Exam 8: Activity-Based Costing

Exam 1: Management Accounting: Information for Creating Value and Managing Resources67 Questions

Exam 2: Management Accounting: Cost Terms and Concepts87 Questions

Exam 3: Cost Behaviour, Cost Drivers and Cost Estimation93 Questions

Exam 4: Product Costing Systems88 Questions

Exam 5: Process Costing and Operation Costing87 Questions

Exam 6: Service Costing91 Questions

Exam 7: A Closer Look at Overhead Costs99 Questions

Exam 8: Activity-Based Costing91 Questions

Exam 9: Budgeting Systems92 Questions

Exam 10: Standard Costs for Control: Direct Material and Direct Labour105 Questions

Exam 11: Standard Costs for Control: Flexible Budgets and Manufacturing Overhead109 Questions

Exam 12: Managing and Reporting Performance102 Questions

Exam 13: Financial Performance Measures and Incentive Schemes93 Questions

Exam 14: Strategic Performance Measurement Systems80 Questions

Exam 15: Managing Suppliers and Customers90 Questions

Exam 16: Managing Costs and Quality92 Questions

Exam 17: Sustainability and Management Accounting76 Questions

Exam 18: Cost Volume Profit Analysis111 Questions

Exam 19: Information for Decisions: Relevant Costs and Benefits116 Questions

Exam 20: Pricing and Product Mix Decisions113 Questions

Exam 21: Information for Capital Expenditure Decisions125 Questions

Select questions type

Twista Manufacturing has the following activities and activity costs per year: Machining ($20 000); Forklifting ($10 000); machine setup ($32 000), and quality inspection ($40 000). The operation starts with setting up the machines; each batch of products requires a different setup. This is followed by machining, where the cost of machining varies directly with the number of machine hours. Forklifts are used to move the work in progress around. Because quality is important, an inspection is carried out for each batch of products.

The following information is also available:

Number of machine hours per year: 20 000 machine hours

Number of forklift moves per year: 500 moves

Number of batches per year: 4000 batches

Each year, Twista Manufacturing produces 5000 units of Product X. These units of Product X require 5000 machine hours, 120 moves and 500 batches to produce. The direct materials and direct labour together cost $15 per unit of Product X.

The total cost for one unit of Product X is:

Free

(Multiple Choice)

4.7/5  (27)

(27)

Correct Answer: Verified

Verified

B

Describe how assigning overhead costs differs under a simple activity-based product costing system from a traditional volume-based costing system.

Free

(Essay)

4.9/5 (35)

Correct Answer:Verified

Under a traditional volume-based system, a predetermined overhead rate based on direct labour hours or some other measure of volume is used to apply overhead to the product. Many manufacturers use direct labour hours assuming that they are closely related to the volume of activity in the factory.

Under a simple activity-based product costing system, overhead is applied in two steps. The first step is to identify significant activities and group costs by these activities into activity cost pools. The second step is to find an activity driver for each pool and apply the costs to products according to their relative use of the activity drivers.

Calculate the cost of processing one sales order if the total activity cost is $1 720 000 p.a., the activity driver is the number of orders received and the annual quantity of the activity driver is

43 000 orders.

Free

(Multiple Choice)

4.9/5 (38)

Correct Answer:Verified

C

Summer Ice Pty Ltd is a manufacturer of a range of ice cream products. The following is a list of activities, costs and quantities of activity drivers for a number of activities that occur in the factory.  Under an activity-based system, what is the activity cost per unit of activity division for packing into containers?

Under an activity-based system, what is the activity cost per unit of activity division for packing into containers?

(Multiple Choice)

4.8/5 (32)

In an activity-based costing system, a bill of activities will include:

(Multiple Choice)

4.9/5 (41)

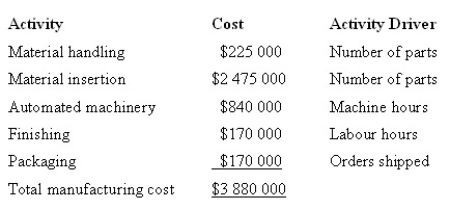

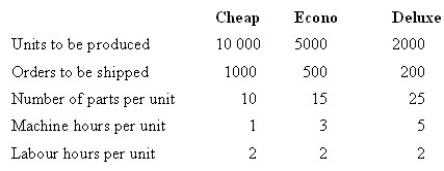

HiTech Products manufactures three types of CD players: Cheap, Econo and Deluxe. HiTech uses an activity-based product costing system. The company has identified five activities. Each activity, its cost and related activity driver are identified below:  The following information pertains to each product line of CD players:

The following information pertains to each product line of CD players:  Under an activity-based product costing system, what is the cost per unit of Cheap?

Under an activity-based product costing system, what is the cost per unit of Cheap?

(Multiple Choice)

4.8/5 (33)

Twista Manufacturing has the following activities and activity costs per year: Machining ($20 000); Forklifting ($10 000); machine setup ($32 000), and quality inspection ($40 000). The operation starts with setting up the machines; each batch of products requires a different setup. This is followed by machining, where the cost of machining varies directly with the number of machine hours. Forklifts are used to move the work in progress around. Because quality is important, an inspection is carried out for each batch of products.

The following information is also available:

Number of machine hours per year: 20 000 machine hours

Number of forklift moves per year: 500 moves

Number of batches per year: 4000 batches

Each year, Twista Manufacturing produces 5000 units of Product X. These units of Product X require 5000 machine hours, 120 moves and 500 batches to produce. The direct materials and direct labour together cost $15 per unit of Product X.

The forklifting costs and machine set up costs allocated to Product X are:

(Multiple Choice)

4.7/5 (31)

When introducing an activity-based costing system which of the following actions are recommended for the changeover to be successful?

(Multiple Choice)

4.8/5 (40)

Calculate the cost per unit for setup for one run of 10 000 units if setup labour is $20 per hour and 10 hours are required to set up.

(Multiple Choice)

4.9/5 (30)

Under an activity-based system where budgeted costs have been used, it is necessary to include the cost of unused capacity, when estimating and reporting profit.

(True/False)

4.7/5 (34)

Consider the following statements. Traditional costing systems can produce distorted product costs if:

i. overheads are driven by non-volume factors.

ii. overheads are a minor part of the product cost.

iii. it fails to recognise non-manufacturing costs as product costs.

Which of the statements is true?

(Multiple Choice)

4.8/5 (40)

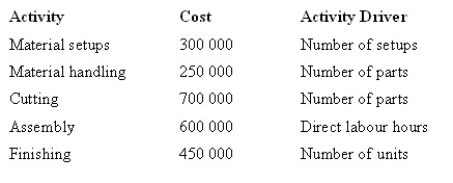

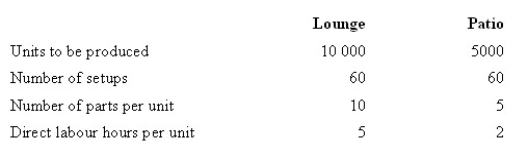

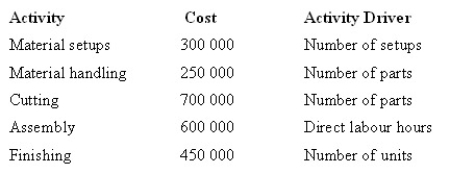

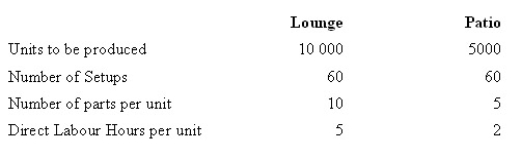

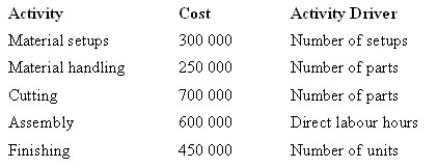

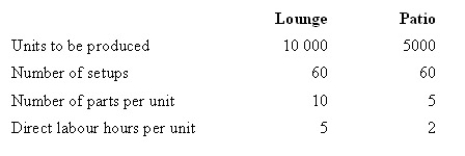

The Pinewood Furniture Company Pty Ltd plans to manufacture two lines of chairs in the coming year-lounge and patio. The company is considering introducing an activity-based costing system. Given below are each activity, its cost and its related activity driver.  The level of activity for the year is:

The level of activity for the year is:  Under an activity-based costing system, what is the activity cost per unit of activity driver for finishing?

Under an activity-based costing system, what is the activity cost per unit of activity driver for finishing?

(Multiple Choice)

4.8/5 (41)

At a recent professional meeting, two accountants discussed product-costing problems in their respective companies. Both accountants are familiar with ABC systems but neither firm uses this method.

Accountant A reported that part of the problem in product costing in his firm is that there are major differences between product lines as to volume of units, utilisation of various activities, quality assurance requirements established by customers and size of the products. Accountant B noted that in her firm, which produces consumer products, all products undergo the same basic production processes and in the same sequence, but in an increasing variety of colours and packaging modes.

Both accountants are worried about the potential distortion of product costs under their traditional product costing systems.

Which accountant should be more concerned about the potential distortion? Explain.

(Essay)

4.7/5 (40)

The Pinewood Furniture Company Pty Ltd plans to manufacture two lines of chairs in the coming year-lounge and patio. The company is considering introducing an activity-based costing system. Given below are each activity, its cost and its related activity driver.  The level of activity for the year is:

The level of activity for the year is:  Under an activity-based costing system, what is the activity cost per unit of activity driver for machine setups?

Under an activity-based costing system, what is the activity cost per unit of activity driver for machine setups?

(Multiple Choice)

4.8/5 (27)

Activity-based costing has the potential to improve the accuracy of product costs, however, it is important for management to understand its limitations. Identify and explain two limitations.

(Essay)

4.9/5 (39)

ABC is a methodology that can be as simple or as complex as the organisation wants it to be.

(True/False)

4.8/5 (39)

Traditional product costing systems result in inaccurate product costs when:

(Multiple Choice)

4.9/5 (41)

Companies are likely to benefit from activity-based costing systems if:

(Multiple Choice)

4.9/5 (39)

The Pinewood Furniture Company Pty Ltd plans to manufacture two lines of chairs in the coming year-lounge and patio. The company is considering introducing an activity-based costing system. Given below are each activity, its cost and its related activity driver.  The level of activity for the year is:

The level of activity for the year is:  Under an activity-based costing system, what is the total cost of patio chairs for the year?

Under an activity-based costing system, what is the total cost of patio chairs for the year?

(Multiple Choice)

4.9/5 (32)

Filters

- Essay(0)

- Multiple Choice(0)

- Short Answer(0)

- True False(0)

- Matching(0)