Multiple Choice

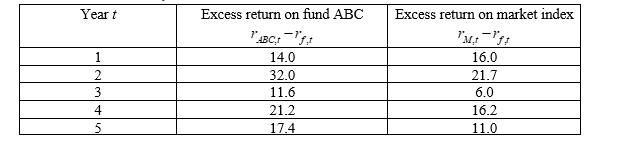

Suppose you have 5-year annual data on the excess returns on a fund manager’s portfolio (“fund ABC”) and the excess returns on a market index (where  is the return on fund ABC,

is the return on fund ABC,  is the risk-free rate and

is the risk-free rate and  is the return on the market index) :

is the return on the market index) :

-What is the most appropriate interpretation of the assumption concerning the regression disturbance terms?

A) The errors are nonlinearly independent of one another

B) The errors are linearly dependent of one another

C) The covariance of the errors is constant and finite over all its values

D) The errors are linearly independent of one another

Correct Answer:

Verified

Correct Answer:

Verified

Q1: Which of the following is a correct

Q3: Which of the following is the most

Q4: Consider an increase in the size of

Q5: Suppose you have calculated the following regression

Q6: What does a positive linear relationship between

Q7: Which of the following statements is correct

Q8: Suppose you have 5-year annual data on

Q9: Regression is concerned with describing and evaluating

Q10: The type I error associated with testing

Q11: What is the relationship, if any, between