Multiple Choice

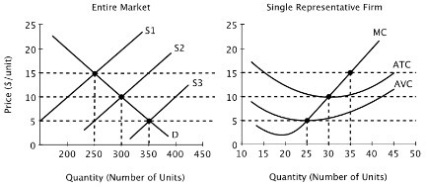

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S1, then in the long run firms will:

If the market supply curve is given by S1, then in the long run firms will:

A) enter the market, leading the market supply curve to shift out to S3.

B) enter the market, leading the market supply curve to shift out to S2.

C) exit the market, leading the market supply curve to shift out to S2.

D) neither enter nor exit the market, so the market supply curve will remain at S1.

Correct Answer:

Verified

Correct Answer:

Verified

Q80: If an individual producer is willing to

Q81: The statement, "If a deal is too

Q82: If the market supply curve does not

Q83: The role that prices play in directing

Q84: Suppose a market is in equilibrium. The

Q86: If you were to start your own

Q87: Consider a perfectly competitive industry in a

Q88: Assume that all firms in this industry

Q89: Suppose the market for coffee is in

Q90: The figure below depicts the short-run market