Multiple Choice

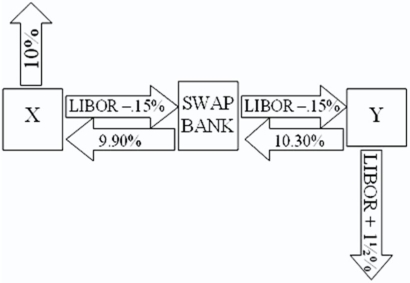

Company X wants to borrow $10,000,000 floating for 5 years; company Y wants to borrow $10,000,000 fixed for 5 years.Their external borrowing opportunities are shown here: A swap bank proposes the following interest only swap:

X will pay the swap bank annual payments on $10,000,000 with the coupon rate of LIBOR ? 0.15 percent; in exchange the swap bank will pay to company X interest payments on $10,000,000 at a fixed rate of 9.90 percent.Y will pay the swap bank interest payments on $10,000,000 at a fixed rate of 10.30 percent and the swap bank will pay Y annual payments on $10,000,000 with the coupon rate of LIBOR ? 0.15 percent.  What is the value of this swap to the swap bank?

What is the value of this swap to the swap bank?

A) The swap bank will lose money on the deal.

B) The swap bank will earn 40 basis points per year on $10,000,000 = $40,000 per year.

C) The swap bank will break even.

D) none of the options

Correct Answer:

Verified

Correct Answer:

Verified

Q84: Company X wants to borrow $10,000,000

Q85: A major risk faced by a swap

Q86: Consider the situation of firm A

Q87: Suppose that the swap that you proposed

Q88: Consider the situation of firm A

Q90: Consider a plain vanilla interest rate swap.Firm

Q91: Consider the situation of firm A

Q92: Company X wants to borrow $10,000,000

Q93: Consider the dollar- and euro-based borrowing

Q94: Company X and company Y have mirror-image