Multiple Choice

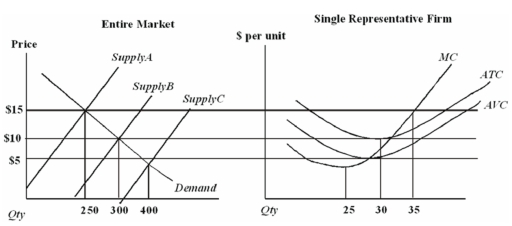

Assume that all firms in this industry have identical cost functions.

When price is $15 in this industry,

A) the industry is in its long run equilibrium.

B) it is because supply has shifted from Supply B to Supply A because firms that were not making a profit left the industry.

C) new firms will be expected to enter.

D) all firms are making zero economic profits.

Correct Answer:

Verified

Correct Answer:

Verified

Q29: Subsidies are most likely to:<br>A)reduce consumer surplus.<br>B)increase

Q40: Assume that all firms in this industry

Q43: Normal profits occur when:<br>A)accounting profits are positive.<br>B)economic

Q45: The following graphs depict a perfectly competitive

Q52: If owners of a business are receiving

Q60: Angelina Jolie's economic rent from starring in

Q61: Ingrid has been waiting for the show

Q65: Chris was the business manager for a

Q82: Economic rent is:<br>A)the amount you pay for

Q84: Adam Smith coined the term "invisible hand"