Exam 13: Segment and Interim Reporting

Exam 1: Intercorporate Acquisitions and Investments in Other Entities46 Questions

Exam 2: Reporting Intercorporate Investments and Consolidation of Wholly Owned Subsidiaries With No Differential39 Questions

Exam 3: The Reporting Entity and Consolidation of Less-Than-Wholly-Owned Subsidiaries With No Differential39 Questions

Exam 4: Consolidation of Wholly Owned Subsidiaries Acquired at More Than Book Value47 Questions

Exam 5: Consolidation of Less-Than-Wholly-Owned Subsidiaries Acquired at More Than Book Value41 Questions

Exam 6: Intercompany Inventory Transactions49 Questions

Exam 7: Intercompany Transfers of Services and Noncurrent Assets46 Questions

Exam 8: Intercompany Indebtedness40 Questions

Exam 9: Consolidation Ownership Issues54 Questions

Exam 10: Additional Consolidation Reporting Issues47 Questions

Exam 11: Multinational Accounting: Foreign Currency Transactions and Financial Instruments66 Questions

Exam 12: Multinational Accounting: Issues in Financial Reporting and Translation of Foreign Entity Statements60 Questions

Exam 13: Segment and Interim Reporting52 Questions

Exam 14: Sec Reporting50 Questions

Exam 15: Partnerships: Formation, operation, and Changes in Membership56 Questions

Exam 16: Partnerships: Liquidation49 Questions

Exam 17: Governmental Entities: Introduction and General Fund Accounting69 Questions

Exam 18: Governmental Entities: Special Funds and Government-Wide Financial Statements66 Questions

Exam 19: Not-For-Profit Entities112 Questions

Exam 20: Corporations in Financial Difficulty41 Questions

Select questions type

Crisfield Company has two reportable segments,C and D.Segment C made $4,000,000 of sales to external customers and $400,000 of sales to other operating segments.Segment D,on the other hand,made sales of $8,000,000 to external customers and $1,600,000 of sales to other operating segments.Crisfield Company reported $13,200,000 of revenues on its consolidated income statement.What calculation below correctly determines whether Crisfield Company's reportable segments satisfy the 75% revenue test?

(Multiple Choice)

4.8/5  (35)

(35)

Trimester Corporation's revenue for the year ended December 31,20X8,was as follows:

Trimester has a reportable operating segment if that segment's revenue exceeds:

(Multiple Choice)

4.8/5 (33)

Trevor Company discloses supplementary operating segment information for its three reportable segments.Data for 20X8 are available as follows:

Allocable costs for the year was $180,000.Allocable costs are assigned based on the ratio of a segment's income before allocable costs to total income before allocable costs.The 20X8 operating profit for Segment B was:

(Multiple Choice)

4.8/5 (39)

Estimated gross profit rates may be used to estimate a company's cost of goods sold and its ending inventory for:

(Multiple Choice)

4.7/5 (31)

Toledo Imports,a calendar-year corporation,had the following income before tax expense and estimated effective annual income tax rates for the first three quarters in 20X8:

Toledo's income tax expense in its interim income statement for the nine months ended September 30 and for the third quarter,respectively,are:

(Multiple Choice)

4.7/5 (44)

William Corporation,which has a fiscal year ending January 31,had the following pretax accounting income and estimated effective annual income tax rates for the first three quarters of the year ended January 31,20X8:

William's income tax expenses in its interim income statement for the third quarter are:

(Multiple Choice)

4.8/5 (35)

Missoula Corporation disposed of one of its segments in the second quarter and incurred a gain from disposal of discontinued segment of $600,000,net of taxes.What is the effect of this gain from disposal of discontinued segment?

(Multiple Choice)

4.8/5 (44)

Tyler Company incurred an inventory loss due to a decline in market prices during its first quarter of operations in 20X8.At the end of the first quarter,management of the company believed the decline in market prices to be permanent.In the second quarter,the market prices of Tyler's inventories increased above their acquisition cost.Market prices remained higher than acquisition cost during the remainder of 20X8.How should Tyler report the facts above on its first and second quarter income statements?

(Multiple Choice)

4.9/5 (28)

Wakefield Company uses a perpetual inventory system.In August,it sold 2,000 units from its LIFO-base inventory,which had originally cost $35 per unit.The replacement cost is expected to be $45 per unit.The company is planning to reduce its inventory and expects to replace only 1,500 of these units by December 31,the end of its fiscal year.The company replaced 1,500 units in November at an actual cost of $50 per unit.

-Based on the preceding information,in the entry to record the replacement of the 1,500 units in November,Inventory will be debited for:

(Multiple Choice)

4.9/5 (41)

All of the following are differences between international standards and U.S.GAAP regarding operating segments,except:

(Multiple Choice)

4.8/5 (41)

An analysis of Abbey Company's operating segments provides the following information:

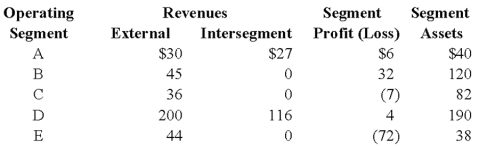

-Refer to the above information.Which of the operating segments above are reportable segments?

-Refer to the above information.Which of the operating segments above are reportable segments?

(Multiple Choice)

4.8/5 (31)

47.Lloyd Corporation reports the following information for 2008 for its three operating segments:

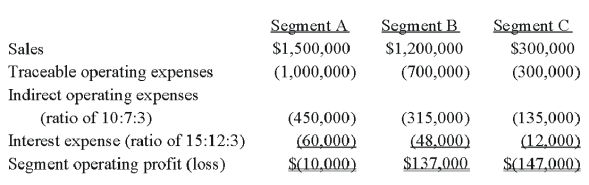

Indirect operating expenses are allocated to segments based upon the ratio of each segment's traceable operating expenses to total traceable operating expenses.Interest expense is allocated to segments based upon the ratio of each segment's sales to total sales.

Required:

a)Calculate the operating profit or loss for each of the segments for 2008.

b)Determine which segments are reportable,applying the operating profit or loss test.

Answer:

a)Operating profit or loss for each segment.

Note: General corporate expenses are not allocated for the purpose of identifying reportable segments.

b)Reportable segments.

Segments B and C both meet the operating profit or loss test.The absolute dollar amount of their respective operating profit and loss amounts are 10% or more of the absolute dollar amount of the combined segment operating losses of $157,000 ($10,000 loss + $147,000 loss).

Answer:

a)Operating profit or loss for each segment.

Note: General corporate expenses are not allocated for the purpose of identifying reportable segments.

b)Reportable segments.

Segments B and C both meet the operating profit or loss test.The absolute dollar amount of their respective operating profit and loss amounts are 10% or more of the absolute dollar amount of the combined segment operating losses of $157,000 ($10,000 loss + $147,000 loss).

-FASB 131 (ASC 280),Disclosure about Segments of an Enterprise and Related Information,has taken what has been referred to as a "management approach" to the definition of a segment and the allocation of costs to a segment.

Required:

a)What is meant by a management approach? How does this concept of a management approach impact the decision to disclose information?

b)How are decisions about cost allocation handled in segment disclosures?

-FASB 131 (ASC 280),Disclosure about Segments of an Enterprise and Related Information,has taken what has been referred to as a "management approach" to the definition of a segment and the allocation of costs to a segment.

Required:

a)What is meant by a management approach? How does this concept of a management approach impact the decision to disclose information?

b)How are decisions about cost allocation handled in segment disclosures?

(Essay)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)