Exam 8: Managing Interest Rate Risk: Economic Value of Equity

Exam 1: Banking and the Financial Services Industry50 Questions

Exam 2: Government Policies and Regulation65 Questions

Exam 3: Analyzing Bank Performance100 Questions

Exam 4: Managing Noninterest Income and Noninterest Expense35 Questions

Exam 5: The Performance of Nontraditional Banking Companies40 Questions

Exam 6: Pricing Fixed-Income Securities50 Questions

Exam 7: Managing Interest Rate Risk: Gap and Earnings Sensitivity55 Questions

Exam 8: Managing Interest Rate Risk: Economic Value of Equity55 Questions

Exam 9: Using Derivatives to Manage Interest Rate Risk60 Questions

Exam 10: Funding the Bank55 Questions

Exam 11: Managing Liquidity40 Questions

Exam 12: The Effective Use of Capital50 Questions

Exam 13: Overview of Credit Policy and Loan Characteristics55 Questions

Exam 14: Evaluating Commercial Loan Requests and Managing Credit Risk50 Questions

Exam 15: Evaluating Consumer Loans50 Questions

Exam 16: Managing the Investment Portfolio65 Questions

Exam 17: Global Banking Activities35 Questions

Select questions type

Which of the following would generally be considered price sensitive?

(Multiple Choice)

5.0/5  (37)

(37)

Discuss the differences between assets and liabilities that are price sensitive and those that are rate sensitive.

(Essay)

4.9/5 (40)

Which of the following is likely to have a negative effective duration?

(Multiple Choice)

4.9/5 (31)

Duration of equity measures the dollar change in EVE with a 1% change in interest rates.

(True/False)

4.8/5 (33)

Why is it difficult to estimate the duration of demand deposits?

(Short Answer)

4.9/5 (37)

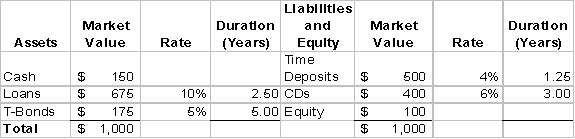

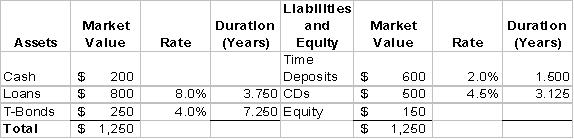

Use the following bank information for questions

-If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

-If interest rates rise 1% for all assets and liabilities, what is the approximate expected change in the economic value of equity?

(Multiple Choice)

4.8/5 (41)

Use the following bank information for questions

-What is the bank's weighted average cost of liabilities?

(Multiple Choice)

4.8/5 (31)

A liability sensitive bank decides to reduce risk by marketing 2-year CDs paying 5% instead of NOW accounts that pay 4%.The bank will benefit if:

(Multiple Choice)

4.9/5 (42)

Put the following steps in duration gap analysis in the proper order.

(Multiple Choice)

4.9/5 (40)

Economic value of equity analysis focuses on net interest income.

(True/False)

4.9/5 (39)

Use the following bank information for questions

-What is the bank's duration gap?

-What is the bank's duration gap?

(Multiple Choice)

4.7/5 (35)

An investor that matches the duration of an investment with her holding period balances price risk and reinvestment risk.

(True/False)

4.8/5 (40)

A 20-year zero coupon bond with a face value of $1,000 is currently selling for $214.55.Using the bond's modified duration, what is the approximate change in the price of the bond if interest rates rise by 25 basis points?

(Multiple Choice)

4.8/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)