Exam 5: Consolidation of Less-Than-Wholly-Owned Subsidiaries Acquired at More Than Book Value

Exam 1: Intercorporate Acquisitions and Investments in Other Entities58 Questions

Exam 2: Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No Differential59 Questions

Exam 3: The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries With No Differentials50 Questions

Exam 4: Consolidation of Wholly Owned Subsidiaries Acquired at More Than Book Value67 Questions

Exam 5: Consolidation of Less-Than-Wholly-Owned Subsidiaries Acquired at More Than Book Value58 Questions

Exam 6: Intercompany Inventory Transactions68 Questions

Exam 7: Intercompany Transfers of Services and Noncurrent Assets57 Questions

Exam 8: Intercompany Indebtedness50 Questions

Exam 8: Appendix A: Intercompany Indebtedness40 Questions

Exam 9: Consolidation Ownership Issues62 Questions

Exam 10: Additional Consolidation Reporting Issues58 Questions

Exam 11: Multinational Accounting: Foreign Currency Transactions and Financial Instruments74 Questions

Exam 12: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements75 Questions

Exam 13: Segment and Interim Reporting76 Questions

Exam 14: Sec Reporting49 Questions

Exam 15: Partnerships: Formation,operation,and Changes in Membership77 Questions

Exam 16: Partnerships: Liquidation67 Questions

Exam 17: Governmental Entities: Introduction and General Fund Accounting86 Questions

Exam 18: Governmental Entities: Special Funds and Government-Wide Financial Statements84 Questions

Exam 19: Not-For-Profit Entities126 Questions

Exam 20: Corporations in Financial Difficulty45 Questions

Select questions type

All of the following are examples of how a parent company may lose control over a subsidiary and discontinue future consolidation,except:

(Multiple Choice)

4.7/5  (43)

(43)

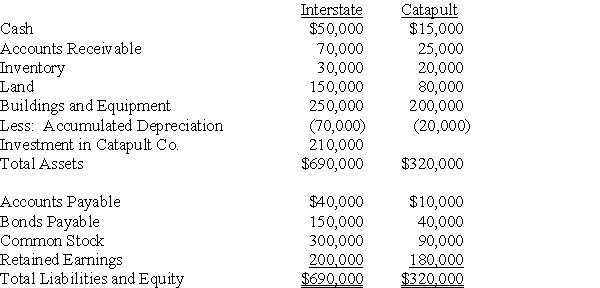

The following information applies to Questions 14 - 20

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company's common stock for $210,000 cash. The fair value of the noncontrolling interest at that date was determined to be $90,000. Data from the balance sheets of the two companies included the following amounts as of the date of acquisition:

At the date of the business combination, the book values of Catapult's assets and liabilities approximated fair value except for inventory, which had a fair value of $30,000, and land, which had a fair value of $95,000.

-Based on the preceding information,what amount will be reported as total stockholders' equity in the consolidated balance sheet prepared immediately after the business combination?

At the date of the business combination, the book values of Catapult's assets and liabilities approximated fair value except for inventory, which had a fair value of $30,000, and land, which had a fair value of $95,000.

-Based on the preceding information,what amount will be reported as total stockholders' equity in the consolidated balance sheet prepared immediately after the business combination?

(Multiple Choice)

4.9/5 (32)

The following information applies to Questions 32 - 34

On January 1, 20X2, Ephraim Corporation acquired 80 percent of Lilac Corporation for $200,000 cash. Lilac reported net income of $25,000 each year and dividends of $5,000 each year for 20X2, 20X3, and 20X4. On January 1, 20X2, Lilac reported common stock outstanding of $160,000 and retained earnings of $40,000, and the fair value of the noncontrolling interest was $50,000. It held land with a book value of $90,000 and a market value of $100,000, and equipment with a book value of $40,000 and a market value of $48,000 at the date of combination. The remainder of the differential at acquisition was attributable to an increase in the value of patents, which had a remaining useful life of eight years. All depreciable assets held by Lilac at the date of acquisition had a remaining economic life of eight years. Ephraim uses the equity method in accounting for its investment in Lilac.

-Based on the preceding information,what balance would Ephraim report as its investment in Lilac at January 1,20X5?

(Multiple Choice)

4.8/5 (39)

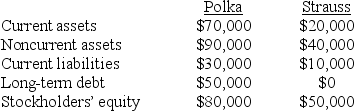

The following information applies to Questions 41-45

On January 1, 20X6, Polka Co. (Polka) and Strauss Co. (Strauss) had condensed balance sheets as follows:

On January 2, 20X6, Polka borrowed $90,000 and used the proceeds to acquire 90% of the outstanding common shares of Strauss. This debt is payable in ten equal annual principal and accrued interest payments beginning December 30, 20X6. On the acquisition date, the fair value of Strauss was $100,000, and the excess cost of the investment over Strauss's carrying amount of acquired net assets should be allocated 60% to inventory and 40% to goodwill.

-Current liabilities on the January 2,20X6,consolidated balance sheet should be:

On January 2, 20X6, Polka borrowed $90,000 and used the proceeds to acquire 90% of the outstanding common shares of Strauss. This debt is payable in ten equal annual principal and accrued interest payments beginning December 30, 20X6. On the acquisition date, the fair value of Strauss was $100,000, and the excess cost of the investment over Strauss's carrying amount of acquired net assets should be allocated 60% to inventory and 40% to goodwill.

-Current liabilities on the January 2,20X6,consolidated balance sheet should be:

(Multiple Choice)

4.8/5 (46)

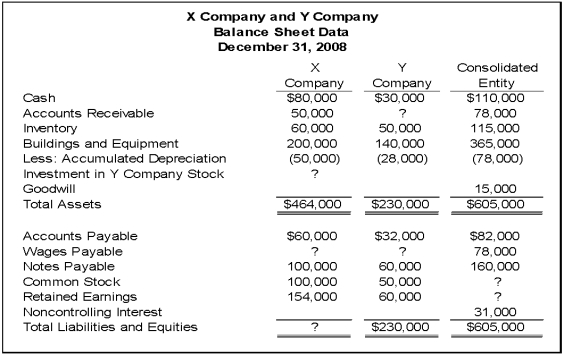

The following information applies to Questions 21-26

On December 31, 20X8, X Company acquired controlling ownership of Y Company. A consolidated balance sheet was prepared immediately. Partial balance sheet data for the two companies and the consolidated entity at that date follow:

During 20X8, X Company provided consulting services to Y Company and has not yet paid for them. There were no other receivables or payables between the companies at December 31, 20X8.

-Based on the information given,what is the amount of unpaid consulting services at December 31,20X8,on work done by X Company for Y Company?

-Based on the information given,what is the amount of unpaid consulting services at December 31,20X8,on work done by X Company for Y Company?

(Multiple Choice)

4.8/5 (38)

Based on the preceding information,what amount of goodwill will be reported in the consolidated balance sheet immediately following the acquisition?

(Multiple Choice)

4.8/5 (29)

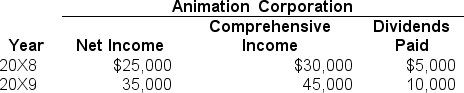

The following information applies to Questions 48-51:

On January 1, 20X8, Bristol Company acquired 80 percent of Animation Company's common stock for $280,000 cash. At that date, Animation reported common stock outstanding of $200,000 and retained earnings of $100,000, and the fair value of the noncontrolling interest was $70,000. The book values and fair values of Animation's assets and liabilities were equal, except for other intangible assets which had a fair value $50,000 greater than book value and an 8-year remaining life. Animation reported  Bristol reported net income of $100,000 and paid dividends of $30,000 for both the years.

-Based on the preceding information,what is the amount of comprehensive income attributable to the controlling interest for 20X8?

Bristol reported net income of $100,000 and paid dividends of $30,000 for both the years.

-Based on the preceding information,what is the amount of comprehensive income attributable to the controlling interest for 20X8?

(Multiple Choice)

4.7/5 (44)

The following information applies to Questions 35-26

On December 31, 20X8, Melkor Corporation acquired 80 percent of Sydney Company's common stock for $160,000. At that date, the fair value of the noncontrolling interest was $40,000. Of the $75,000 differential, $10,000 related to the increased value of Sydney's inventory, $20,000 related to the increased value of its land, and $25,000 related to the increased value of its equipment that had a remaining life of 10 years from the date of combination. Sydney sold all inventory it held at the end of 20X8 during 20X9. The land to which the differential related was also sold during 20X9 for a large gain. At the date of combination, Sydney reported retained earnings of $75,000 and common stock outstanding of $50,000. In 20X9, Sydney reported net income of $60,000, but paid no dividends. Melkor accounts for its investment in Sydney using the equity method.

-Based on the preceding information,the amount of goodwill reported in the consolidated financial statements prepared immediately after the combination is:

(Multiple Choice)

4.9/5 (33)

The following information applies to Questions 21-26

On December 31, 20X8, X Company acquired controlling ownership of Y Company. A consolidated balance sheet was prepared immediately. Partial balance sheet data for the two companies and the consolidated entity at that date follow:

During 20X8, X Company provided consulting services to Y Company and has not yet paid for them. There were no other receivables or payables between the companies at December 31, 20X8.

-Based on the information given,what balance in accounts receivable did Y Company report at December 31,20X8?

(Multiple Choice)

4.8/5 (30)

The following information applies to Questions 14 - 20

On January 1, 20X6, Interstate Corporation acquired 70 percent of Catapult Company's common stock for $210,000 cash. The fair value of the noncontrolling interest at that date was determined to be $90,000. Data from the balance sheets of the two companies included the following amounts as of the date of acquisition:

At the date of the business combination, the book values of Catapult's assets and liabilities approximated fair value except for inventory, which had a fair value of $30,000, and land, which had a fair value of $95,000.

-Based on the preceding information,what amount of total inventory will be reported in the consolidated balance sheet prepared immediately after the business combination?

(Multiple Choice)

4.8/5 (31)

Magellan Corporation acquired 80 percent ownership of Dipper Corporation on January 1,20X8,for $200,000.At that date,Dipper reported common stock outstanding of $75,000 and retained earnings of $150,000.The fair value of the noncontrolling interest was $50,000.The differential is assigned to equipment,which had a fair value $25,000 greater than book value and a remaining economic life of five years at the date of the business combination.Dipper reported net income of $40,000 and paid dividends of $20,000 in 20X8.

Required:

1)Provide the journal entries recorded by Magellan during 20X8 on its books if it accounts for its investment in Dipper using the equity method.

2)Give the consolidating entries needed at December 31,20X8,to prepare consolidated financial statements.

Problem 56 (continued):

(Essay)

4.8/5 (34)

Based on the preceding information,what amount will be reported as investment in Silver Corporation stock in the consolidated balance sheet immediately following the acquisition?

(Multiple Choice)

4.9/5 (37)

The following information applies to Questions 32 - 34

On January 1, 20X2, Ephraim Corporation acquired 80 percent of Lilac Corporation for $200,000 cash. Lilac reported net income of $25,000 each year and dividends of $5,000 each year for 20X2, 20X3, and 20X4. On January 1, 20X2, Lilac reported common stock outstanding of $160,000 and retained earnings of $40,000, and the fair value of the noncontrolling interest was $50,000. It held land with a book value of $90,000 and a market value of $100,000, and equipment with a book value of $40,000 and a market value of $48,000 at the date of combination. The remainder of the differential at acquisition was attributable to an increase in the value of patents, which had a remaining useful life of eight years. All depreciable assets held by Lilac at the date of acquisition had a remaining economic life of eight years. Ephraim uses the equity method in accounting for its investment in Lilac.

-Based on the preceding information,the increase in the fair value of patents held by Lilac is

(Multiple Choice)

4.8/5 (31)

The following information applies to Questions 41-45

On January 1, 20X6, Polka Co. (Polka) and Strauss Co. (Strauss) had condensed balance sheets as follows:

On January 2, 20X6, Polka borrowed $90,000 and used the proceeds to acquire 90% of the outstanding common shares of Strauss. This debt is payable in ten equal annual principal and accrued interest payments beginning December 30, 20X6. On the acquisition date, the fair value of Strauss was $100,000, and the excess cost of the investment over Strauss's carrying amount of acquired net assets should be allocated 60% to inventory and 40% to goodwill.

-Current assets on the January 2,20X6,consolidated balance sheet should be:

(Multiple Choice)

4.9/5 (41)

The following information applies to Questions 21-26

On December 31, 20X8, X Company acquired controlling ownership of Y Company. A consolidated balance sheet was prepared immediately. Partial balance sheet data for the two companies and the consolidated entity at that date follow:

During 20X8, X Company provided consulting services to Y Company and has not yet paid for them. There were no other receivables or payables between the companies at December 31, 20X8.

-Based on the information given,what amount will be reported as total controlling interest in the consolidated balance sheet?

(Multiple Choice)

4.9/5 (38)

The following information applies to Questions 48-51:

On January 1, 20X8, Bristol Company acquired 80 percent of Animation Company's common stock for $280,000 cash. At that date, Animation reported common stock outstanding of $200,000 and retained earnings of $100,000, and the fair value of the noncontrolling interest was $70,000. The book values and fair values of Animation's assets and liabilities were equal, except for other intangible assets which had a fair value $50,000 greater than book value and an 8-year remaining life. Animation reported Bristol reported net income of $100,000 and paid dividends of $30,000 for both the years.

-Based on the preceding information,what is the amount of comprehensive income attributable to the controlling interest for 20X9?

(Multiple Choice)

4.9/5 (37)

The following information applies to Questions 21-26

On December 31, 20X8, X Company acquired controlling ownership of Y Company. A consolidated balance sheet was prepared immediately. Partial balance sheet data for the two companies and the consolidated entity at that date follow:

During 20X8, X Company provided consulting services to Y Company and has not yet paid for them. There were no other receivables or payables between the companies at December 31, 20X8.

-Based on the information given,what percentage of Y Company's shares were acquired by X Company?

(Multiple Choice)

4.9/5 (36)

The following information applies to Questions 37 - 38

On December 31, 20X5, Paris Corporation acquired 60 percent of Sanlo Company's common stock for $180,000. At that date, the fair value of the noncontrolling interest was $120,000. Of the $45,000 differential, $5,000 related to the increased value of Sanlo's inventory, $15,000 related to the increased value of its land, and $10,000 related to the increased value of its equipment that had a remaining life of five years from the date of combination. Sanlo sold all inventory it held at the end of 20X5 during 20X6. The land to which the differential related was also sold during 20X6 for a large gain. In 20X6, Sanlo reported net income of $40,000 but paid no dividends. Paris accounts for its investment in Sanlo using the equity method.

-Based on the preceding information,the amount of goodwill reported in the consolidated financial statements prepared immediately after the combination is

(Multiple Choice)

4.9/5 (45)

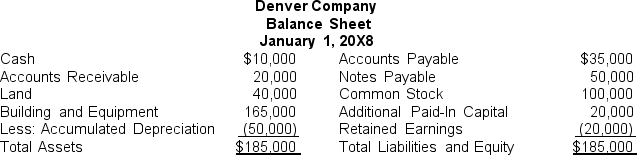

The following information applies to Questions 52-53

On January 1, 20X8, Colorado Corporation acquired 75 percent of Denver Company's voting common stock for $90,000 cash. At that date, the fair value of the noncontrolling interest was $30,000. Denvers's balance sheet at the date of acquisition contained the following balances:

At the date of acquisition, the reported book values of Denver's assets and liabilities approximated fair value. Consolidating entries are being made to prepare a consolidated balance sheet immediately following the business combination.

-Based on the preceding information,the amount of goodwill reported is:

At the date of acquisition, the reported book values of Denver's assets and liabilities approximated fair value. Consolidating entries are being made to prepare a consolidated balance sheet immediately following the business combination.

-Based on the preceding information,the amount of goodwill reported is:

(Multiple Choice)

4.9/5 (47)

The following information applies to Questions 21-26

On December 31, 20X8, X Company acquired controlling ownership of Y Company. A consolidated balance sheet was prepared immediately. Partial balance sheet data for the two companies and the consolidated entity at that date follow:

During 20X8, X Company provided consulting services to Y Company and has not yet paid for them. There were no other receivables or payables between the companies at December 31, 20X8.

-Based on the information given,what was the fair value of Y Company as a whole at the date of acquisition?

(Multiple Choice)

4.9/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)