Multiple Choice

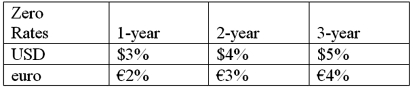

Suppose that you are a swap bank and you notice that interest rates on zero coupon bonds are as shown. Develop the 3-year bid price of a euro swap quoted against flat USD LIBOR.  In other words, what you be willing to pay in euro against receiving USD LIBOR?

In other words, what you be willing to pay in euro against receiving USD LIBOR?

A) 5%

B) 4%

C) 3%

D) 2%

Correct Answer:

Verified

Correct Answer:

Verified

Q30: A major risk faced by a swap

Q31: Consider the dollar- and euro-based borrowing opportunities

Q32: Company X wants to borrow $10,000,000 floating

Q33: Amortizing currency swaps<br>A)the debt service exchanges decrease

Q35: Some of the risks that a swap

Q36: When a swap bank serves as a

Q37: Suppose the quote for a five-year swap

Q38: In the swap market, which position potentially

Q39: Company X wants to borrow $10,000,000 floating

Q84: Explain how firm B could use the