Exam 2: Consolidation of Financial Information

Exam 1: The Equity Method of Accounting for Investments119 Questions

Exam 2: Consolidation of Financial Information115 Questions

Exam 3: Consolidations-Subsequent to the Date of Acquisition120 Questions

Exam 4: Consolidated Financial Statements and Outside Ownership117 Questions

Exam 5: Consolidated Financial Statements - Intra-Entity Asset Transactions127 Questions

Exam 6: Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flo115 Questions

Exam 7: Consolidated Financial Statements - Ownership Patterns and Income118 Questions

Exam 8: Segment and Interim Reporting113 Questions

Exam 9: Foreign Currency Transactions and Hedging Foreign Exchange Risk93 Questions

Exam 10: Translation of Foreign Currency Financial Statements97 Questions

Exam 11: Worldwide Accounting Diversity and International Standards60 Questions

Exam 12: Financial Reporting and the Securities and Exchange Commission77 Questions

Exam 13: Accounting for Legal Reorganizations and Liquidations82 Questions

Exam 14: Partnerships: Formation and Operations88 Questions

Exam 15: Partnerships: Termination and Liquidation70 Questions

Exam 16: Accounting for State and Local Governments78 Questions

Exam 17: Accounting for State and Local Governments46 Questions

Exam 18: Accounting and Reporting for Private Not-For-Profit Organizations62 Questions

Exam 19: Accounting for Estates and Trusts80 Questions

Select questions type

In a transaction accounted for using the acquisition method where consideration transferred exceeds book value of the acquired company, which statement is true for the acquiring company with regard to its investment?

Free

(Multiple Choice)

4.9/5  (40)

(40)

Correct Answer: Verified

Verified

A

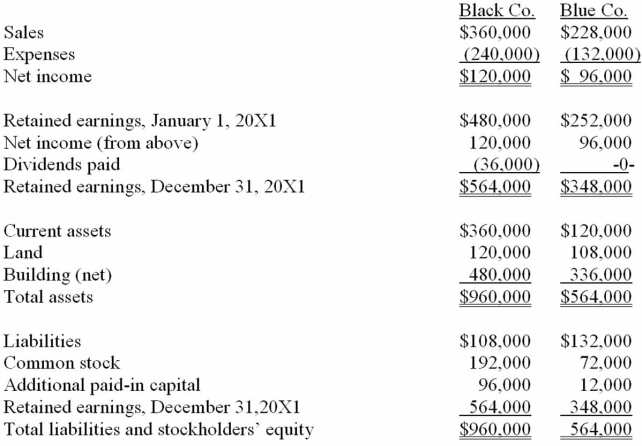

The following are preliminary financial statements for Black Co. and Blue Co. for the year ending December 31, 20X1 prior to Black's acquisition of Blue.  On December 31, 20X1 (subsequent to the preceding statements), Black exchanged 10,000 shares of its $10 par value common stock for all of the outstanding shares of Blue. Black's stock on that date has a fair value of $60 per share. Black was willing to issue 10,000 shares of stock because Blue's land was appraised at $204,000. Black also paid $14,000 to several attorneys and accountants who assisted in creating this combination.

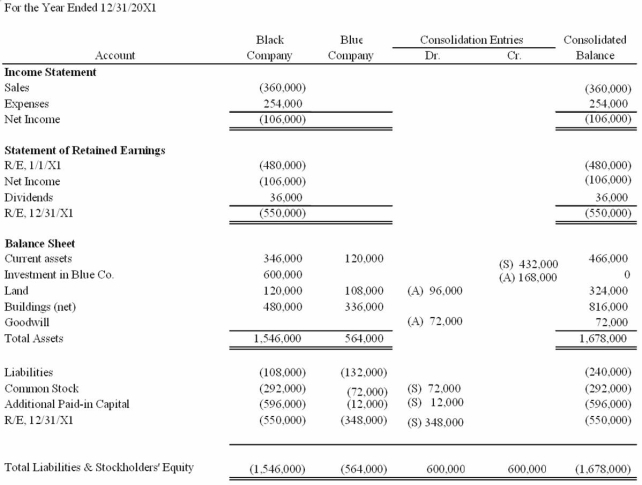

Required: Assuming that these two companies retained their separate legal identities, prepare a consolidation worksheet as of December 31, 20X1 after the acquisition transaction is completed.

On December 31, 20X1 (subsequent to the preceding statements), Black exchanged 10,000 shares of its $10 par value common stock for all of the outstanding shares of Blue. Black's stock on that date has a fair value of $60 per share. Black was willing to issue 10,000 shares of stock because Blue's land was appraised at $204,000. Black also paid $14,000 to several attorneys and accountants who assisted in creating this combination.

Required: Assuming that these two companies retained their separate legal identities, prepare a consolidation worksheet as of December 31, 20X1 after the acquisition transaction is completed.

Free

(Essay)

4.8/5 (32)

Correct Answer:Verified

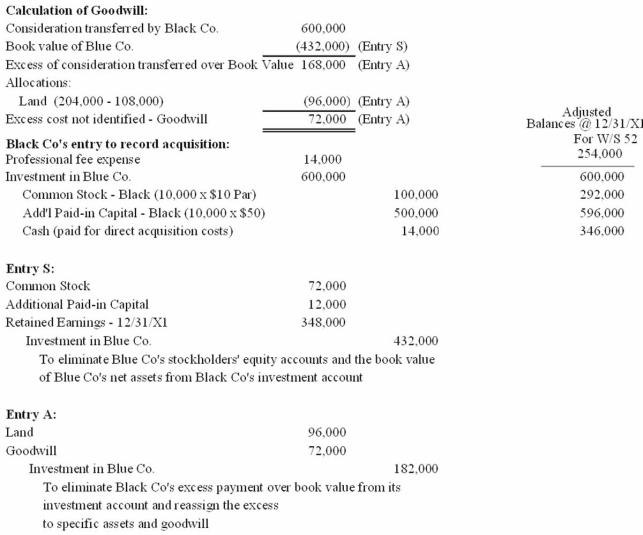

Acquisition Consolidation Worksheet

How are stock issuance costs and direct combination costs treated in a business combination which is accounted for as an acquisition when the subsidiary will retain its incorporation?

Free

(Multiple Choice)

4.8/5 (36)

Correct Answer:Verified

C

Which one of the following is a characteristic of a business combination that is accounted for as an acquisition?

(Multiple Choice)

5.0/5 (30)

Which of the following statements is true regarding a statutory merger?

(Multiple Choice)

4.9/5 (31)

Figure:

Bullen Inc. acquired 100% of the voting common stock of Vicker Inc. on January 1, 20X1. The book value and fair value of Vicker's accounts on that date (prior to creating the combination) follow, along with the book value of Bullen's accounts: Bullen Vicker Vicker Book Book Fair Value Value Value Retained earnings, 1/1/X1 \ 250,000 \ 240,000 Cash and receivables 170,000 70,000 \ 70,000 Inventory 230,000 170,000 210,000 Land 280,000 220,000 240,000 Buildings (net) 480,000 240,000 270,000 Equipment (net) 120,000 90,000 90,000 Liabilities 650,000 430,000 420,000 Common stock 360,000 80,000 Additional paid-in capital 20,000 40,000

-Assume that Bullen issued preferred stock with a par value of $240,000 and a fair value of $500,000 for all of the outstanding shares of Vicker in an acquisition business combination. What will be the balance in the consolidated Inventory and Land accounts?

(Multiple Choice)

4.7/5 (32)

What is the primary accounting difference between accounting for when the subsidiary is dissolved and when the subsidiary retains its incorporation?

(Multiple Choice)

4.8/5 (46)

What is the difference in consolidated results between a business combination whereby the acquired company is dissolved, and a business combination whereby separate incorporation is maintained?

(Essay)

4.9/5 (36)

Jernigan Corp. had the following account balances at 12/1/10: Receivables \ 96,000 Inventory 240,000 Land 720,000 Building 600,000 Liabilities 480,000 Common stock 120,000 Additional paid-in capital 120,000 Retained earnings, 12/1/10 840,000 Revenues 360,000 Expenses 264,000

Several of Jernigan's accounts have fair values that differ from book value. The fair values are: Land - $480,000; Building - $720,000; Inventory - $336,000; and Liabilities - $396,000.

Inglewood Inc. acquired all of the outstanding common shares of Jernigan by issuing 20,000 shares of common stock having a $6 par value, but a $66 fair value. Stock issuance costs amounted to $12,000.

Required: Prepare a fair value allocation and goodwill schedule at the date of the acquisition.

(Essay)

4.8/5 (32)

Elon Corp. obtained all of the common stock of Finley Co., paying slightly less than the fair value of Finley's net assets acquired. How should the difference between the consideration transferred and the fair value of the net assets be treated if the transaction is accounted for as an acquisition?

(Essay)

4.7/5 (39)

Using the acquisition method for a business combination, goodwill is generally defined as:

(Multiple Choice)

4.7/5 (35)

Figure:

On January 1, 20X1, the Moody company entered into a transaction for 100% of the outstanding common stock of Osorio Company. To acquire these shares, Moody issued $400 in long-term liabilities and 40 shares of common stock having a par value of $1 per share but a fair value of $10 per share. Moody paid $20 to lawyers, accountants, and brokers for assistance in bringing about this acquisition. Another $15 was paid in connection with stock issuance costs. Prior to these transactions, the balance sheets for the two companies were as follows: Moody Osorio Cash \ 180 \ 40 Receivables 810 180 Inventories 1,080 280 Land 600 360 Buildings (net) 1,260 440 Equipment (net) 480 100 Accounts payable (450) (80) Long-term liabilities (1,290) (400) Common stock (\ 1 par ) (330) Common stock (\ 20 par ) (240) Additional paid-in capital (1,080) (340) Retained earnings (1,260) (340) Note: Parentheses indicate a credit balance.

In Moody's appraisal of Osorio, three assets were deemed to be undervalued on the subsidiary's books: Inventory by $10, Land by $40, and Buildings by $60.

-Compute the amount of consolidated land at date of acquisition.

(Multiple Choice)

4.8/5 (42)

How are bargain purchases accounted for in an acquisition business transaction?

(Essay)

4.7/5 (38)

Figure:

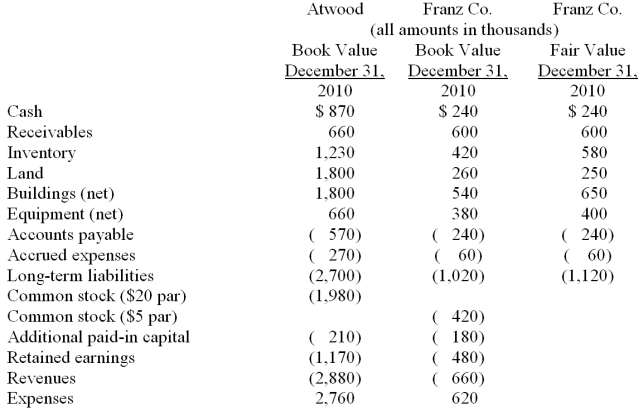

Presented below are the financial balances for the Atwood Company and the Franz Company as of December 31, 2010, immediately before Atwood acquired Franz. Also included are the fair values for Franz Company's net assets at that date.  Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2010. Atwood issued 50 shares of its common stock with a fair value of $35 per share for all of the outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of $10 (in thousands) were paid to effect this acquisition transaction. To settle a difference of opinion regarding Franz's fair value, Atwood promises to pay an additional $5.2 (in thousands) to the former owners if Franz's earnings exceed a certain sum during the next year. Given the probability of the required contingency payment and utilizing a 4% discount rate, the expected present value of the contingency is $5 (in thousands).

-Compute consolidated buildings (net) at date of acquisition.

Note: Parenthesis indicate a credit balance

Assume a business combination took place at December 31, 2010. Atwood issued 50 shares of its common stock with a fair value of $35 per share for all of the outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of $10 (in thousands) were paid to effect this acquisition transaction. To settle a difference of opinion regarding Franz's fair value, Atwood promises to pay an additional $5.2 (in thousands) to the former owners if Franz's earnings exceed a certain sum during the next year. Given the probability of the required contingency payment and utilizing a 4% discount rate, the expected present value of the contingency is $5 (in thousands).

-Compute consolidated buildings (net) at date of acquisition.

(Multiple Choice)

4.9/5 (34)

Figure:

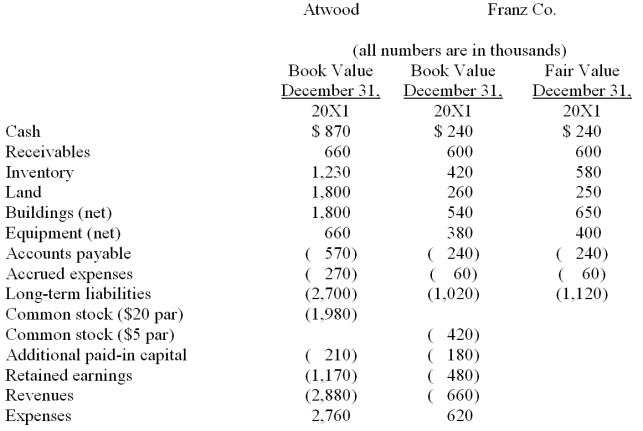

The financial balances for the Atwood Company and the Franz Company as of December 31, 20X1, are presented below. Also included are the fair values for Franz Company's net assets.  Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 20X1. Atwood issued 50 shares of its common stock with a fair value of $35 per share for all of the outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of $10 (in thousands) were paid.

-Compute consolidated buildings (net) at the date of the acquisition.

Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 20X1. Atwood issued 50 shares of its common stock with a fair value of $35 per share for all of the outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of $10 (in thousands) were paid.

-Compute consolidated buildings (net) at the date of the acquisition.

(Multiple Choice)

4.9/5 (30)

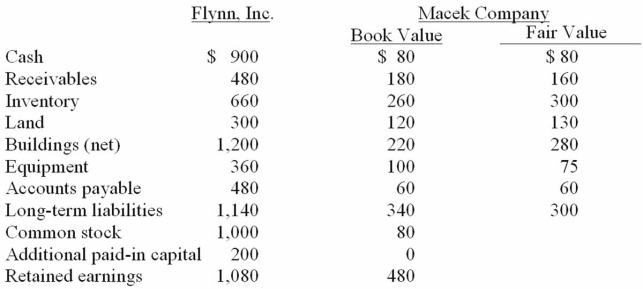

Figure:

Flynn acquires 100 percent of the outstanding voting shares of Macek Company on January 1, 20X1. To obtain these shares, Flynn pays $400 cash (in thousands) and issues 10,000 shares of $20 par value common stock on this date. Flynn's stock had a fair value of $36 per share on that date. Flynn also pays $15 (in thousands) to a local investment firm for arranging the acquisition. An additional $10 (in thousands) was paid by Flynn in stock issuance costs.

The book values for both Flynn and Macek as of January 1, 20X1 follow. The fair value of each of Flynn and Macek accounts is also included. In addition, Macek holds a fully amortized trademark that still retains a $40 (in thousands) value. The figures below are in thousands. Any related question also is in thousands.  -What amount will be reported for consolidated long-term liabilities?

-What amount will be reported for consolidated long-term liabilities?

(Multiple Choice)

4.9/5 (35)

Bale Co. acquired Silo Inc. on December 31, 20X1, in an acquisition business combination transaction. Bale's net income for the year was $1,400,000, while Silo had net income of $400,000 earned evenly during the year. Bale paid $100,000 in direct combination costs, $50,000 in indirect costs, and $30,000 in stock issue costs to effect the combination.

Required: What is consolidated net income for 20X1?

(Essay)

4.9/5 (34)

Describe the accounting for direct costs, indirect costs, and issuance costs under the acquisition method of accounting for a business combination.

(Essay)

4.7/5 (40)

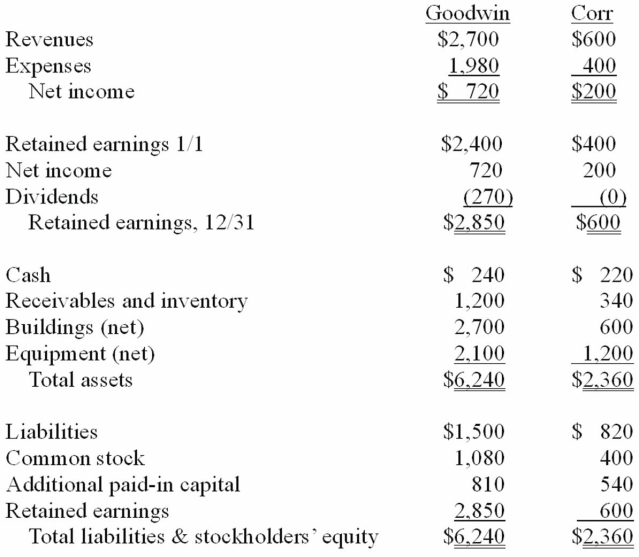

Figure:

The financial statements for Goodwin, Inc., and Corr Company for the year ended December 31, 20X1, prior to Goodwin's acquisition business combination transaction regarding Corr, follow (in thousands):  On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10 par value common stock to the owners of Corr to acquire all of the outstanding shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in stock issuance costs. Corr's equipment was actually worth $1,400 but its buildings were only valued at $560.

-Compute the consolidated common stock account at December 31, 20X1.

On December 31, 20X1, Goodwin issued $600 in debt and 30 shares of its $10 par value common stock to the owners of Corr to acquire all of the outstanding shares of that company. Goodwin shares had a fair value of $40 per share.

Goodwin paid $25 to a broker for arranging the transaction. Goodwin paid $35 in stock issuance costs. Corr's equipment was actually worth $1,400 but its buildings were only valued at $560.

-Compute the consolidated common stock account at December 31, 20X1.

(Multiple Choice)

4.8/5 (36)

Figure:

The financial balances for the Atwood Company and the Franz Company as of December 31, 20X1, are presented below. Also included are the fair values for Franz Company's net assets. Note: Parenthesis indicate a credit balance

Assume an acquisition business combination took place at December 31, 20X1. Atwood issued 50 shares of its common stock with a fair value of $35 per share for all of the outstanding common shares of Franz. Stock issuance costs of $15 (in thousands) and direct costs of $10 (in thousands) were paid.

-Compute consolidated long-term liabilities at the date of the acquisition.

(Multiple Choice)

4.8/5 (42)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)