Exam 11: Variance Analysis: Revenue and Cost

Exam 1: The Role of Accounting Information in Management Decision Making53 Questions

Exam 2: Cost Concepts, Behaviour and Estimation71 Questions

Exam 3: A Costing Framework and Cost Allocation68 Questions

Exam 4: Costvolumeprofit Cvp Analysis66 Questions

Exam 5: Planning Budgeting and Behaviour70 Questions

Exam 6: Operational Budgets69 Questions

Exam 7: Job Costing Systems72 Questions

Exam 8: Process Costing Systems67 Questions

Exam 9: Absorption and Variable Costing69 Questions

Exam 10: Flexible Budgets, Standard Costs and Variance Analysis69 Questions

Exam 11: Variance Analysis: Revenue and Cost68 Questions

Exam 12: Activity Analysis: Costing and Management63 Questions

Exam 13: Relevant Costs for Decision Making71 Questions

Exam 14: Strategy and Control72 Questions

Exam 15: Capital Budgeting and Strategic Investment Decisions58 Questions

Exam 16: The Strategic Management of Costs and Revenues55 Questions

Exam 17: Strategic Management Control: a Lean Perspective54 Questions

Exam 18: Responsibility Accounting, Performance Evaluation and Transfer Pricing50 Questions

Exam 19: The Balanced Scorecard and Strategy Maps54 Questions

Select questions type

The master budget is a network consisting of many separate budgets that are interdependent

Free

(True/False)

4.8/5  (44)

(44)

Correct Answer: Verified

Verified

True

Noskey Corporation is a merchandising firm. Information pertaining to the company's sales revenue is presented in the following table. June July August (Actual) (Budged) (Budget) Cash sales. £80,000 £100,000 £60,000 Credit sales. Total sales.

Management estimates that 5% of credit sales are uncollectible. Of the credit sales that are collectible, 60% are collected in the month of sale and the remainder in the month following the sale. Purchases of inventory are equal to next month's cost of goods sold. The cost of goods sold is 30% of the selling price. All purchases of inventory are on account; 25% are paid in the month of purchase, and the remainder is paid in the month following the purchase.

- Noskey Corporation's budgeted total cash payments in July for inventory purchases are

Free

(Multiple Choice)

4.9/5 (42)

Correct Answer:Verified

B

Berol Company plans to sell 200,000 units of finished product in July and anticipates a growth rate in sales of 5% per month. The desired monthly ending inventory in units of finished product is 80% of the next month's estimated sales. There are 150,000 finished units in inventory on June 30.

Berol Company's production requirement in units of finished product for the three-month period ending September 30 is

Free

(Multiple Choice)

4.8/5 (38)

Correct Answer:Verified

D

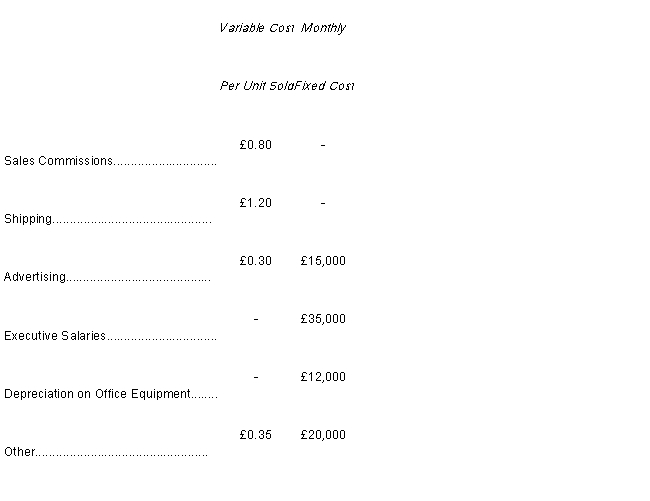

The International Company makes and sells only one product. There are 2 divisions, one in France and one in Newcastle.

The company is in the process of preparing its Selling and Administrative Expense Budget for the last half of the year. The following budget data are available:

French Division Cost Structure

Newcastle Division Cost Structure

Newcastle Division Cost Structure

- All of these expenses (except depreciation) are paid in cash in the month they are incurred. If the budgeted cash disbursements for selling and administrative expenses for November total £154,180, how many units does the Newcastle Division plan to sell in November (rounded to the nearest whole unit)

- All of these expenses (except depreciation) are paid in cash in the month they are incurred. If the budgeted cash disbursements for selling and administrative expenses for November total £154,180, how many units does the Newcastle Division plan to sell in November (rounded to the nearest whole unit)

(Multiple Choice)

4.7/5 (38)

Zero-based budgeting requires managers to justify all costs of programs as if these programs were being proposed for the first time

(True/False)

4.8/5 (36)

The production budget is typically prepared prior to the sales budget

(True/False)

4.9/5 (34)

Self-imposed budgets are those that are prepared by top management and then assigned to other managers within the organisation

(True/False)

4.9/5 (46)

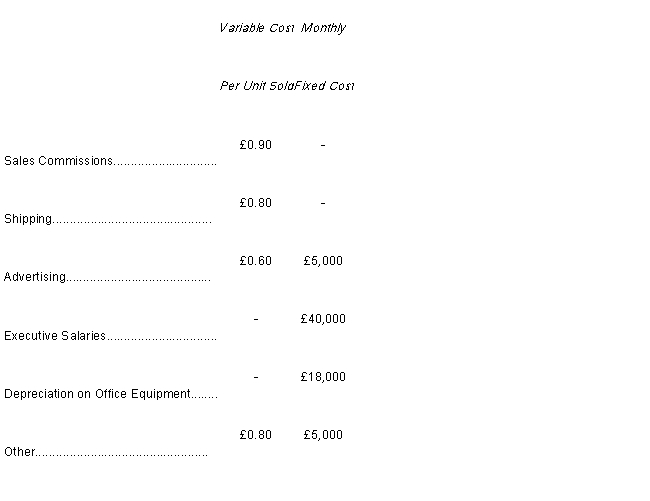

The International Company makes and sells only one product. There are 2 divisions, one in France and one in Newcastle.

The company is in the process of preparing its Selling and Administrative Expense Budget for the last half of the year. The following budget data are available:

French Division Cost Structure

Newcastle Division Cost Structure

-

All of these expenses (except depreciation) are paid in cash in the month they are incurred. If the French Division budgeted to sell 25,000 units in July, then the total budgeted selling and administrative expenses per unit sold for July is

(Multiple Choice)

4.7/5 (40)

The Khaki Company has the following budgeted sales data: January February March April Credit Sales £400,000 £350,000 £300,000 £320,000 Cash Sales £70,000 £90,000 £80,000 £70,000

The regular pattern of collection of credit sales is 40% in the month of sale, 50% in the month following sale, and the remainder in the second month following the month of sale. There are no bad debts. The budgeted cash receipts for April would be

(Multiple Choice)

4.9/5 (37)

The International Company makes and sells only one product. There are 2 divisions, one in France and one in Newcastle.

The company is in the process of preparing its Selling and Administrative Expense Budget for the last half of the year. The following budget data are available:

French Division Cost Structure

Newcastle Division Cost Structure

- All of these expenses (except depreciation) are paid in cash in the month they are incurred. If the budgeted disbursements (including depreciation) for selling and administrative expenses for November total £154,180, how many units does the Newcastle Division plan to sell in November (rounded to the nearest whole unit)

(Multiple Choice)

4.7/5 (31)

Cash Sales Credit Sales January £80,000 £350,000 February 60,000 200,000 March 50,000 145,000 April 45,000 130,000 May 55,000 170,000 June 50,000 150,000 The company is in the process of preparing a cash budget and must determine the expected cash collections by month. To this end, the following information has been assembled:Collections on credit sales:

in month of sale

in month following sale

in second month following sale

-

Assume that the accounts receivable balance on January 1 is £70,000. Of this amount, £60,000 represents uncollected December sales and £10,000 represents uncollected November sales. Given these data, the total cash collected during January would be

(Multiple Choice)

4.8/5 (33)

The Kafusi Company has the following budgeted sales: April May June July Credit Sales £320,000 £300,000 £350,000 £400,000 Cash Sales £70,000 £80,000 £90,000 £70,000

The regular pattern of collection of credit sales is 30% in the month of sale, 60% in the month following the month of sale, and the remainder in the second month following the month of sale. There are no bad debts.

- The budgeted cash receipts for July would be

(Multiple Choice)

4.7/5 (34)

The Kafusi Company has the following budgeted sales: April May June July Credit Sales £320,000 £300,000 £350,000 £400,000 Cash Sales £70,000 £80,000 £90,000 £70,000

The regular pattern of collection of credit sales is 30% in the month of sale, 60% in the month following the month of sale, and the remainder in the second month following the month of sale. There are no bad debts.

- The budgeted accounts receivable balance on May 31 would be

(Multiple Choice)

4.8/5 (37)

Noskey Corporation is a merchandising firm. Information pertaining to the company's sales revenue is presented in the following table. June July August (Actual) (Budged) (Budget) Cash sales. £80,000 £100,000 £60,000 Credit sales. Total sales.

Management estimates that 5% of credit sales are uncollectible. Of the credit sales that are collectible, 60% are collected in the month of sale and the remainder in the month following the sale. Purchases of inventory are equal to next month's cost of goods sold. The cost of goods sold is 30% of the selling price. All purchases of inventory are on account; 25% are paid in the month of purchase, and the remainder is paid in the month following the purchase.

-Noskey Corporation's budgeted cash collections in July from June credit sales are

(Multiple Choice)

4.8/5 (36)

One difficulty with self-imposed budgets is that they are not subject to any type of review

(True/False)

4.8/5 (36)

Shown below is the sales forecast for Cooper Inc. for the first four months of the coming year. Jan Feb Mar Apr Cash Sales £15,000 £24,000 £18,000 £14,000 Credit Sales £100,000 £120,000 £90,000 £70,000

On average, 50% of credit sales are paid for in the month of the sale, 30% in the month following sale, and the remainder is paid two months after the month of the sale. Assuming there are no bad debts, the expected cash inflow in March is

(Multiple Choice)

4.8/5 (33)

The Adams Company, a merchandising firm, has budgeted its activity for November according to the following information:* Sales at , all for cash

* Merchandise inventory on October 31 was .

* The cash balance November 1 was .

* Selling and administrative expenses are budgeted at for November and are paid for in cash.

* Budgeted depreciation for Nowember is .

* The planned merchandise inventory on November 31 is .

* The cost of goods sold is of the selling price.

* All purchases are paid for in cash.

-

The budgeted cash receipts for November are

(Multiple Choice)

4.8/5 (43)

Both variable and fixed manufacturing overhead costs are included in the manufacturing overhead budget

(True/False)

4.8/5 (34)

Cash Sales Credit Sales July £50,000 £150,000 August. 55,000 170,000 September 45,000 130,000 October 50,000 145,000 November 60,000 200,000 December 80,000 350,000

The company is in the process of preparing a cash budget and must determine the expected cash collections by month. To this end, the following information has been assembled:Collections on credit sales:

in month of sale

in month following sale

in second month following sale

-

Assume that the accounts receivable balance on July 1 was £75,000. Of this amount, £60,000 represented uncollected June sales and £15,000 represented uncollected May sales. Given these data, the total cash collected during July would be

(Multiple Choice)

4.9/5 (42)

The International Company makes and sells only one product. There are 2 divisions, one in France and one in Newcastle.

The company is in the process of preparing its Selling and Administrative Expense Budget for the last half of the year. The following budget data are available:

French Division Cost Structure

Newcastle Division Cost Structure

- All of these expenses (except depreciation) are paid in cash in the month they are incurred. If the Newcastle Division has budgeted to sell 24,000 units in September, then the total budgeted fixed selling and administrative expenses for September would be

(Multiple Choice)

4.7/5 (34)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)