Multiple Choice

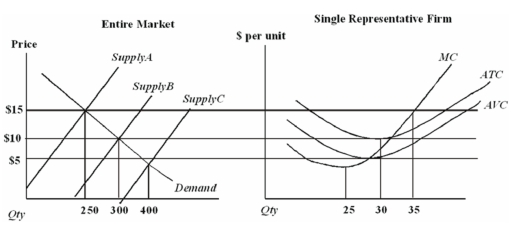

Assume that all firms in this industry have identical cost functions.

When price is $15 in this industry,

A) the industry is in its long run equilibrium.

B) it is because supply has shifted from Supply B to Supply A because firms that were not making a profit left the industry.

C) new firms will be expected to enter.

D) all firms are making zero economic profits.

Correct Answer:

Verified

Correct Answer:

Verified

Q105: A market equilibrium is only efficient when:<br>A)buyers

Q106: Assume that all firms in this industry

Q107: Assume that all firms in this industry

Q108: Daily Supply and Demand: Oranges in Hurricane

Q109: Barriers to entry are _,and one effect

Q110: Suppose that a firm is located along

Q111: An implication of entry and exit in

Q112: Duke is a particularly highly skilled negotiator.The

Q114: Pareto efficiency is a situation in which:<br>A)no

Q115: The statement,"price distributes goods and services to