Multiple Choice

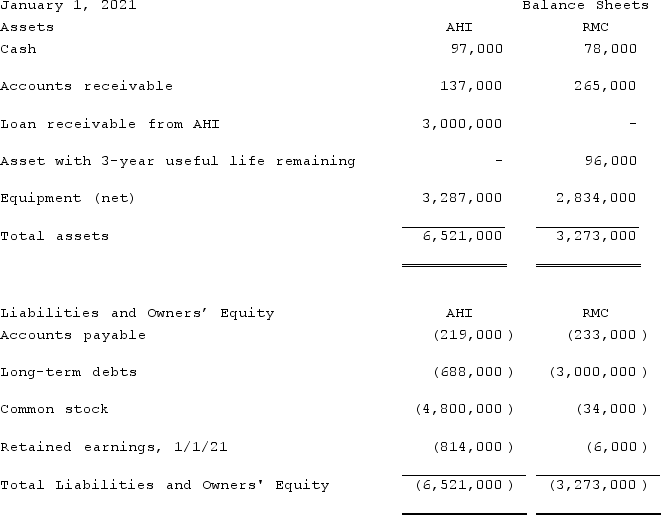

On January 1, 2021, A. Hamilton, Inc. ("AHI") provides a loan for $3,000,000 to Reynolds Manufacturing Corp. ("RMC") . The terms of the loan require payment of the loan no later than January 1, 2026. RMC was in terrible financial condition and would cease operations absent securing a loan. Prior to requesting a loan from AHI, RMC exhausted all other possible avenues for funding. The terms of the loan agreement include provisions that require RMC to provide AHI with the following from January 1, 2021 through January 1, 2026: (i) 6% annual interest on the principal amount of the loan, which reflects a market rate of interest; (ii) 100% participation rights to RMC's profits less $17,000 in a guaranteed annual dividend to RMC's common shareholders; and (iii) complete decision-making authority over RMC's operations and financing decisions.At the end of the term of the loan, AHI is given the right to acquire RMC or, in its discretion, extend the term of the original loan an additional 5 years. At the date the loan was extended to RMC, RMC's common stock had an estimated fair value of $136,000 and a book value of $40,000. The $96,000 difference was attributed to an asset with a 3-year useful life remaining ("Asset") . At January 1, 2021, the balance sheets for AHI and RMC are as follows:  In preparing the consolidation worksheet as of December 31, 2021 for AHI and RMC, which of the following worksheet entry descriptions reflects what AHI should do to consolidate the financial statements?

In preparing the consolidation worksheet as of December 31, 2021 for AHI and RMC, which of the following worksheet entry descriptions reflects what AHI should do to consolidate the financial statements?

A) Consolidation Entry A is recorded to allocate the excess fair value to the noncontrolling interest and record a credit to the Asset in connection with a fair valuation on the date AHI obtains control of RMC as follows:

B) Consolidation Entry P is recorded to eliminate the long-term receivable and debt representing AHI's initial investment in RMC as follows:

C) Consolidation Entry S is recorded to eliminate the interest payment on the loan from RMC to AHI as follows:

D) Consolidation Entry E is recorded to amortize the excess fair value allocation to the Asset over its remaining useful life as follows:

E) Consolidation Entry P is recorded to eliminate the beginning stockholders' equity of the VIE and recognize the 100% equity ownership of the noncontrolling interest as follows:

Correct Answer:

Verified

Correct Answer:

Verified

Q13: Johnson, Inc. owns control over Kaspar, Inc.

Q76: Webb Company purchased 90% of Jones Company

Q82: MacDonald, Inc. owns 80% of the outstanding

Q94: The balance sheets of Butler, Inc. and

Q95: On January 1, 2021, Nichols Company acquired

Q97: On January 1, 2021, Bast Co. had

Q102: Ryan Company purchased 80% of Chase Company

Q104: Knight Co. owned 80% of the common

Q116: How does the creation of a consolidated

Q118: Which of the following statements regarding consolidation