Exam 7: Advanced Option Strategies

Exam 1: Introduction40 Questions

Exam 2: Structure of Options Markets63 Questions

Exam 3: Principles of Option Pricing56 Questions

Exam 4: Option Pricing Models: the Binomial Model60 Questions

Exam 5: Option Pricing Models: the Black-Scholes-Merton Model60 Questions

Exam 6: Basic Option Strategies60 Questions

Exam 7: Advanced Option Strategies60 Questions

Exam 8: Principles of Pricing Forwards,futures and Options on Futures59 Questions

Exam 9: Futures Arbitrage Strategies59 Questions

Exam 10: Forward and Futures Hedging,spread,and Target Strategies60 Questions

Exam 11: Swaps60 Questions

Exam 12: Interest Rate Forwards and Options60 Questions

Exam 13: Advanced Derivatives and Strategies60 Questions

Exam 14: Financial Risk Management Techniques and Appplications62 Questions

Exam 15: Managing Risk in an Organization58 Questions

Select questions type

A call butterfly spread is a bullish strategy that is profitable if stock prices increase.

Free

(True/False)

4.8/5  (32)

(32)

Correct Answer: Verified

Verified

False

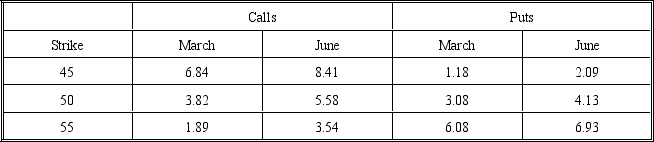

The following prices are available for call and put options on a stock priced at $50.The risk-free rate is 6 percent and the volatility is 0.35.The March options have 90 days remaining and the June options have 180 days remaining.The Black-Scholes model was used to obtain the prices.

Use this information to answer questions 1 through 20.Assume that each transaction consists of one contract (for 100 shares)unless otherwise indicated.

Answer questions 18 through 20 about a long box spread using the June 50 and 55 options.

-What is the net present value of the box spread?

Use this information to answer questions 1 through 20.Assume that each transaction consists of one contract (for 100 shares)unless otherwise indicated.

Answer questions 18 through 20 about a long box spread using the June 50 and 55 options.

-What is the net present value of the box spread?

Free

(Multiple Choice)

4.8/5 (32)

Correct Answer:Verified

D

Early exercise is a disadvantage in which of the following transactions?

Free

(Multiple Choice)

4.8/5 (31)

Correct Answer:Verified

A

The payoffs form a straddle are more like the payoffs from a money spread than a calendar spread.

(True/False)

4.9/5 (33)

Which of the following is the best strategy for an expected fall in the market?

(Multiple Choice)

4.7/5 (31)

The following prices are available for call and put options on a stock priced at $50.The risk-free rate is 6 percent and the volatility is 0.35.The March options have 90 days remaining and the June options have 180 days remaining.The Black-Scholes model was used to obtain the prices.

Use this information to answer questions 1 through 20.Assume that each transaction consists of one contract (for 100 shares)unless otherwise indicated.

Answer questions 12 through 17 about a long straddle constructed using the June 50 options.

-What are the two breakeven stock prices at expiration?

(Multiple Choice)

4.8/5 (34)

The profit from a put bear spread strategy when both options are out of the money is

(Multiple Choice)

4.9/5 (41)

The longer an investor holds a long call butterfly spread position,everything else the same,the greater the distance between the breakeven stock prices.

(True/False)

4.9/5 (30)

If a straddle is closed prior to expiration,the investor can recover some of the time value of either the call or the put but not both.

(True/False)

4.8/5 (35)

The option strategy where the holder of a long position in a stock buys a put with an exercise price lower than the current stock price and sells a call with an exercise price higher than the current stock price is known as

(Multiple Choice)

4.8/5 (35)

The following prices are available for call and put options on a stock priced at $50.The risk-free rate is 6 percent and the volatility is 0.35.The March options have 90 days remaining and the June options have 180 days remaining.The Black-Scholes model was used to obtain the prices.

Use this information to answer questions 1 through 20.Assume that each transaction consists of one contract (for 100 shares)unless otherwise indicated.

For questions 1 through 6,consider a bull money spread using the March 45/50 calls.

-What is the profit if the stock price at expiration is $47?

(Multiple Choice)

4.7/5 (25)

To truly gain from a straddle,an investor must have a better estimate of volatility than everyone else.

(True/False)

4.8/5 (34)

A call bear spread is a strategy for investors who expect stock prices to increase.

(True/False)

4.9/5 (30)

An investor who holds a strap (2 calls and 1 put)believes the market is more likely to go up than down.

(True/False)

4.9/5 (30)

The following prices are available for call and put options on a stock priced at $50.The risk-free rate is 6 percent and the volatility is 0.35.The March options have 90 days remaining and the June options have 180 days remaining.The Black-Scholes model was used to obtain the prices.

Use this information to answer questions 1 through 20.Assume that each transaction consists of one contract (for 100 shares)unless otherwise indicated.

Answer questions 10 and 11 about a calendar spread based on the assumption that stock prices are expected to remain fairly constant. Use the June/March 50 call spread. Assume one contract of each.

-What will be the profit if the spread is held 90 days and the stock price is $45?

(Multiple Choice)

4.7/5 (29)

The risk of early exercise is of no concern to the holder of a long straddle.

(True/False)

4.9/5 (35)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)