Multiple Choice

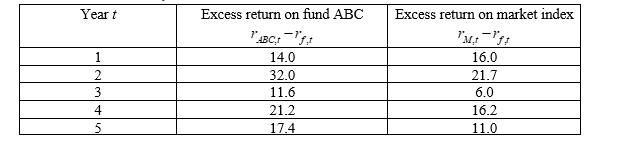

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-Suppose that the unbiased estimator of the standard deviation of the disturbance (s) is 5.1. What is the nearest value to the standard errors of the estimated CAPM alpha (  ) of Fund ABC from question 6?

) of Fund ABC from question 6?

A) 3.5

B) 4.5

C) 5.5

D) 6.5

Correct Answer:

Verified

Correct Answer:

Verified

Q12: Which of the following is NOT correct

Q13: Assuming there are 1000 observations in your

Q14: The method of estimating econometric models which

Q15: Which of these is not a standard

Q16: Which of these is not a reason

Q18: Which of the following is NOT a

Q19: Suppose you have 5-year annual data on

Q20: In a time series regression of

Q21: Two researchers have identical models, data, coefficients

Q22: Consider a bivariate regression model with coefficient