Multiple Choice

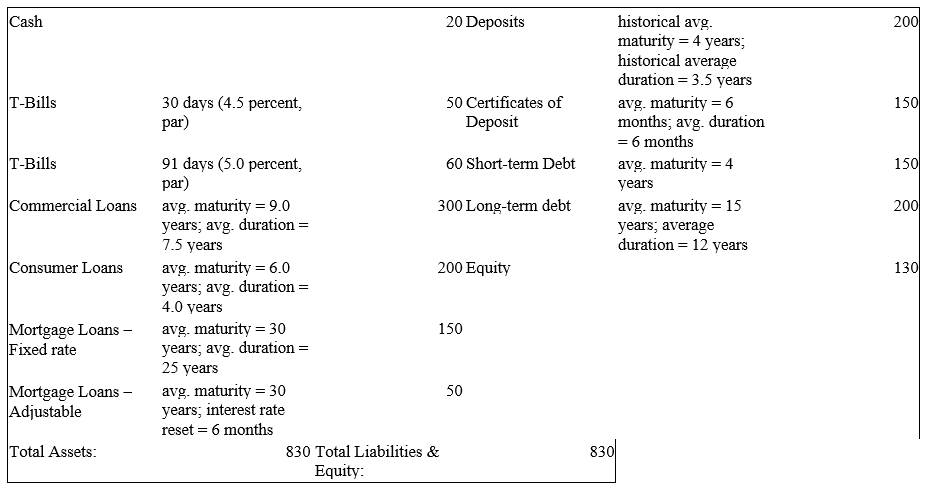

The numbers provided are in millions of dollars and reflect market values:

-What is the leverage-adjusted duration gap of the FI?

A) 3.61 years.

B) 3.74 years.

C) 4.01 years.

D) 4.26 years.

Correct Answer:

Verified

Correct Answer:

Verified

Related Questions

Q10: Duration increases with the maturity of a

Q16: One method of changing the positive leverage

Q62: What is the price of the bond

Q62: A bond is scheduled to mature in

Q64: For a given maturity fixed-income asset, duration

Q64: Why does immunization against interest rate shocks

Q65: Matching the maturities of assets and liabilities

Q71: A $1,000 six-year Eurobond has an 8

Q103: As interest rates rise, the duration of

Q130: The greater is convexity, the more insurance