Multiple Choice

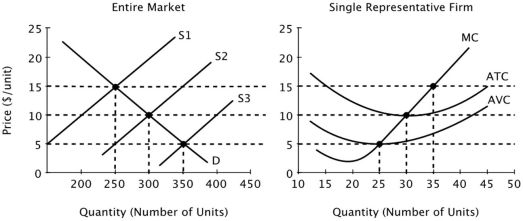

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  If the market supply curve is given by S1, then in the long run firms will:

If the market supply curve is given by S1, then in the long run firms will:

A) enter the market, leading the market supply curve to shift out to S3.

B) enter the market, leading the market supply curve to shift out to S2.

C) exit the market, leading the market supply curve to shift out to S2.

D) neither enter nor exit the market, so the market supply curve will remain at S1.

Correct Answer:

Verified

Correct Answer:

Verified

Q29: Subsidies are most likely to:<br>A)reduce consumer surplus.<br>B)increase

Q35: Pat used to work as an aerobics

Q56: Refer to the table below. Suppose

Q57: Refer to the figure below. <img src="https://d2lvgg3v3hfg70.cloudfront.net/TB3719/.jpg"

Q59: The figure below shows the supply and

Q60: Suppose the production of cotton causes substantial

Q98: In a free market economy, the decisions

Q135: In an industry with free entry and

Q143: A situation is efficient if it is:<br>A)possible

Q157: Suppose the production of cotton causes substantial