Multiple Choice

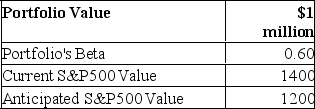

You are given the following information about a portfolio you are to manage.For the long term, you are bullish, but you think the market may fall over the next month.  For a 200-point drop in the S&P 500, by how much does the value of the futures position change?

For a 200-point drop in the S&P 500, by how much does the value of the futures position change?

A) $200,000

B) $50,000

C) $250,000

D) $500,000

Correct Answer:

Verified

Correct Answer:

Verified

Q10: Which one of the following stock index

Q11: Suppose that the risk-free rates in the

Q12: Suppose that the risk-free rates in the

Q13: A swap<br>A) obligates two counterparties to exchange

Q13: You are given the following information about

Q16: If you purchased one S&P 500 Index

Q18: Which one of the following stock index

Q19: In the equation Profits = a +

Q20: If covered interest arbitrage opportunities exist,<br>A)interest rate

Q38: One reason swaps are desirable is that<br>A)