Exam 29: Consolidation: Non-Controlling Interest

Exam 1: Accounting Regulation and the Conceptual Framework21 Questions

Exam 2: Application of Accounting Theory30 Questions

Exam 3: Fair Value Measurement29 Questions

Exam 4: Inventories30 Questions

Exam 5: Property, Plant and Equipment27 Questions

Exam 6: Intangible Assets24 Questions

Exam 7: Impairment of Assets23 Questions

Exam 8: Provisions, Contingent Liabilities and Contingent Assets27 Questions

Exam 9: Employee Benefits28 Questions

Exam 10: Leases24 Questions

Exam 11: Financial Instruments21 Questions

Exam 12: Income Taxes22 Questions

Exam 13: Share Capital and Reserves29 Questions

Exam 14: Share-Based Payment24 Questions

Exam 15: Revenue23 Questions

Exam 16: Presentation of Financial Statements25 Questions

Exam 17: Statement of Cash Flows29 Questions

Exam 18: Accounting Policies and Other Disclosures14 Questions

Exam 19: Earnings Per Share19 Questions

Exam 20: Operating Segments20 Questions

Exam 21: Related Party Disclosures27 Questions

Exam 22: Sustainability and Corporate Social Responsibility Reporting17 Questions

Exam 23: Foreign Currency Transactions and Forward Exchange Contracts20 Questions

Exam 24: Translation of Foreign Currency Financial Statements18 Questions

Exam 25: Business Combinations23 Questions

Exam 26: Consolidation: Controlled Entities40 Questions

Exam 27: Consolidation: Wholly Owned Entities48 Questions

Exam 28: Consolidation: Intragroup Transactions40 Questions

Exam 29: Consolidation: Non-Controlling Interest51 Questions

Exam 30: Consolidation: Other Issues28 Questions

Exam 31: Associates and Joint Ventures26 Questions

Exam 32: Joint Arrangements26 Questions

Exam 33: Insolvency and Liquidation40 Questions

Exam 34: Accounting for Mineral Resources24 Questions

Exam 35: Agriculture27 Questions

Select questions type

If a gain on bargain purchase arises on a business combination, the non-controlling interest:

Free

(Multiple Choice)

4.8/5  (34)

(34)

Correct Answer: Verified

Verified

B

A Ltd holds a 60% interest in B Ltd. B Ltd sells inventory to A Ltd during the year for $10 000. The inventories originally cost $7 000 when purchased from an external party. At the end of the year all inventories are still on hand. The tax rate is 30%. The NCI adjustment to this intragroup transaction is a debit to NCI of:

Free

(Multiple Choice)

4.9/5 (28)

Correct Answer:Verified

B

Changes in equity in the current period that must be identified for the step 3 NCI entry include:

Free

(Multiple Choice)

4.9/5 (37)

Correct Answer:Verified

D

Company A Limited owns 90% of the share capital of Company B Limited. Company B Limited paid a dividend of $20 000 during the financial period. The NCI adjustment entries in the consolidation worksheet for the dividend include:

(Multiple Choice)

4.9/5 (36)

Xin Limited paid $12 000 for 75% of the shares in Yan Limited. At the date of acquisition Yan Limited had equity as follows:

Share capital $10 000

Retained earnings $5 000

Other reserves $3 000

All of Yan Limited's assets and liabilities were recorded at fair value. The fair value of identifiable net assets acquired by Xin Limited amounted to:

(Multiple Choice)

4.9/5 (33)

When preparing a set of consolidated financial statements, the pre-acquisition entry relates to:

(Multiple Choice)

4.9/5 (44)

A non-controlling interest in a subsidiary entity is entitled to a share of the following items:

(Multiple Choice)

4.8/5 (37)

Jiminez Limited acquired 80% of the shares in Mustang Limited for $150 000. At acquisition date, share capital in Mustang was $150 000 and reserves amounted to $50 000. All assets and liabilities of Mustang were recorded at fair value at acquisition date. The partial goodwill method is adopted by the group. If the company tax rate was 30%, the NCI will recognise a gain on bargain purchase of:

(Multiple Choice)

4.9/5 (38)

Non-controlling interest is classified, according to AASB 10 Consolidated Financial Statements, as:

(Multiple Choice)

4.7/5 (40)

When presenting a consolidated statement of financial position the non-controlling interest is:

(Multiple Choice)

4.8/5 (36)

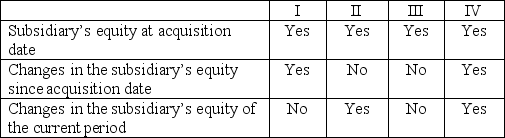

A non-controlling interest is entitled to a share of which of the following items?

I Equity of the group entity at acquisition date.

II Current period profit or loss of the subsidiary entity.

III Changes in equity of the subsidiary since acquisition date and the beginning of the financial period.

IV Equity of the subsidiary at acquisition date.

(Multiple Choice)

4.8/5 (38)

A Ltd holds a 60% interest in B Ltd. On 1 July 2017 B Ltd transferred a depreciable non-current asset to A Ltd at a profit of $5 000. The remaining useful life of the asset at the date of transfer was 4 years and the tax rate is 30%. The impact of the above transaction on the NCI share of profit for the year ended 30 June 2018 is:

(Multiple Choice)

5.0/5 (34)

Ownership interests in a subsidiary entity that do not belong to the parent entity are known as:

(Multiple Choice)

4.7/5 (33)

During the previous year, a partly-owned subsidiary has made a transfer from retained earnings to a general reserve. Which of the following lines would appear in the NCI journal relating to the current year transfer?

(Multiple Choice)

4.8/5 (43)

In respect to the intragroup services provided by a partly-owned subsidiary to the parent, the NCI adjustment required is a debit to NCI of:

(Multiple Choice)

4.7/5 (45)

During the current year, a partly-owned subsidiary has made a transfer from retained earnings to a general reserve. Which of the following lines would appear in the NCI journal relating to the current year transfer?

(Multiple Choice)

4.9/5 (29)

Disclosure of NCI's share of consolidated equity is required in the following financial statements:

(Multiple Choice)

4.9/5 (34)

Jiminez Limited acquired 80% of the shares in Mustang Limited for $180 000. At acquisition date, share capital in Mustang was $100 000 and reserves amounted to $50 000. All assets and liabilities of Mustang were recorded at fair value at acquisition date except buildings which was recorded at $10 000 below fair value. If the company tax rate was 30%, and the partial goodwill method was adopted, the NCI share of equity at the date of acquisition was:

(Multiple Choice)

4.9/5 (35)

Which of the following is not a reason for an entity's preference to have less than 100% ownership interest in some subsidiaries:

(Multiple Choice)

4.7/5 (39)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)