Multiple Choice

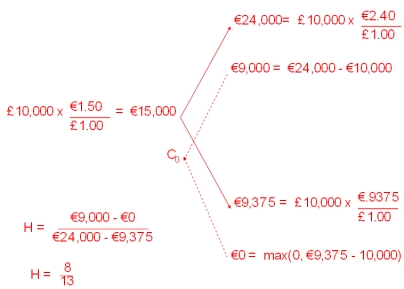

Find the hedge ratio for a call option on £10,000 with a strike price of €12,500. The current exchange rate is €1.50/£1.00 and in the next period the exchange rate can increase to €2.40/£ or decrease to €0.9375/€1.00 .

The current interest rates are i€ = 3% and are i£ = 4%.

Choose the answer closest to yours.

A) 5/9

B) 8/13

C) 2/3

D) 3/8

E) None of the above

Correct Answer:

Verified

Correct Answer:

Verified

Q1: Find the Black-Scholes price of a six-month

Q2: For European currency options written on euro

Q33: Suppose the futures price is below the

Q37: With currency futures options the underlying asset

Q49: Draw the binomial tree for this option.

Q59: Consider the graph of a call option

Q59: Find the hedge ratio for a put

Q60: The current spot exchange rate is $1.55

Q74: Exercise of a currency futures option results

Q85: A European option is different from an