Exam 15: Forward, Futures, and Swap Contracts

Exam 1: The Investment Setting72 Questions

Exam 1: The Investment Setting: Part A6 Questions

Exam 2: Asset Allocation and Security Selection77 Questions

Exam 2: Asset Allocation and Security Selection: Part A3 Questions

Exam 3: Organization and Functioning of Securities Markets87 Questions

Exam 4: Security Market Indexes and Index Funds89 Questions

Exam 5: Efficient Capital Markets, Behavioral Finance, and Technical Analysis162 Questions

Exam 6: An Introduction to Portfolio Management114 Questions

Exam 6: An Introduction to Portfolio Management: Part A2 Questions

Exam 6: An Introduction to Portfolio Management: Part B2 Questions

Exam 7: Asset Pricing Models152 Questions

Exam 8: Equity Valuation83 Questions

Exam 9: The Top-Down Approach to Market, Industry, and Company Analysis216 Questions

Exam 10: The Practice of Fundamental Investing60 Questions

Exam 11: Equity Portfolio Management Strategies65 Questions

Exam 12: Bond Fundamentals and Valuation138 Questions

Exam 13: Bond Analysis and Portfolio Management Strategies125 Questions

Exam 14: An Introduction to Derivative Markets and Securities102 Questions

Exam 15: Forward, Futures, and Swap Contracts148 Questions

Exam 16: Option Contracts122 Questions

Exam 17: Professional Money Management, Alternative Assets, and Industry Ethics109 Questions

Exam 18: Evaluation of Portfolio Performance111 Questions

Select questions type

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 15.3. If 90-day LIBOR rises to the levels "predicted" by the implied forward rates, what will the dollar level of the bank's interest receipt be at the end of the first quarter?

-Refer to Exhibit 15.3. If 90-day LIBOR rises to the levels "predicted" by the implied forward rates, what will the dollar level of the bank's interest receipt be at the end of the first quarter?

(Multiple Choice)

4.9/5  (41)

(41)

A pay-fixed interest rate swap can be viewed as equivalent to

(Multiple Choice)

4.7/5 (35)

Assume the exchange rate is GBP 1.35/USD, the US risk-free rate is 3.0 percent, and the UK risk-free rate is 3.0 percent. What is the implied one-year forward rate?

(Multiple Choice)

5.0/5 (40)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

TexMex Corporation has decided to borrow $50,000,000 for six months in two three-month issues. The corporation is concerned that interest rates will rise over the next three months. Thus, the corporation purchases a 3 * 6 FRA whereby the corporation pays the dealer's quoted fixed rate of 3.5 percent in exchange for receiving three-month LIBOR at the settlement date. In order to hedge her exposure, the dealer buys LIBOR from Newport Inc. at its bid rate of 3 percent. The notional principal is $50,000,000 and that there are 60 days between month 3 and month 6.

-Refer to Exhibit 15.18. How much compensation does the dealer receive for transaction costs, credit risk, and other costs associated with matching the FRAs?

(Multiple Choice)

4.9/5 (46)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

December futures on the S&P 500 stock index trade at 250 times the index value of 1187.70. Your broker requires an initial margin of 10 percent on futures contracts. The current value of the S&P 500 stock index is 1178.

-Refer to Exhibit 15.14. How much must you deposit in a margin account if you wish to purchase one contract?

(Multiple Choice)

4.8/5 (32)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Chimichango Industries has decided to borrow $50,000,000.00 for six months in two three-month issues. As the Treasurer, you are concerned that interest rates will rise over the next three months and the rate upon which the second payment will be based will be undesirable. (The amount of Chimichango's first payment will be known at origination.) To reduce the company's interest rate exposure, you decide to purchase a 3 * 6 FRA whereby you pay the dealer's quoted fixed rate of 5.91 percent in exchange for receiving three-month LIBOR at the settlement date. In order to hedge her exposure, the dealer buys LIBOR from Megabuks Industries at its bid rate of 5.85 percent. (Assume a notional principal of $50,000,000.00 and that there are 60 days between month 3 and month 6.)

-Refer to Exhibit 15.16. Assuming that three-month LIBOR is 5.6 percent on the rate determination day, and the contract specified settlement in advance, describe the transaction that occurs between the dealer and Megabuks.

(Multiple Choice)

4.8/5 (27)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

As a portfolio manager, you are responsible for a $150 million portfolio, 90 percent of which is invested in equities, with a portfolio beta of 1.25. You are utilizing the S&P 500 as your passive benchmark. Currently the S&P 500 is valued at 1202. The value of the S&P 500 futures contract is equal to $250 times the value of the index. The beta of the futures contract is 1.0.

-Refer to Exhibit 15.11. If you anticipate a cash outflow of $5 million next week, how many futures contracts should you buy or sell in order to mitigate the effect of this outflow on the portfolio's performance (rounded to the nearest integer)?

(Multiple Choice)

4.9/5 (40)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 15.3. What is the implied 90-day forward rate at the beginning of the third quarter?

(Multiple Choice)

4.8/5 (35)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

As a relationship officer for a money-center commercial bank, one of your corporate accounts has just approached you about a one-year loan for $3,000,000. The customer would pay a quarterly interest expense based on the prevailing level of LIBOR at the beginning of each quarter. As is the bank's convention on all such loans, the amount of the interest payment would then be paid at the end of the quarterly cycle when the new rate for the next cycle is determined. You observe the following LIBOR yield curve in the cash market:

-Refer to Exhibit 15.3. What is the implied 90-day forward rate at the beginning of the second quarter?

(Multiple Choice)

5.0/5 (36)

According to the cost of carry model, the futures price is the present value of the spot price discounted at the risk-free rate.

(True/False)

4.8/5 (33)

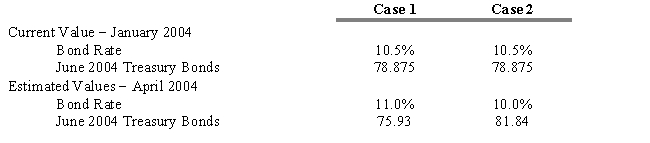

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

In late January 2004, The Union Cosmos Company is considering the sale of $100 million in 10-year bonds that will probably be rated AAA like the firm's other bond issues. The firm is anxious to proceed at today's rate of 10.5 percent. As treasurer, you know that it will take until sometime in April to get the issue registered and sold. Therefore, you suggest that the firm hedge the pending issue using Treasury bond futures contracts each representing $100,000.

-Refer to Exhibit 15.1. What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs).

-Refer to Exhibit 15.1. What is the dollar gain or loss assuming that future conditions described in Case 2 actually occur? (Ignore commissions and margin costs).

(Multiple Choice)

4.9/5 (33)

The number of future contracts needed to hedge a unit of the spot assets is solely a function of the variance of the spot prices.

(True/False)

4.8/5 (39)

Assume that you manage an equity portfolio. The portfolio beta is 1.15. You anticipate a decline in equity values and wish to hedge $500 million of the portfolio. Calculate the number of contracts you would need to hedge your position and indicate whether you would go short or long. Assume that the price of the S&P 500 futures contract is 1105 and the multiplier is 250.

(Multiple Choice)

4.9/5 (34)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

December futures on the S&P 500 stock index trade at 250 times the index value of 1187.70. Your broker requires an initial margin of 10 percent on futures contracts. The current value of the S&P 500 stock index is 1178.

-Refer to Exhibit 15.14. Calculate the return on a cash investment in the S&P 500 stock index if the ending index value is 1170 over the same time period.

(Multiple Choice)

4.8/5 (34)

The Eurodollar futures contract is a popular hedging vehicle because it is based on the three-month LIBOR.

(True/False)

4.8/5 (34)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Chimichango Industries has decided to borrow $50,000,000.00 for six months in two three-month issues. As the Treasurer, you are concerned that interest rates will rise over the next three months and the rate upon which the second payment will be based will be undesirable. (The amount of Chimichango's first payment will be known at origination.) To reduce the company's interest rate exposure, you decide to purchase a 3 * 6 FRA whereby you pay the dealer's quoted fixed rate of 5.91 percent in exchange for receiving three-month LIBOR at the settlement date. In order to hedge her exposure, the dealer buys LIBOR from Megabuks Industries at its bid rate of 5.85 percent. (Assume a notional principal of $50,000,000.00 and that there are 60 days between month 3 and month 6.)

-Refer to Exhibit 15.16. How much compensation does the dealer receive for transaction costs, credit risk, and other costs associated with matching the FRAs?

(Multiple Choice)

4.8/5 (36)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The WallMal Company has entered into a four-year interest rate swap, with semiannual settlement, to pay a fixed rate of 8 percent per year and receive six-month LIBOR. The notional principal is $50,000,000.

-Refer to Exhibit 15.19. Indicate the market value of the swap to the WallMal Company.

(Multiple Choice)

4.9/5 (37)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The S&P 500 stock index is at 1100. The annualized interest rate is 3.5 percent, and the annualized dividend is 2 percent.

-Refer to Exhibit 15.9. If the futures contract was currently available for 1050, indicate the appropriate strategy that would earn an arbitrage profit.

(Multiple Choice)

4.8/5 (46)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

The S&P 500 stock index is at 1100. The annualized interest rate is 3.5 percent, and the annualized dividend is 2 percent.

-Refer to Exhibit 15.9. If the futures contract was currently available for 1250, indicate the appropriate strategy that would earn an arbitrage profit.

(Multiple Choice)

4.8/5 (29)

USE THE INFORMATION BELOW FOR THE FOLLOWING PROBLEM(S)

Assume that you observe the following prices in the T-Bill and Eurodollar futures markets

-Refer to Exhibit 15.6. If you expected the spread to narrow over the next month, then an appropriate strategy would be to

-Refer to Exhibit 15.6. If you expected the spread to narrow over the next month, then an appropriate strategy would be to

(Multiple Choice)

4.8/5 (37)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)