partnership as a collection of taxpayers joined in an agency relationship.

m. Allows many unincorporated entities to select their Federal tax status.

n. No correct match provided.

-Limited liability company

(Short Answer)

4.7/5 (43)

Which of the following is a correct definition of a concept related to partnership taxation?

(Multiple Choice)

4.8/5 (31)

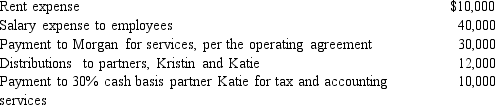

Morgan is a 50% managing member in the calendar year, cash basis MKK LLC. The LLC received $150,000 income from services and paid the following other amounts:

How much will Morgan's adjusted gross income increase as a result of the above items? What amount will be included in Morgan's selfemployment tax calculation?

How much will Morgan's adjusted gross income increase as a result of the above items? What amount will be included in Morgan's selfemployment tax calculation?

(Essay)

4.8/5 (38)

A partnership must provide any information to the partners that the partners would need to calculate deductions not permitted at the partnership level, such as for oil and gas depletion or the corporate dividends received deduction.

(True/False)

5.0/5 (39)

Match each of the following statements with the terms below that provide the best definition.

a. Organizational choice of many large accounting firms.

b. Partner's percentage allocation of current operating income.

c. Might affect any two partners' tax liabilities in different ways.

d. Brokerage and registration fees incurred for promoting and marketing partnership interests.

e. Transfer of asset to partnership followed by immediate distribution of cash to partner.

f. Must have at least one general and one limited partner.

g. All partners are jointly and severally liable for entity debts.

h. Theory treating the partner and partnership as separate economic units.

i. Partner's basis in partnership interest after taxfree contribution of asset to partnership.

j. Partnership's basis in asset after taxfree contribution of asset to partnership.

k. Owners are "members."

l. Theory treating the partnership as a collection of taxpayers joined in an agency relationship.

m. Allows many unincorporated entities to select their Federal tax status.

n. No correct match provided.

-Qualified nonrecourse debt

(Short Answer)

4.7/5 (37)

Match each of the following statements with the terms below that provide the best definition.

a. Adjusted basis of each partnership asset.

b. Operating expenses incurred after entity is formed but before it begins doing business.

c. Each partner's basis in the partnership.

d. Reconciles book income to "taxable income."

e. Tax accounting election made by partnership.

f. Tax accounting calculation made by partner.

g. Tax accounting election made by partner.

h. Does not include liabilities.

i. Designed to prevent excessive deferral of taxation of partnership income.

j. Amount that may be received by partner for performance of services for the partnership.

k. Computation that determines the way recourse debt is shared.

l. Will eventually be allocated to partner making tax-free property contribution to partnership.

m. Partner's share of partnership items.

n. Must generally be satisfied by any allocation to the partners.

o. Justification for a tax year other than the required taxable year.

p. No correct match is provided.

-Precontribution gain

(Short Answer)

4.9/5 (32)

A partnership will take a carryover basis in an asset it acquires when:

(Multiple Choice)

4.9/5 (36)

Match each of the following statements with the terms below that provide the best definition.

a. Organizational choice of many large accounting firms.

b. Partner's percentage allocation of current operating income.

c. Might affect any two partners' tax liabilities in different ways.

d. Brokerage and registration fees incurred for promoting and marketing partnership interests.

e. Transfer of asset to partnership followed by immediate distribution of cash to partner.

f. Must have at least one general and one limited partner.

g. All partners are jointly and severally liable for entity debts.

h. Theory treating the partner and partnership as separate economic units.

i. Partner's basis in partnership interest after taxfree contribution of asset to partnership.

j. Partnership's basis in asset after taxfree contribution of asset to partnership.

k. Owners are "members."

l. Theory treating the partnership as a collection of taxpayers joined in an agency relationship.

m. Allows many unincorporated entities to select their Federal tax status.

n. No correct match provided.

-Aggregate concept

(Short Answer)

4.8/5 (39)

A partnership is an association formed by two or more taxpayers (who may be any type of entity) to carry on a trade or business.

(True/False)

4.8/5 (37)

If a partnership earns tax-exempt income, the income should not affect the partners' bases in their partnership interests. Do you agree with this statement? Explain.

(Essay)

4.9/5 (40)

Match each of the following statements with the terms below that provide the best definition.

a. Organizational choice of many large accounting firms.

b. Partner's percentage allocation of current operating income.

c. Might affect any two partners' tax liabilities in different ways.

d. Brokerage and registration fees incurred for promoting and marketing partnership interests.

e. Transfer of asset to partnership followed by immediate distribution of cash to partner.

f. Must have at least one general and one limited partner.

g. All partners are jointly and severally liable for entity debts.

h. Theory treating the partner and partnership as separate economic units.

i. Partner's basis in partnership interest after taxfree contribution of asset to partnership.

j. Partnership's basis in asset after taxfree contribution of asset to partnership.

k. Owners are "members."

l. Theory treating the partnership as a collection of taxpayers joined in an agency relationship.

m. Allows many unincorporated entities to select their Federal tax status.

n. No correct match provided.

-Profits interest

(Short Answer)

4.8/5 (25)

Syndication costs arise when partnership interests are being marketed to investors. These costs cannot be amortized or deducted.

(True/False)

4.8/5 (41)

Which one of the following statements regarding partnership taxation is incorrect?

(Multiple Choice)

4.9/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)