Multiple Choice

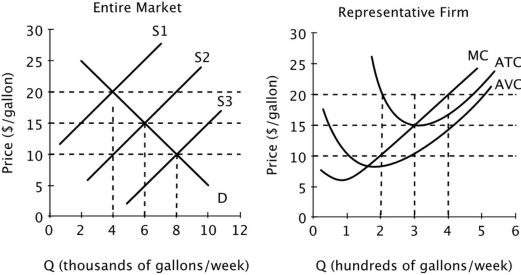

Assume that all firms in this industry have identical cost curves, and that the market is perfectly competitive.  In the long run, the equilibrium price will be _____ per gallon, and each firm's profit-maximizing quantity will be ______ gallons per week.

In the long run, the equilibrium price will be _____ per gallon, and each firm's profit-maximizing quantity will be ______ gallons per week.

A) $20; 4 hundred

B) $15; 6 thousand

C) $15; 3 hundred

D) $20; 4 thousand

Correct Answer:

Verified

Correct Answer:

Verified

Q28: Suppose all firms in a perfectly competitive

Q37: Suppose a market is in equilibrium. The

Q41: Economic profit is equal to:<br>A)accounting profit plus

Q73: Assume that all firms in this industry

Q74: Assume that all firms in this industry

Q75: The figure below shows the supply and

Q79: Refer to the table below. At

Q80: The statement, "If a deal is too

Q83: Suppose a small island nation imports sugar

Q86: If you were to start your own