Exam 33: Producer Theory With Isoquants

Exam 1: The Central Idea154 Questions

Exam 2: Observing and Explaining the Economy107 Questions

Exam 3: The Supply and Demand Model170 Questions

Exam 4: Subtleties of the Supply and Demand Model: Price Floors,price Ceilings,and Elasticity181 Questions

Exam 5: The Demand Curve and the Behavior of Consumers136 Questions

Exam 6: The Supply Curve and the Behavior of Firms182 Questions

Exam 7: The Interaction of People in Markets158 Questions

Exam 8: Costs and the Changes at Firms Over Time172 Questions

Exam 9: The Rise and Fall of Industries139 Questions

Exam 10: Monopoly183 Questions

Exam 11: Product Differentiation, monopolistic Competition, and Oligopoly169 Questions

Exam 12: Antitrust Policy and Regulation152 Questions

Exam 13: Labor Markets179 Questions

Exam 14: Taxes, transfers, and Income Distribution180 Questions

Exam 15: Public Goods, externalities, and Government Behavior198 Questions

Exam 16: Capital and Financial Markets173 Questions

Exam 17: Macroeconomics: the Big Picture152 Questions

Exam 18: Measuring the Production, income, and Spending of Nations160 Questions

Exam 19: The Spending Allocation Model168 Questions

Exam 20: Unemployment and Employment207 Questions

Exam 21: Productivity and Economic Growth158 Questions

Exam 22: Money and Inflation149 Questions

Exam 23: The Nature and Causes of Economic Fluctuations162 Questions

Exam 24: The Economic Fluctuations Model207 Questions

Exam 25: Using the Economic Fluctuations Model177 Questions

Exam 26: Fiscal Policy137 Questions

Exam 27: Monetary Policy168 Questions

Exam 28: Economic Growth and Globalization162 Questions

Exam 29: International Trade248 Questions

Exam 30: International Finance123 Questions

Exam 31: Reading,understanding,and Creating Graphs34 Questions

Exam 32: Consumer Theory With Indifference Curves39 Questions

Exam 33: Producer Theory With Isoquants19 Questions

Exam 34: Present Discounted Value16 Questions

Exam 35: The Miracle of Compound Growth11 Questions

Exam 36:Deriving the Growth Accounting Formula13 Questions

Exam 37: Deriving the Formula for the Keynesian Multiplier and the Forward-Looking Consumption Model28 Questions

Select questions type

The slope of an isocost line is constant.

Free

(True/False)

4.9/5  (25)

(25)

Correct Answer: Verified

Verified

True

The slope of an isocost line depends on the ratio of

Free

(Multiple Choice)

4.9/5 (40)

Correct Answer:Verified

B

If a profit-maximizing firm is producing at the tangency between an isoquant and an isocost line,then a movement along the current isocost line

(Multiple Choice)

4.8/5 (37)

Suppose the wage rate is $20 and the price of capital is $100.Graph the isocost line for a firm with a total cost of $400.What happens to the isocost line if the price of capital goes up to $200? Graph this isocost line,assuming that the firm maintains a total cost of $400.What happens to production in this case?

(Essay)

4.9/5 (24)

Sketch a typical isocost line and isoquant where a firm is minimizing total cost for a given quantity of output.Suppose the price of labor rises and the price of capital doesn't change.What does the firm do to maintain the original level of output? How does its input use change?

(Essay)

4.9/5 (33)

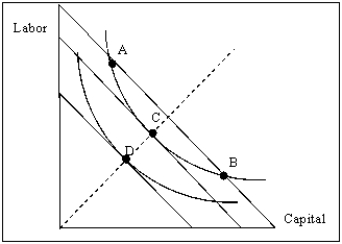

Exhibit 8A-1  -Refer to Exhibit 8A-1.A cost-minimizing firm would prefer producing at point C to producing at

-Refer to Exhibit 8A-1.A cost-minimizing firm would prefer producing at point C to producing at

(Multiple Choice)

4.7/5 (35)

A line that illustrates all the different combinations of two inputs that result in the same total cost is called a(n)

(Multiple Choice)

4.8/5 (22)

An isoquant indicates different combinations of outputs that can be used to yield the same amount of profits.

(True/False)

4.8/5 (31)

We are looking at a graph with capital on the vertical axis and labor on the horizontal axis.If the price of labor increases,then the

(Multiple Choice)

4.7/5 (39)

A firm that maximizes output for a specific total cost is producing at the point where the isocost line is above the highest isoquant.

(True/False)

4.9/5 (30)

In a given isocost line,any combination of different inputs results in the same total cost.

(True/False)

4.9/5 (38)

Explain the similarities and differences between consumer choice theory and producer theory.More specifically,explain how a budget line and indifference curve are related to an isocost line and isoquant,and explain the importance of the tangency point.

(Essay)

4.9/5 (37)

The combination of two inputs that results in a given quantity of output at least cost occurs where

(Multiple Choice)

4.7/5 (37)

A firm can minimize the total costs of producing a given output level at the point of tangency between an isoquant and the isocost line.

(True/False)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)