Exam 6: Differential Analysis: the Key to Decision Making

Exam 1: Managerial Accounting and Cost Concepts186 Questions

Exam 2: Cost-Volume-Profit Relationships187 Questions

Exam 3: Job-Order Costing100 Questions

Exam 4: Variable Costing and Segment Reporting: Tools for Management224 Questions

Exam 5: Activity-Based-Costing: a Tool to Aid Decision Making145 Questions

Exam 6: Differential Analysis: the Key to Decision Making174 Questions

Exam 7: Capital Budgeting Decisions167 Questions

Exam 8: Profit Planning172 Questions

Exam 9: Flexible Budgets and Performance Analysis306 Questions

Exam 10: Standard Costs and Variances187 Questions

Exam 11: Performance Measurement in Decentralized Organizations115 Questions

Exam 12: Pricing Products and Services82 Questions

Exam 13: Profitability Analysis76 Questions

Exam 14: Least Squares Regression Computations21 Questions

Exam 15: Activity-Based Absorption Costing12 Questions

Exam 16: the Predetermined Overhead Rate and Capacity28 Questions

Exam 17: Super-Variable Costing49 Questions

Exam 18: Abc Action Analysis16 Questions

Exam 19: the Concept of Present Value13 Questions

Exam 20: Income Taxes and the Net Present Value Method147 Questions

Exam 21: Predetermined Overhead Rates and Overhead Analysis in a Standard Costing System111 Questions

Exam 22: Transfer Pricing25 Questions

Exam 23: Service Department Charges51 Questions

Select questions type

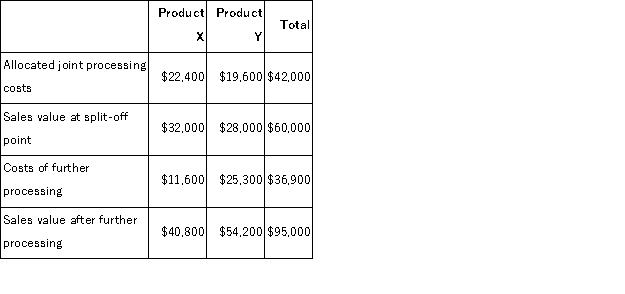

Iaci Company makes two products from a common input.Joint processing costs up to the split-off point total $42, 000 a year.The company allocates these costs to the joint products on the basis of their total sales values at the split-off point.Each product may be sold at the split-off point or processed further.Data concerning these products appear below:  Required:

a.What is the net monetary advantage (disadvantage)of processing Product X beyond the split-off point?

b.What is the net monetary advantage (disadvantage)of processing Product Y beyond the split-off point?

c.What is the minimum amount the company should accept for Product X if it is to be sold at the split-off point?

d.What is the minimum amount the company should accept for Product Y if it is to be sold at the split-off point?

Required:

a.What is the net monetary advantage (disadvantage)of processing Product X beyond the split-off point?

b.What is the net monetary advantage (disadvantage)of processing Product Y beyond the split-off point?

c.What is the minimum amount the company should accept for Product X if it is to be sold at the split-off point?

d.What is the minimum amount the company should accept for Product Y if it is to be sold at the split-off point?

(Essay)

4.8/5  (41)

(41)

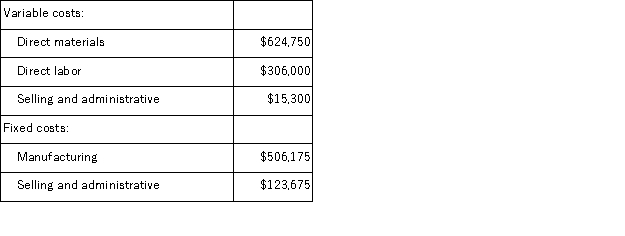

Adamyan Co.manufactures and sells medals for winners of athletic and other events.Its manufacturing plant has the capacity to produce 15, 000 medals each month;current monthly production is 12, 750 medals.The company normally charges $120 per medal.Cost data for the current level of production are shown below:  The company has just received a special one-time order for 700 medals at $83 each.For this particular order, no variable selling and administrative costs would be incurred.This order would also have no effect on fixed costs.

Required:

Should the company accept this special order? Why?

The company has just received a special one-time order for 700 medals at $83 each.For this particular order, no variable selling and administrative costs would be incurred.This order would also have no effect on fixed costs.

Required:

Should the company accept this special order? Why?

(Essay)

4.8/5 (35)

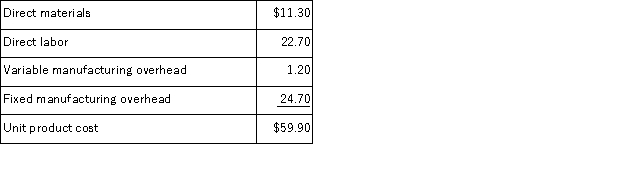

Aholt Corporation makes 40, 000 units per year of a part it uses in the products it manufactures.The unit product cost of this part is computed as follows:  An outside supplier has offered to sell the company all of these parts it needs for $46.20 a unit.If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand.The additional contribution margin on this other product would be $264, 000 per year. If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided.However, $21.90 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier.This fixed manufacturing overhead cost would be applied to the company's remaining products.

What is the maximum amount the company should be willing to pay an outside supplier per unit for the part if the supplier commits to supplying all 40, 000 units required each year?

An outside supplier has offered to sell the company all of these parts it needs for $46.20 a unit.If the company accepts this offer, the facilities now being used to make the part could be used to make more units of a product that is in high demand.The additional contribution margin on this other product would be $264, 000 per year. If the part were purchased from the outside supplier, all of the direct labor cost of the part would be avoided.However, $21.90 of the fixed manufacturing overhead cost being applied to the part would continue even if the part were purchased from the outside supplier.This fixed manufacturing overhead cost would be applied to the company's remaining products.

What is the maximum amount the company should be willing to pay an outside supplier per unit for the part if the supplier commits to supplying all 40, 000 units required each year?

(Multiple Choice)

4.8/5 (38)

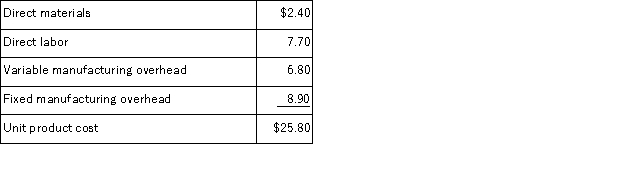

Wiacek Corporation has received a request for a special order of 4, 000 units of product F65 for $26.60 each.Product F65's unit product cost is $25.80, determined as follows:  Direct labor is a variable cost.The special order would have no effect on the company's total fixed manufacturing overhead costs.The customer would like modifications made to product F65 that would increase the variable costs by $3.00 per unit and that would require an investment of $23, 000 in special molds that would have no salvage value. This special order would have no effect on the company's other sales.The company has ample spare capacity for producing the special order.If the special order is accepted, the company's overall net operating income would increase (decrease)by:

Direct labor is a variable cost.The special order would have no effect on the company's total fixed manufacturing overhead costs.The customer would like modifications made to product F65 that would increase the variable costs by $3.00 per unit and that would require an investment of $23, 000 in special molds that would have no salvage value. This special order would have no effect on the company's other sales.The company has ample spare capacity for producing the special order.If the special order is accepted, the company's overall net operating income would increase (decrease)by:

(Multiple Choice)

4.8/5 (30)

A cost that can be avoided by choosing one alternative over another is not relevant for decision purposes.

(True/False)

4.8/5 (37)

Management is considering a one-time-only special order.There is sufficient idle capacity to fill the order without affecting any normal sales.Which one of the following is NOT relevant in making the decision?

(Multiple Choice)

4.8/5 (40)

Palinkas Cane Products Inc. , processes sugar cane in batches.The company buys a batch of sugar cane from farmers for $80 which is then crushed in the company's plant at a cost of $11.Two intermediate products, cane fiber and cane juice, emerge from the crushing process.The cane fiber can be sold as is for $22 or processed further for $10 to make the end product industrial fiber that is sold for $30.The cane juice can be sold as is for $41 or processed further for $27 to make the end product molasses that is sold for $101.How much more profit (loss)does the company make by processing one batch of sugar cane into the end products industrial fiber and molasses?

(Multiple Choice)

4.8/5 (34)

Fixed costs may or may not be relevant in decisions about whether a product should be dropped.

(True/False)

4.9/5 (35)

In a decision to drop a segment, the opportunity cost of the space occupied by the segment is the cost of renting or building similar space nearby.

(True/False)

5.0/5 (36)

Eliminating nonproductive processing time is particularly important in work stations that do not contain bottlenecks.

(True/False)

4.8/5 (33)

When a multi-product factory operates at full capacity, decisions must be made about which products to emphasize.In making such decisions, products should be ranked based on:

(Multiple Choice)

4.8/5 (45)

A study has been conducted to determine if one of the departments in Barry Corporation should be discontinued.The contribution margin in the department is $60, 000 per year.Fixed expenses charged to the department are $75, 000 per year.It is estimated that $34, 000 of these fixed expenses could be eliminated if the department is discontinued.These data indicate that if the department is discontinued, the company's overall net operating income would:

(Multiple Choice)

4.9/5 (45)

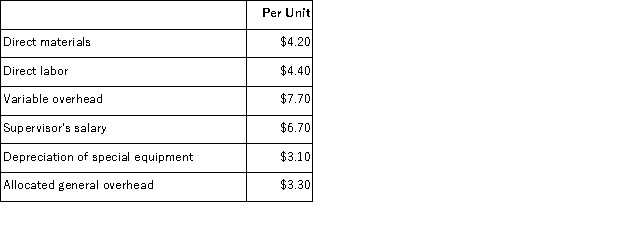

Hermenegildo Corporation is presently making part P42 that is used in one of its products.A total of 10, 000 units of this part are produced and used every year.The company's Accounting Department reports the following costs of producing the part at this level of activity:  An outside supplier has offered to produce and sell the part to the company for $23.90 each.If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted, only $4, 000 of these allocated general overhead costs would be avoided. In addition to the facts given above, assume that the space used to produce part P42 could be used to make more of one of the company's other products, generating an additional segment margin of $13, 000 per year for that product.What would be the impact on the company's overall net operating income of buying part P42 from the outside supplier and using the freed space to make more of the other product?

An outside supplier has offered to produce and sell the part to the company for $23.90 each.If this offer is accepted, the supervisor's salary and all of the variable costs, including direct labor, can be avoided.The special equipment used to make the part was purchased many years ago and has no salvage value or other use.The allocated general overhead represents fixed costs of the entire company.If the outside supplier's offer were accepted, only $4, 000 of these allocated general overhead costs would be avoided. In addition to the facts given above, assume that the space used to produce part P42 could be used to make more of one of the company's other products, generating an additional segment margin of $13, 000 per year for that product.What would be the impact on the company's overall net operating income of buying part P42 from the outside supplier and using the freed space to make more of the other product?

(Multiple Choice)

4.9/5 (42)

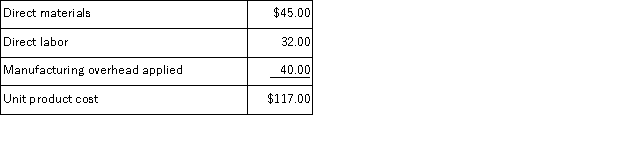

Bulan Inc.makes a range of products.The company's predetermined overhead rate is $20 per direct labor-hour, which was calculated using the following budgeted data:  Component T6 is used in one of the company's products.The unit product cost of the component according to the company's cost accounting system is determined as follows:

Component T6 is used in one of the company's products.The unit product cost of the component according to the company's cost accounting system is determined as follows:  An outside supplier has offered to supply component T6 for $101 each.The outside supplier is known for quality and reliability.Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by this decision.Bulan chronically has idle capacity.

Required:

Is the offer from the outside supplier financially attractive? Why?

An outside supplier has offered to supply component T6 for $101 each.The outside supplier is known for quality and reliability.Assume that direct labor is a variable cost, variable manufacturing overhead is really driven by direct labor-hours, and total fixed manufacturing overhead would not be affected by this decision.Bulan chronically has idle capacity.

Required:

Is the offer from the outside supplier financially attractive? Why?

(Essay)

4.9/5 (38)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)