Multiple Choice

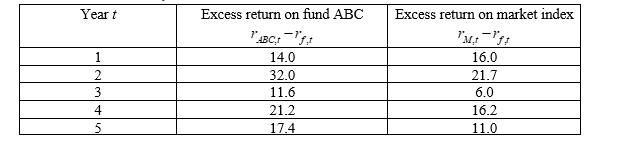

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-The estimators  and

and  determined by OLS will be the Best Linear Unbiased Estimators (BLUE) if which of the following assumptions hold?

determined by OLS will be the Best Linear Unbiased Estimators (BLUE) if which of the following assumptions hold?

(I) The errors have zero mean

(II) The variance of the errors is constant and finite over all values of the independent variable(s)

(III) The errors are linearly independent of one another

(IV) There is no relationship between the error and corresponding independent variables

A) I and II only

B) I, II and III only

C) II, III and IV only

D) I, II, III and IV

Correct Answer:

Verified

Correct Answer:

Verified

Q14: The method of estimating econometric models which

Q15: Which of these is not a standard

Q16: Which of these is not a reason

Q17: Suppose you have 5-year annual data on

Q18: Which of the following is NOT a

Q20: In a time series regression of

Q21: Two researchers have identical models, data, coefficients

Q22: Consider a bivariate regression model with coefficient

Q23: Suppose you have 5-year annual data on

Q24: Which one of the following is NOT