Exam 22: The Firm: Cost and Output Determination

Exam 1: The Nature of Economics348 Questions

Exam 2: Scarcity and the World of Trade-Offs411 Questions

Exam 3: Demand and Supply451 Questions

Exam 4: Extensions of Demand and Supply Analysis401 Questions

Exam 5: Public Spending and Public Choice362 Questions

Exam 6: Funding the Public Sector201 Questions

Exam 7: The Macroeconomy: Unemployment, Inflation, and Deflation413 Questions

Exam 8: Measuring the Economys Performance416 Questions

Exam 9: Global Economic Growth and Development290 Questions

Exam 10: Real GDP and the Price Level in the Long Run298 Questions

Exam 11: Classical and Keynesian Macro Analyses368 Questions

Exam 12: Consumption, Real GDP, and the Multiplier452 Questions

Exam 13: Fiscal Policy274 Questions

Exam 14: Deficit Spending and the Public Debt146 Questions

Exam 15: Money, Banking, and Central Banking516 Questions

Exam 16: Domestic and International Dimensions of Monetary Policy357 Questions

Exam 17: Stabilization in an Integrated World Economy321 Questions

Exam 18: Policies and Prospects for Global Economic Growth228 Questions

Exam 19: Demand and Supply Elasticity412 Questions

Exam 20: Consumer Choice459 Questions

Exam 21: Rents, Profits, and the Financial Environment of Business445 Questions

Exam 22: The Firm: Cost and Output Determination391 Questions

Exam 23: Perfect Competition432 Questions

Exam 24: Monopoly386 Questions

Exam 25: Monopolistic Competition307 Questions

Exam 26: Oligopoly and Strategic Behavior308 Questions

Exam 27: Regulation and Antitrust Policy in a Globalized Economy310 Questions

Exam 28: The Labor Market: Demand, Supply and Outsourcing376 Questions

Exam 29: Unions and Labor Market Monopoly Power319 Questions

Exam 30: Income, Poverty, and Health Care304 Questions

Exam 31: Environmental Economics299 Questions

Exam 32: Comparative Advantage and the Open Economy282 Questions

Exam 33: Exchange Rates and the Balance of Payments285 Questions

Select questions type

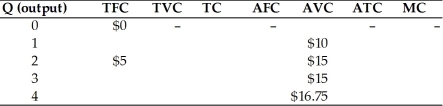

-Using the above table, the TVC, the TC, and MC when output is 3 units are

-Using the above table, the TVC, the TC, and MC when output is 3 units are

(Multiple Choice)

4.9/5  (39)

(39)

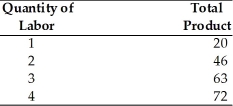

-Refer to the above table. When the quantity of labor equals 3, what does the average product equal?

-Refer to the above table. When the quantity of labor equals 3, what does the average product equal?

(Multiple Choice)

5.0/5 (37)

Increases in long-run average cost that result from output increases is

(Multiple Choice)

4.8/5 (33)

The marginal cost curve always intersects the average total cost curve at the point at which the average total cost curve

(Multiple Choice)

4.7/5 (40)

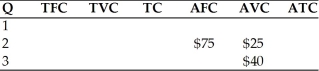

-Refer to the above table. What are total fixed costs at an output of 2 units?

-Refer to the above table. What are total fixed costs at an output of 2 units?

(Multiple Choice)

4.8/5 (42)

Which of the following would NOT be considered a fixed cost of production?

(Multiple Choice)

4.9/5 (34)

The law of diminishing marginal product is NOT responsible for the shape of

(Multiple Choice)

4.9/5 (36)

All of the following are most likely to be fixed costs EXCEPT the cost relating to

(Multiple Choice)

4.8/5 (49)

Suppose that one worker can produce 15 cookies, two workers can produce 40 cookies together, and three workers can produce 75 cookies together. What is the marginal product of the 2nd worker?

(Multiple Choice)

4.8/5 (30)

Which of the following statements is TRUE about the planning horizon?

(Multiple Choice)

4.7/5 (32)

The typical shape of the long-run average cost curve is like

(Multiple Choice)

4.8/5 (38)

-Refer to the above table. What are total variable costs at an output of 2 units?

(Multiple Choice)

4.8/5 (39)

The production function does NOT provide information about

(Multiple Choice)

4.9/5 (36)

The change in output caused by a one-unit change in labor is referred to as the

(Multiple Choice)

4.8/5 (44)

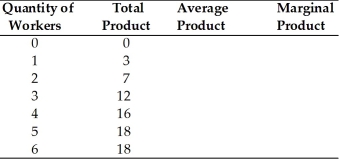

-In the above table, the law of diminishing marginal product sets in after the ________ worker.

-In the above table, the law of diminishing marginal product sets in after the ________ worker.

(Multiple Choice)

4.7/5 (30)

When a company produces 5,000 units, total costs equal $150,000 and total variable costs equal $75,000. At this level of output, what is that company average fixed cost?

(Multiple Choice)

4.8/5 (33)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)