Essay

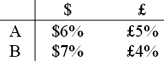

Consider the situation of firm A and firmB. The current exchange rate is $2.00/£ Firm A is a U.S. MNC and wants to borrow £30 million for 2 years. Firm B is a British MNC and wants to borrow $60 million for 2 years. Their borrowing opportunities are as shown, both firms have AAA credit ratings.  The IRP 1-year and 2-year forward exchange rates are

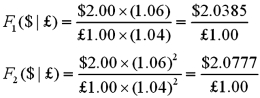

The IRP 1-year and 2-year forward exchange rates are

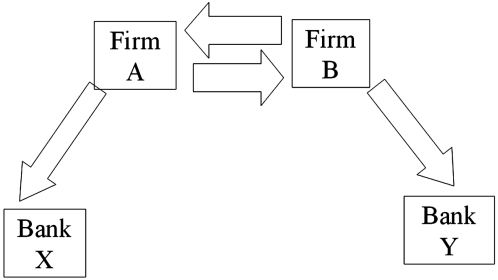

Devise a direct swap for A and B that has no swap bank. Show their external borrowing. Answer the problem in the template provided.

Devise a direct swap for A and B that has no swap bank. Show their external borrowing. Answer the problem in the template provided.

Correct Answer:

Verified

Correct Answer:

Verified

Q3: Floating for floating currency swaps<br>A)the reference rates

Q6: Floating for floating currency swaps<br>A)the reference rates

Q7: In an efficient market without barriers to

Q9: Explain how firm B could use the

Q10: A swap bank<br>A)can act as a broker,

Q11: Consider fixed-for-fixed currency swap. Firm A is

Q12: A swap bank has identified two companies

Q13: Company X wants to borrow $10,000,000 floating

Q25: What are the IRP 1-year and 2-year

Q99: Which combination of the following statements is