Multiple Choice

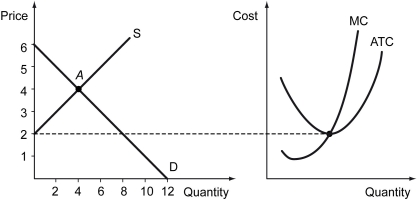

The figure below shows the supply and the demand for a good (left) and the cost curves of an individual firm in this market (right) . Assume that all firms in this market, including the potential entrants, have identical cost curves. Initially, the market is in equilibrium at point A.

-Refer to the figure above.At the equilibrium A,each firm in the market earns ________ and there will be ________.

A) positive economic profit; entries of new firms

B) negative economic profit; exit of existing firms

C) zero economic profit; both entry and exit of firms

D) zero accounting profit; entries of new firms

Correct Answer:

Verified

Correct Answer:

Verified

Q27: Marginal cost is the _.<br>A) cost(s) a

Q28: Sellers in a perfectly competitive market _.<br>A)

Q29: In a perfectly competitive market,firms earn zero

Q30: A production function establishes the relationship between

Q31: The following graph shows the supply curve

Q33: In a perfectly competitive market,sellers _.<br>A) coordinate

Q34: The following table shows the total output,

Q35: Using the notation in the text,AFC equals

Q36: Calculate the price elasticity of supply for

Q37: If firms in a perfectly competitive market