Exam 7: Advanced Option Strategies

Exam 1: Introduction29 Questions

Exam 2: Structure of Options Markets55 Questions

Exam 3: Principles of Option Pricing50 Questions

Exam 4: Option Pricing Models: the Binomial Model50 Questions

Exam 5: Option Pricing Models: the Black-Scholes-Merton Model50 Questions

Exam 6: Basic Option Strategies50 Questions

Exam 7: Advanced Option Strategies50 Questions

Exam 8: The Structure of Forward and Futures Markets50 Questions

Exam 9: Principles of Pricing Forwards, Futures, and Options on Futures50 Questions

Exam 10: Futures Arbitrage Strategies48 Questions

Exam 11: Forward and Futures Hedging, Spread, and Target Strategies50 Questions

Exam 12: Swaps50 Questions

Exam 13: Interest Rate Forwards and Options49 Questions

Exam 14: Advanced Derivatives and Strategies50 Questions

Exam 15: Financial Risk Management Techniques and Applications50 Questions

Exam 16: Managing Risk in an Organization50 Questions

Select questions type

The delta of a straddle would be the call delta plus the put delta.

(True/False)

4.8/5  (41)

(41)

At the expiration of a box spread,at most there will be only one option exercised.

(True/False)

4.9/5 (31)

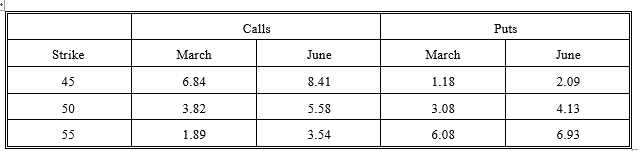

The following prices are available for call and put options on a stock priced at $50. The risk-free rate is 6 percent and the volatility is 0.35. The March options have 90 days remaining and the June options have 180 days remaining. The Black-Scholes model was used to obtain the prices.

Use this information to answer questions 1 through 20. Assume that each transaction consists of one contract (100 options) unless otherwise indicated.

For questions 1 through 6, consider a bull money spread using the March 45/50 calls.

-What is the maximum profit on the spread?

Use this information to answer questions 1 through 20. Assume that each transaction consists of one contract (100 options) unless otherwise indicated.

For questions 1 through 6, consider a bull money spread using the March 45/50 calls.

-What is the maximum profit on the spread?

(Multiple Choice)

5.0/5 (37)

The risk of early exercise is of no concern to the holder of a long straddle.

(True/False)

4.9/5 (33)

Answer questions about a long straddle constructed using the June 50 options.

-What is the profit if the stock price at expiration is at $64.75?

(Multiple Choice)

4.9/5 (44)

If a straddle is closed prior to expiration,the investor can recover some of the time value of either the call or the put but not both.

(True/False)

4.8/5 (30)

A call money spread that is closed prior to expiration has lower losses but higher profits for each stock price than if held to expiration.

(True/False)

4.8/5 (40)

The holder of a straddle does not care which way the market moves as long as it makes a significant move.

(True/False)

4.9/5 (42)

Answer questions about a long straddle constructed using the June 50 options.

-Suppose a put is added to a straddle.This overall transaction is called a strip.Determine the profit at expiration on a strip if the stock price at expiration is $36.

(Multiple Choice)

4.8/5 (39)

A spread that is profitable if the options are in-the-money is called a money spread.

(True/False)

4.7/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)