Essay

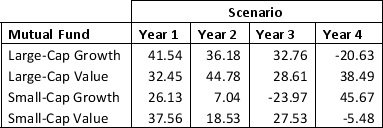

Develop a model that minimizes semivariance for the data given below with a required return of 15 percent. Define a variable ds for each scenario and let ds≥R-Rs with ds ≥ 0. Then make the objective function: Min 14s=14ds2.

Solve the model you developed with a required expected return of at least 15 percent.

Correct Answer:

Verified

Let:

LG = proportion of portfolio invest...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

LG = proportion of portfolio invest...

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q17: A _ is the shadow price of

Q36: A portfolio optimization model used to construct

Q41: Solving nonlinear problems with local optimal solutions

Q43: A feasible solution is a local minimum

Q45: The portfolio variance is the<br>A)sum of the

Q48: Jim is trying to solve a problem

Q51: Consider the EOQ model for multiple products

Q52: An Electrical Company has two manufacturing plants.

Q55: Consider the following data on the returns

Q56: Which of the following conclusions can be