Exam 5: Audit Evidence and Documentation

Exam 1: The Role of the Public Accountant in the American Economy45 Questions

Exam 2: Professional Standards62 Questions

Exam 3: Professional Ethics62 Questions

Exam 4: Legal Liability of Cpas56 Questions

Exam 5: Audit Evidence and Documentation82 Questions

Exam 6: Planning the Audit; Linking Audit Procedures to Risk78 Questions

Exam 7: Internal Control92 Questions

Exam 8: Consideration of Internal Control in an Information Technology Environment63 Questions

Exam 9: Audit Sampling83 Questions

Exam 10: Cash and Financial Investments61 Questions

Exam 11: Accounts Receivable, Notes Receivable, and Revenue64 Questions

Exam 12: Inventories and Cost of Goods Sold59 Questions

Exam 13: Property, Plant, and Equipment: Depreciation and Depletion39 Questions

Exam 14: Accounts Payable and Other Liabilities50 Questions

Exam 15: Debt and Equity Capital40 Questions

Exam 16: Auditing Operations and Completing the Audit69 Questions

Exam 17: Auditors Report62 Questions

Exam 18: Integrated Audits of Public Companies43 Questions

Exam 19: Additional Assurance Services: Historical Financial Information60 Questions

Exam 20: Additional Assurance Services: Other Information51 Questions

Exam 21: Internal, Operational, and Compliance Auditing48 Questions

Select questions type

Working papers that record the procedures used by the auditor to gather evidence should be:

(Multiple Choice)

4.8/5  (43)

(43)

Which of the following statements is generally correct about audit evidence?

(Multiple Choice)

4.9/5 (46)

Which of the following is not a typical analytical procedure?

(Multiple Choice)

4.8/5 (33)

Which of the following is true about analytical procedures?

(Multiple Choice)

4.8/5 (34)

The professional standards consider calculating depreciation expense a "routine" transaction.

(True/False)

4.8/5 (33)

Which of the following is not an assertion relating to classes of transactions?

(Multiple Choice)

4.9/5 (35)

The primary purpose of a letter of representations is to obtain additional evidence about specific accounts.

(True/False)

4.9/5 (29)

Adjusting journal entries are ordinarily recorded by the client, while reclassifying journal entries need not be recorded.

(True/False)

4.8/5 (40)

The date on which no information may be deleted from audit documentation is the

(Multiple Choice)

4.9/5 (41)

Which of the following is not considered to be an analytical procedure?

(Multiple Choice)

4.9/5 (38)

Which of the following ultimately determines the specific audit procedures necessary to provide independent auditors with a reasonable basis for the expression of an opinion?

(Multiple Choice)

4.9/5 (35)

The permanent file section of the working papers that is kept for each audit client most likely contains:

(Multiple Choice)

4.8/5 (36)

To be effective, analytical procedures performed near the end of the audit should be performed by

(Multiple Choice)

4.7/5 (30)

Audit documentation should be sufficient to allow which individual to understand the audit work performed, the evidence obtained, and the significant conclusions?

(Multiple Choice)

4.9/5 (34)

Working papers of continuing audit interest usually are filed with the administrative working papers.

(True/False)

4.8/5 (49)

The use of lead schedules is designed to increase the detail of the working trial balance.

(True/False)

4.8/5 (34)

Which of the following is a basic approach often used by auditors to evaluate the reasonableness of accounting estimates?

(Multiple Choice)

4.9/5 (40)

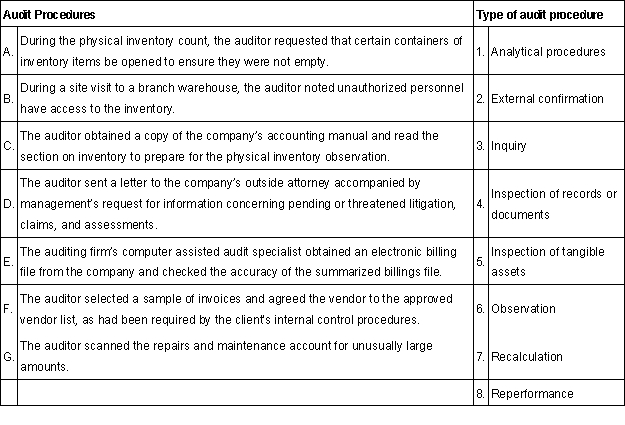

For each of the audit procedures listed below select the type of audit procedure, if any, that the auditor performed. A type of audit procedure may be selected once or not at all.

(Essay)

4.8/5 (36)

Failure to detect material dollar errors in the financial statements is a risk which the auditors primarily mitigate by:

(Multiple Choice)

4.9/5 (36)

The auditors of Smith Electronics wish to limit the audit risk of material misstatement in the test of accounts receivable to 5 percent. They believe that inherent risk is 100%, and there is a 40% risk that material misstatement could have bypassed the client's system of internal control. What is the maximum detection risk the auditors should specify in their substantive procedures of details of accounts receivable?

(Multiple Choice)

4.7/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)