Exam 5: Efficient Capital Markets, Behavioral Finance, and Technical Analysis

Exam 1: The Investment Setting72 Questions

Exam 1: The Investment Setting: Part A6 Questions

Exam 2: Asset Allocation and Security Selection77 Questions

Exam 2: Asset Allocation and Security Selection: Part A3 Questions

Exam 3: Organization and Functioning of Securities Markets87 Questions

Exam 4: Security Market Indexes and Index Funds89 Questions

Exam 5: Efficient Capital Markets, Behavioral Finance, and Technical Analysis162 Questions

Exam 6: An Introduction to Portfolio Management114 Questions

Exam 6: An Introduction to Portfolio Management: Part A2 Questions

Exam 6: An Introduction to Portfolio Management: Part B2 Questions

Exam 7: Asset Pricing Models152 Questions

Exam 8: Equity Valuation83 Questions

Exam 9: The Top-Down Approach to Market, Industry, and Company Analysis216 Questions

Exam 10: The Practice of Fundamental Investing60 Questions

Exam 11: Equity Portfolio Management Strategies65 Questions

Exam 12: Bond Fundamentals and Valuation138 Questions

Exam 13: Bond Analysis and Portfolio Management Strategies125 Questions

Exam 14: An Introduction to Derivative Markets and Securities102 Questions

Exam 15: Forward, Futures, and Swap Contracts148 Questions

Exam 16: Option Contracts122 Questions

Exam 17: Professional Money Management, Alternative Assets, and Industry Ethics109 Questions

Exam 18: Evaluation of Portfolio Performance111 Questions

Select questions type

The performance of four major groups of investors has been studied in connection with tests of the strong-form of the efficient market hypothesis. These include all of the following EXCEPT

(Multiple Choice)

4.8/5  (42)

(42)

Technicians using the confidence index published by Barron's to make investment decisions

(Multiple Choice)

4.9/5 (36)

If a technical trading rule is successful, then more traders use it, causing the rule to become even more successful.

(True/False)

4.8/5 (38)

Fusion investing is the integration of the following elements of investment valuation:

(Multiple Choice)

4.9/5 (37)

The implication of efficient capital markets and a lack of superior analysts have led to the introduction of

(Multiple Choice)

4.8/5 (36)

According to technical analysts, which mutual fund cash position guides investment decisions?

(Multiple Choice)

4.8/5 (38)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Rit = return for stock i during period t

Rmt = return for the aggregate market during period t

-Refer to Exhibit 5.4. What is the abnormal rate of return for Stock A during period t using only the aggregate market return (ignore differential systematic risk)?

Rit = return for stock i during period t

Rmt = return for the aggregate market during period t

-Refer to Exhibit 5.4. What is the abnormal rate of return for Stock A during period t using only the aggregate market return (ignore differential systematic risk)?

(Multiple Choice)

4.8/5 (37)

For technical trading rules to consistently generate superior returns, the market would have to be inefficient.

(True/False)

4.8/5 (44)

Which of the following is NOT a technical trading rule category?

(Multiple Choice)

4.8/5 (46)

Based on the daily closings for the Dow Jones Industrial Average given in the table below, calculate a four-day moving average for Day 4.

(Multiple Choice)

4.9/5 (48)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

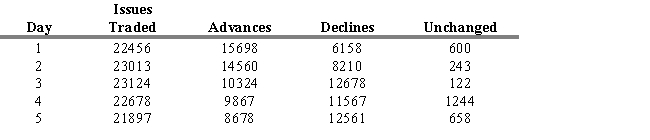

The table below provides five days of trade data.

-Refer to Exhibit 5.8. Calculate the final value of the cumulative advance-decline line at the end of the fifth day.

-Refer to Exhibit 5.8. Calculate the final value of the cumulative advance-decline line at the end of the fifth day.

(Multiple Choice)

4.9/5 (45)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The table below provides five days of trade data.

-Refer to Exhibit 5.8. Calculate the net advance-decline for day 5.

(Multiple Choice)

5.0/5 (37)

Studies examining stock splits support the semistrong-form efficient market hypothesis.

(True/False)

4.9/5 (38)

Technical analysis and the efficient market hypothesis have a consistent set of assumptions concerning stock market behavior.

(True/False)

4.7/5 (33)

The strong form of the efficient market hypothesis contends that only insiders can earn abnormal returns.

(True/False)

5.0/5 (41)

The relative strength index for a stock is equal to the price of the stock

(Multiple Choice)

4.8/5 (39)

The Dow Theory describes stock prices as moving in trends analogous to the movement of water. Which of the following statements is NOT true?

(Multiple Choice)

4.8/5 (24)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Rit = return for stock i during period t

Rmt = return for the aggregate market during period t

-Refer to Exhibit 5.1. What is the abnormal rate of return for Stock C during period t using only the aggregate market return (ignore differential systematic risk)?

Rit = return for stock i during period t

Rmt = return for the aggregate market during period t

-Refer to Exhibit 5.1. What is the abnormal rate of return for Stock C during period t using only the aggregate market return (ignore differential systematic risk)?

(Multiple Choice)

4.8/5 (35)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Rit = return for stock i during period t

Rmt = return for the aggregate market during period t

-Refer to Exhibit 5.2. What is the abnormal rate of return for Stock ABC during period t using only the aggregate market return (ignore differential systematic risk)?

Rit = return for stock i during period t

Rmt = return for the aggregate market during period t

-Refer to Exhibit 5.2. What is the abnormal rate of return for Stock ABC during period t using only the aggregate market return (ignore differential systematic risk)?

(Multiple Choice)

4.9/5 (34)

If statistical tests of stock returns over time support the efficient market hypothesis, then the resulting correlations should be

(Multiple Choice)

4.9/5 (48)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)