Exam 6: Inventories

Exam 1: Uses of Accounting Information and the Financial Statements178 Questions

Exam 2: Measurement Concepts: Recording Business Transactions139 Questions

Exam 3: Measuring Business Income: Adjusting the Accounts168 Questions

Exam 4: Foundations of Financial Reporting and the Classified Balance Sheet130 Questions

Exam 5: Accounting for Merchandising Operations177 Questions

Exam 6: Inventories162 Questions

Exam 7: Cash and Internal Control141 Questions

Exam 8: Receivables111 Questions

Exam 9: Long-Term Assets227 Questions

Exam 10: Current Liabilities and Fair Value Accounting179 Questions

Exam 11: Long-Term Liabilities200 Questions

Exam 12: Stockholders Equity196 Questions

Exam 13: The Statement of Cash Flows147 Questions

Exam 14: Financial Statement Analysis164 Questions

Exam 15: Managerial Accounting and Cost Concepts199 Questions

Exam 16: Costing Systems: Job Order Costing121 Questions

Exam 17: Costing Systems: Process Costing139 Questions

Exam 18: Value-Based Systems: Activity-Based Costing and Lean Accounting146 Questions

Exam 19: Cost-Volume-Profit Analysis167 Questions

Exam 20: The Budgeting Process113 Questions

Exam 21: Flexible Budgets and Performance Analysis116 Questions

Exam 22: Standard Costing and Variance Analysis118 Questions

Exam 23: Short-Run Decision Analysis128 Questions

Exam 24: Capital Investment Analysis106 Questions

Exam 25: Pricing Decisions, including Target Costing and Transfer Pricing139 Questions

Exam 26: Quality Management and Measurement101 Questions

Exam 27: Accounting for Unincorporated Businesses106 Questions

Exam 28: Accounting for Investments112 Questions

Select questions type

An overstatement of ending inventory in a period will result in an understatement of gross margin in that period.

(True/False)

4.8/5  (38)

(38)

Which of the following costs would not be included in the inventory cost?

(Multiple Choice)

4.8/5 (44)

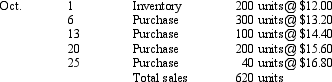

Use this inventory information for the month of March to answer the following question.  -Assuming that a periodic inventory system is used,what is ending inventory (rounded)under the average-cost method?

-Assuming that a periodic inventory system is used,what is ending inventory (rounded)under the average-cost method?

(Multiple Choice)

4.9/5 (44)

To increase their levels of inventory,many merchandisers and manufacturers use supply-chain management in conjunction with a just-in-time operating environment.

(True/False)

4.9/5 (40)

Applying the lower-of-cost-or-market rule follows which of the following accounting conventions?

(Multiple Choice)

4.9/5 (34)

A retail store prices its goods to achieve a gross margin of 35 percent.Up to the date of a fire that destroyed the store's inventory,sales were $250,000 and cost of goods available for sale was $175,000.The estimated cost of the inventory destroyed is

(Multiple Choice)

4.8/5 (35)

The specific identification method is well suited for a discount department store.

(True/False)

4.9/5 (36)

A cost-to-retail percentage must be calculated when applying the gross profit method.

(True/False)

4.9/5 (30)

How is the matching rule applied when accounting for merchandise inventory?

(Essay)

4.9/5 (37)

Use this information to answer the following question.  A periodic inventory system is used.

-Using the average-cost method,the cost assigned to ending inventory is

A periodic inventory system is used.

-Using the average-cost method,the cost assigned to ending inventory is

(Multiple Choice)

4.9/5 (38)

Which inventory method generally best follows the matching principle?

(Multiple Choice)

4.8/5 (35)

When the average-cost method is applied to a perpetual inventory system,the sale of goods will not change the unit cost of the goods that remain in inventory.

(True/False)

4.9/5 (33)

In periods of rising inventory prices,the LIFO method will result in a higher inventory valuation than will the average-cost method.

(True/False)

4.9/5 (34)

A major criticism of the FIFO method is that it magnifies the effects of the business cycle on business income.

(True/False)

4.9/5 (37)

Which inventory method generally results in the most realistic balance sheet valuation?

(Multiple Choice)

4.8/5 (35)

An overstatement of beginning inventory in a period will result in an overstatement of gross margin in the next period.

(True/False)

4.9/5 (40)

Both the retail method and the gross profit method are useful in estimating the inventory cost.

(True/False)

4.9/5 (40)

Which of the following inventory methods when used for income tax purposes must also be used for reporting purposes?

(Multiple Choice)

4.8/5 (44)

Which costing method will produce different results under perpetual and periodic systems?

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)