Exam 3: Principles of Option Pricing

Exam 1: Introduction29 Questions

Exam 2: Structure of Options Markets55 Questions

Exam 3: Principles of Option Pricing50 Questions

Exam 4: Option Pricing Models: the Binomial Model50 Questions

Exam 5: Option Pricing Models: the Black-Scholes-Merton Model50 Questions

Exam 6: Basic Option Strategies50 Questions

Exam 7: Advanced Option Strategies50 Questions

Exam 8: The Structure of Forward and Futures Markets50 Questions

Exam 9: Principles of Pricing Forwards, Futures, and Options on Futures50 Questions

Exam 10: Futures Arbitrage Strategies48 Questions

Exam 11: Forward and Futures Hedging, Spread, and Target Strategies50 Questions

Exam 12: Swaps50 Questions

Exam 13: Interest Rate Forwards and Options49 Questions

Exam 14: Advanced Derivatives and Strategies50 Questions

Exam 15: Financial Risk Management Techniques and Applications50 Questions

Exam 16: Managing Risk in an Organization50 Questions

Select questions type

Which of the following statements about an American call is not true?

Free

(Multiple Choice)

4.7/5  (30)

(30)

Correct Answer: Verified

Verified

D

The gain from the early exercise of an American put is X(1 + r)-T - S0.

Free

(True/False)

4.9/5 (28)

Correct Answer:Verified

False

Another expression for intrinsic value is

Free

(Multiple Choice)

4.9/5 (40)

Correct Answer:Verified

D

High volatility is bad for option holders because it increases the probability that the option will expire out-of-the-money.

(True/False)

4.8/5 (38)

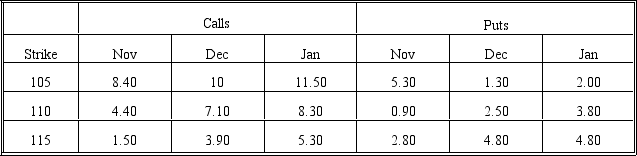

The following quotes were observed for options on a given stock on November 1 of a given year.These are American calls except where indicated.Use the information to answer questions 7 through 20.

The stock price was 113.25.The risk-free rates were 7.30 percent (November),7.50 percent (December)and 7.62 percent (January).The times to expiration were 0.0384 (November),0.1342 (December),and 0.211 (January).Assume no dividends unless indicated.

-What is the intrinsic value of the January 110 call?

The stock price was 113.25.The risk-free rates were 7.30 percent (November),7.50 percent (December)and 7.62 percent (January).The times to expiration were 0.0384 (November),0.1342 (December),and 0.211 (January).Assume no dividends unless indicated.

-What is the intrinsic value of the January 110 call?

(Multiple Choice)

4.7/5 (41)

The difference between a Treasury bill's face value and its price is called the

(Multiple Choice)

4.7/5 (40)

Holding everything else constant,put options are more expensive in periods of high interest rates.

(True/False)

4.9/5 (35)

The time value of a call is greatest when the stock price is very high.

(True/False)

4.8/5 (39)

The lower bound of a European call on a non-dividend paying stock is lower than the intrinsic value of an American call.

(True/False)

4.9/5 (35)

An American call should be exercised early when the stock price is extremely high and is expected to fall.

(True/False)

5.0/5 (37)

The concept of the intrinsic value does not apply to European calls prior to expiration because they cannot be exercised immediately.

(True/False)

4.9/5 (32)

The difference between an American call's price and its intrinsic value is called the time value because the call can be exercised at any time.

(True/False)

4.9/5 (41)

The following quotes were observed for options on a given stock on November 1 of a given year.These are American calls except where indicated.Use the information to answer questions 7 through 20.

The stock price was 113.25.The risk-free rates were 7.30 percent (November),7.50 percent (December)and 7.62 percent (January).The times to expiration were 0.0384 (November),0.1342 (December),and 0.211 (January).Assume no dividends unless indicated.

-What is the time value of the November 115 put?

(Multiple Choice)

4.9/5 (40)

Suppose you knew that the January 115 options were correctly priced but suspected that the stock was mispriced.Using put-call parity,what would you expect the stock price to be? For this problem,treat the options as if they were European.

(Multiple Choice)

4.8/5 (30)

The lower bound of a European put on a non-dividend paying stock is lower than the intrinsic value of an American put.

(True/False)

4.8/5 (37)

On March 2,a Treasury bill expiring on April 20 had a bid discount of 5.80,and an ask discount of 5.86.What is the best estimate of the risk-free rate as given in the text?

(Multiple Choice)

4.8/5 (38)

The spread between the prices of two European puts,alike in all respects except exercise price,cannot exceed the difference in their exercise prices.

(True/False)

4.9/5 (36)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)