Exam 16: Statement of Cash Flows: Another Look

Exam 1: Introduction to Business Activities and Overview of Financial Statements and the Reporting Process139 Questions

Exam 2: The Basics of Record Keeping and Financial Statement Preparation: Balance Sheet115 Questions

Exam 3: The Basics of Record Keeping and Financial Statement Preparation: Income Statement129 Questions

Exam 4: Balance Sheet: Presenting and Analyzing Resources and Financing120 Questions

Exam 5: Income Statement: Reporting Results of Operating Activities109 Questions

Exam 6: Statement of Cash Flows140 Questions

Exam 7: Introduction to Financial Statement Analysis166 Questions

Exam 8: Revenue Recognition, Receivables, and Advances From Customers138 Questions

Exam 9: Working Capital167 Questions

Exam 10: Long-Lived Tangible and Intangible Assets182 Questions

Exam 11: Notes, Bonds, and Leases139 Questions

Exam 12: Liabilities: Off-Balance Sheet Financing, Retirement Benefits, and Income Taxes117 Questions

Exam 13: Marketable Securities and Derivatives144 Questions

Exam 14: Intercorporate Investments in Common Stock103 Questions

Exam 15: Shareholders Equity: Capital Contributions and Distributions199 Questions

Exam 16: Statement of Cash Flows: Another Look146 Questions

Exam 17: Synthesis and Extensions246 Questions

Select questions type

In preparing the statement of cash flows for Year 4, internal records indicate that depreciation on manufacturing facilities totaled $800.The firm included this amount in cost of goods sold in the income statement for Year 4.None of the of depreciation required an operating cash flow during Year 4.The T-account work sheet entry adds back the $800 of depreciation on manufacturing facilities.Accountants treat depreciation charges on manufacturing facilities as

(Multiple Choice)

4.9/5  (45)

(45)

The product life-cycle concept from microeconomics and marketing provides useful insights into the relations among cash flows from operating, investing, and financing activities.Biotechnology firms are in their _____ phase, consumer foods companies are in their _____ phase, and U.S.auto manufacturers are in the _____ phase.

(Multiple Choice)

4.7/5 (37)

The product life-cycle concept from microeconomics and marketing provides useful insights into the relations between cash flows from operating, investing, and financing activities.During the introduction phase

(Multiple Choice)

4.9/5 (34)

The product life-cycle concept from microeconomics and marketing provides useful insights into the relations between cash flows from operating, investing, and financing activities.During the introduction phase

(Multiple Choice)

4.7/5 (33)

The last step in the accounting record-keeping process is preparing the statement of cash flows from balance sheet amounts and from details of transactions affecting the cash account.

(True/False)

4.9/5 (40)

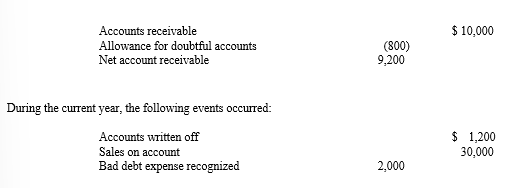

Kendrick Company began the current year with the following:  During the current year, the following events occurred:

1,200 Accounts written off 30,000 Sales on account 2,000 Bad debt expense recognized At the end of the current year, the company showed a balance in gross accounts receivable (before the allowance for doubtful accounts) of $16,800.

What amount would be shown as an operating cash inflow in the statement of cash flows under the indirect method?

During the current year, the following events occurred:

1,200 Accounts written off 30,000 Sales on account 2,000 Bad debt expense recognized At the end of the current year, the company showed a balance in gross accounts receivable (before the allowance for doubtful accounts) of $16,800.

What amount would be shown as an operating cash inflow in the statement of cash flows under the indirect method?

(Multiple Choice)

4.7/5 (30)

Cash flow from ____ activities includes purchases and sales of marketable securities, investments in securities, property, plant, and equipment, and intangibles.

(Multiple Choice)

4.9/5 (35)

Which of the following items involving current trade accounts receivable is most likely to appear in a statement of cash flows?

(Multiple Choice)

4.9/5 (44)

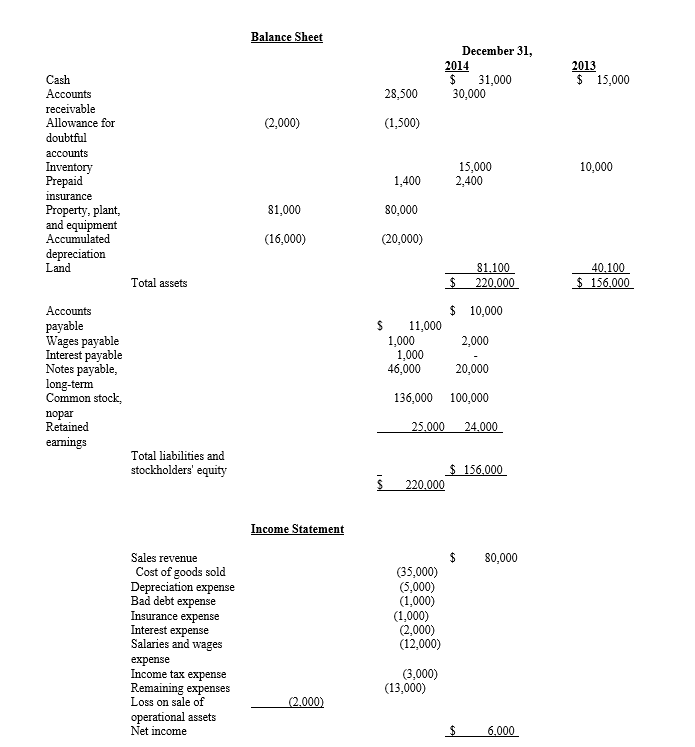

Financial information for Price Company at December 31, 2014, and for the year then ended, are presented below:

Additional information:

1. On December 31, 2013, Newton acquired 25 percent of Trent Corporation’s common stock for $137,500. On that date, the carrying value of Trent’s net assets and liabilities (which approximated fair value) was $550,000. Trent reported income of $60,000 for the year ended December 31, 2014. No dividend was paid on Trent’s common stock during the year.

2. During 2014, Newton loaned $150,000 to Dalton Company, an unrelated entity. Dalton made the first semi-annual principal payment of $15,000, plus interest at 10 percent, on October 1, 2014.

3. On January 2, 2014, Newton sold equipment costing $30,000, with a carrying value of $17,500, for $20,000 cash.

4. On January 2, 2014, Newton entered into a capital lease for an office building. The present value of the annual rental payments is $200,000, which equals the fair value of the building. Newton made the first lease payment of $30,000 when due on January 2, 2015.

5. Newton’s net income for 2014 was $180,000.

6. Newton declared and paid cash dividends for 2014 and 2013 as follows:

Required:

Prepare the statement of cash flows using the indirect method.

Additional information:

1. On December 31, 2013, Newton acquired 25 percent of Trent Corporation’s common stock for $137,500. On that date, the carrying value of Trent’s net assets and liabilities (which approximated fair value) was $550,000. Trent reported income of $60,000 for the year ended December 31, 2014. No dividend was paid on Trent’s common stock during the year.

2. During 2014, Newton loaned $150,000 to Dalton Company, an unrelated entity. Dalton made the first semi-annual principal payment of $15,000, plus interest at 10 percent, on October 1, 2014.

3. On January 2, 2014, Newton sold equipment costing $30,000, with a carrying value of $17,500, for $20,000 cash.

4. On January 2, 2014, Newton entered into a capital lease for an office building. The present value of the annual rental payments is $200,000, which equals the fair value of the building. Newton made the first lease payment of $30,000 when due on January 2, 2015.

5. Newton’s net income for 2014 was $180,000.

6. Newton declared and paid cash dividends for 2014 and 2013 as follows:

Required:

Prepare the statement of cash flows using the indirect method.

(Essay)

4.8/5 (40)

Glass Corporation retired $7,500,000 of long-term debt at maturity.The income statement shows no gain or loss on retirement of debt.The statement of cash flows classifies the transaction as a(n)

(Multiple Choice)

4.8/5 (36)

Discuss the effects of transactions involving derivatives and the fair value option on the statements of cash flows.

(Essay)

4.8/5 (34)

In order to explain the change in the master cash account between the beginning and the end of the period, the accountant reconstructs the entries originally made in the accounts during the period and enters them in appropriate T-accounts on the T-account work sheet.By explaining the changes in balance sheet accounts other than cash, this process also explains the change in

(Multiple Choice)

4.8/5 (46)

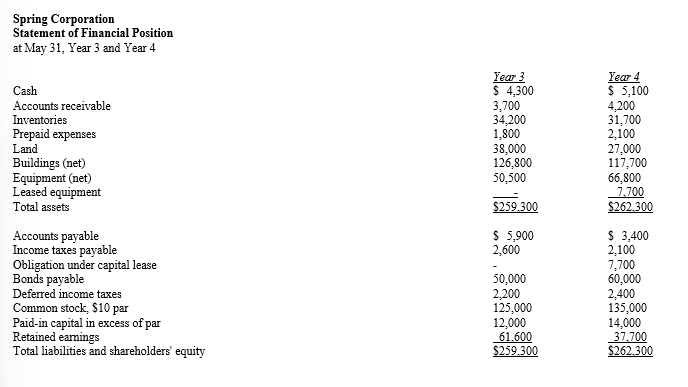

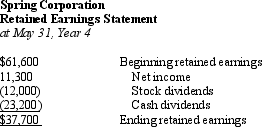

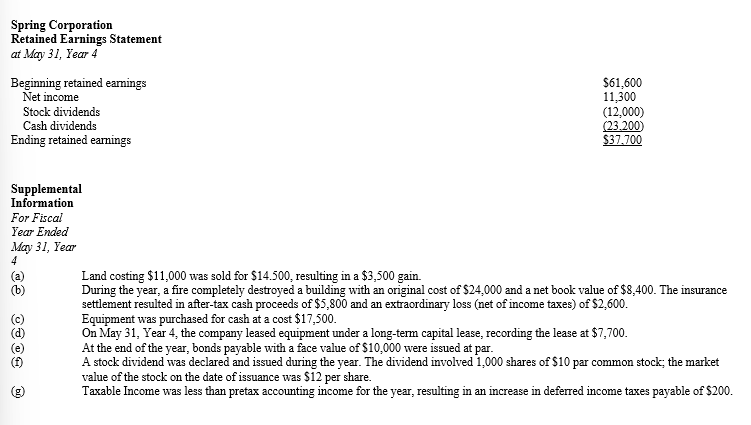

(CMA adapted, Jun 94 #4) Spring Corporation, a public company, has prepared all of its year-end financial statements with the exception of the statement of cash flows.Presented below is condensed financial information for the years ended May 31, Year 3 and Year 4, as well as supplemental data on certain transactions that occurred during the year ended May 31, Year 4.

Required:

Using the indirect method, prepare the Statement of Cash Flows for Spring Corporation for the year ended May 31, Year 4.The statement should comply with the requirements of Statements of Financial Accounting Standards No.95, 'Statement of Cash Flows,' and be supported by appropriate calculations.

Required:

Using the indirect method, prepare the Statement of Cash Flows for Spring Corporation for the year ended May 31, Year 4.The statement should comply with the requirements of Statements of Financial Accounting Standards No.95, 'Statement of Cash Flows,' and be supported by appropriate calculations.

(Essay)

4.8/5 (38)

Most, but not all, firms report cash flows from operations using the indirect method.

(True/False)

4.8/5 (33)

The product life-cycle concept from microeconomics and marketing provides useful insights into the relations between cash flows from operating, investing, and financing activities.During the introduction phase

(Multiple Choice)

5.0/5 (25)

Generally only investments with maturities of _____ months or less qualify as cash equivalents.

(Multiple Choice)

4.9/5 (40)

The product life-cycle concept from microeconomics and marketing provides useful insights into the relations between cash flows from operating, investing, and financing activities.During the maturity phase

(Multiple Choice)

4.8/5 (29)

The product life-cycle concept from microeconomics and marketing provides useful insights into the relations among cash flows from operating, investing, and financing activities.The _____ phase reflects sales of successful products, and net income turns positive.The firm makes more sales, but it also needs to acquire more goods to sell.Because it usually must pay for the goods it acquires before it collects for the goods it sells, the firm finds itself often short of cash from operations.The faster it grows (even though profitable), the more cash it needs.Banks do not like to lend for such needs.They view such needs (even though for current assets) as a permanent part of the firm's financing needs.Thus, banks want firms to use shareholders' equity or long-term debt to finance growth in nonseasonal inventories and receivables.

(Multiple Choice)

4.9/5 (43)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)