Short Answer

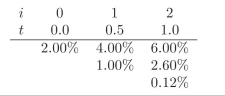

You are given the following interest rate tree. Use it when required in the

exercises.

-Using risk neutral pricing obtain the value for a put option on a 1.5 year zero coupon bond with K = 97.40, maturity at t = 1. Assume that p? = 0.7038 is constant over time.

Correct Answer:

Verified

Correct Answer:

Verified

Related Questions

Q1: Compute the spot rate duration for a

Q3: What is one major drawback from using

Q4: Compute the spot rate duration for a

Q5: You are given the following interest rate

Q6: How realistic is it to speak about

Q7: You are given the following interest rate

Q8: In order to compute the spot rate

Q9: Which of the following prices should be

Q10: What is the difference between risk neutral

Q11: Why do we say that the dynamic