Exam 3: A Costing Framework and Cost Allocation

Exam 1: The Role of Accounting Information in Management Decision Making53 Questions

Exam 2: Cost Concepts, Behaviour and Estimation71 Questions

Exam 3: A Costing Framework and Cost Allocation68 Questions

Exam 4: Costvolumeprofit Cvp Analysis66 Questions

Exam 5: Planning Budgeting and Behaviour70 Questions

Exam 6: Operational Budgets69 Questions

Exam 7: Job Costing Systems72 Questions

Exam 8: Process Costing Systems67 Questions

Exam 9: Absorption and Variable Costing69 Questions

Exam 10: Flexible Budgets, Standard Costs and Variance Analysis69 Questions

Exam 11: Variance Analysis: Revenue and Cost68 Questions

Exam 12: Activity Analysis: Costing and Management63 Questions

Exam 13: Relevant Costs for Decision Making71 Questions

Exam 14: Strategy and Control72 Questions

Exam 15: Capital Budgeting and Strategic Investment Decisions58 Questions

Exam 16: The Strategic Management of Costs and Revenues55 Questions

Exam 17: Strategic Management Control: a Lean Perspective54 Questions

Exam 18: Responsibility Accounting, Performance Evaluation and Transfer Pricing50 Questions

Exam 19: The Balanced Scorecard and Strategy Maps54 Questions

Select questions type

The Bristol Company uses a job-order cost system. The following data were recorded for June:

Overhead is charged to production at 80% of direct materials cost. Jobs 235, 237, and 238 were completed during June and transferred to finished goods. Jobs 235 and 238 have been delivered to customers. Bristol's Work in Process Stock balance on June 30 was:

June 1 Added During June Work in Process Direct Direct

Job Number Stock Materials Labour 235 £2,500 £600 £400 236 £1,500 £800 £1,000 237 £1,000 £1,200 £1,750 238 £800 £1,500 £2,250

(Multiple Choice)

4.8/5  (38)

(38)

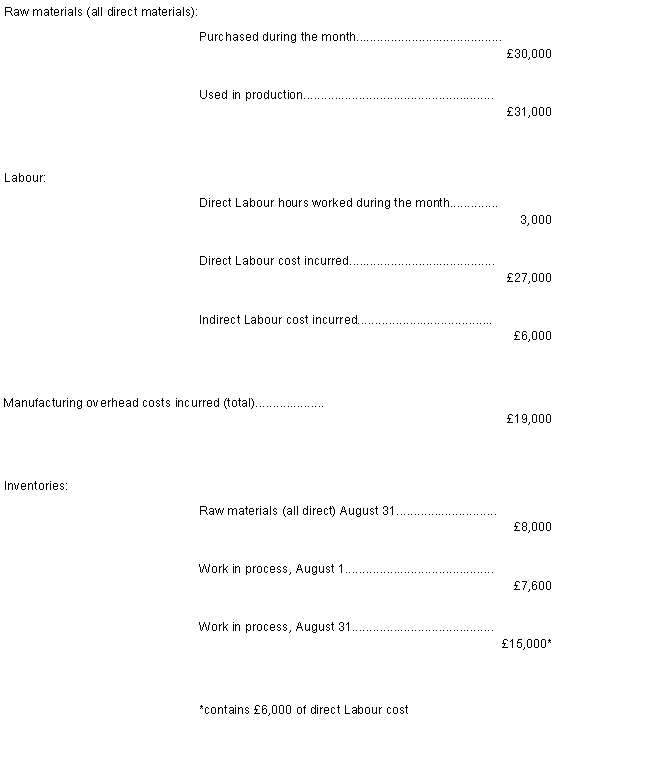

Loraine Company applies manufacturing overhead to jobs using a predetermined overhead rate of 70% of direct Labour cost. Any under- or overapplied overhead cost is closed to Cost of Goods Sold at the end of the month. During August, the following transactions were recorded by the company: -The balance on August 1 in the Raw Materials Stock account was:

-The balance on August 1 in the Raw Materials Stock account was:

(Multiple Choice)

4.8/5 (44)

The following journal entry would be made to apply overhead cost to jobs in a job-order costing system:

Manufacturing Overhead. xxx Work in Process. xxx

(True/False)

4.8/5 (39)

Precision Company data: Actual manufacturing overhead cost incurred £84,000 Actual direct Labour hours worked 27,000

Precision Company used a predetermined overhead rate last year of £3 per direct Labour hour, based on an estimate of 24,000 direct Labour hours to be worked during the year.

The under- or overapplied overhead for the year was:

(Multiple Choice)

4.8/5 (37)

Using the various documents used, outline how a job costing system works.

(Essay)

4.9/5 (36)

An averaging process is used to compute unit product costs under which of the following costing method(s)

(Multiple Choice)

4.8/5 (42)

In a job order cost system using predetermined manufacturing overhead rates, indirect materials issued into production usually are recorded as an increase in

(Multiple Choice)

4.9/5 (38)

The Bristol Company uses a job-order cost system. The following data were recorded for June: June 1 Added During June Work in Process Direct Direct

Job Number Stock Materials Labour 235 £2,500 £600 £400 236 £1,500 £800 £1,000 237 £1,000 £1,200 £1,750 238 £800 £1,500 £2,250

In the previous question overhead is charged to production at 80% of direct materials cost. Jobs 235, 237, and 238 were completed during June and transferred to finished goods. Jobs 235 and 238 have been delivered to customers.

Assume that the company wants to recalculate the overhead rate and now wants to charge overhead to production at 75% of direct material cost. Bristol Company's cost of goods sold for June would change to:

(Multiple Choice)

4.8/5 (40)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)