Exam 2: Asset Allocation and Security Selection: Part A

Exam 1: The Investment Setting72 Questions

Exam 1: The Investment Setting: Part A6 Questions

Exam 2: Asset Allocation and Security Selection77 Questions

Exam 2: Asset Allocation and Security Selection: Part A3 Questions

Exam 3: Organization and Functioning of Securities Markets87 Questions

Exam 4: Security Market Indexes and Index Funds89 Questions

Exam 5: Efficient Capital Markets, Behavioral Finance, and Technical Analysis162 Questions

Exam 6: An Introduction to Portfolio Management114 Questions

Exam 6: An Introduction to Portfolio Management: Part A2 Questions

Exam 6: An Introduction to Portfolio Management: Part B2 Questions

Exam 7: Asset Pricing Models152 Questions

Exam 8: Equity Valuation83 Questions

Exam 9: The Top-Down Approach to Market, Industry, and Company Analysis216 Questions

Exam 10: The Practice of Fundamental Investing60 Questions

Exam 11: Equity Portfolio Management Strategies65 Questions

Exam 12: Bond Fundamentals and Valuation138 Questions

Exam 13: Bond Analysis and Portfolio Management Strategies125 Questions

Exam 14: An Introduction to Derivative Markets and Securities102 Questions

Exam 15: Forward, Futures, and Swap Contracts148 Questions

Exam 16: Option Contracts122 Questions

Exam 17: Professional Money Management, Alternative Assets, and Industry Ethics109 Questions

Exam 18: Evaluation of Portfolio Performance111 Questions

Select questions type

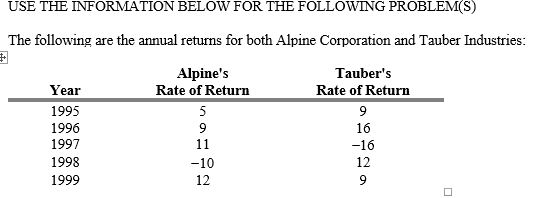

-Refer to Exhibit 2A.1. Calculate the coefficient of correlation.

-Refer to Exhibit 2A.1. Calculate the coefficient of correlation.

Free

(Multiple Choice)

4.9/5  (39)

(39)

Correct Answer: Verified

Verified

B

What is the correlation coefficient for two assets with a covariance of .0032, if asset 1 has a standard deviation of 12 percent and asset 2 has a standard deviation of 9 percent?

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

A

-Refer to Exhibit 2A.1. Calculate the covariance.

Free

(Multiple Choice)

5.0/5 (40)

Correct Answer:Verified

A

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)