Multiple Choice

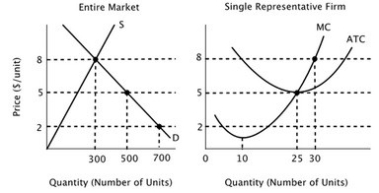

The figure below depicts the short-run market equilibrium in a perfectly competitive market and the cost curves for a representative firm in that market. Assume that all firms in this market have identical cost curves.  Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

Given that the current equilibrium price is $8, what will happen to the number of firms in this market in the long run?

A) The number of firms in the market will not change unless there is a change in either demand or in the cost of production.

B) The number of firms in the market will fall as firms exit the market in response to negative economic profit.

C) It is impossible to determine whether the number of firms in this market will rise or fall.

D) The number of firms in the market will rise as firms enter the market in response to positive economic profit.

Correct Answer:

Verified

Correct Answer:

Verified

Q85: Assume that all firms in this industry

Q86: If you were to start your own

Q87: Consider a perfectly competitive industry in a

Q88: Assume that all firms in this industry

Q89: Suppose the market for coffee is in

Q91: The figure below shows the supply and

Q92: If a firm is earning zero economic

Q93: Suppose a small island nation imports sugar

Q94: The figure below depicts the short-run market

Q95: The fact that price subsidies reduce economic