Multiple Choice

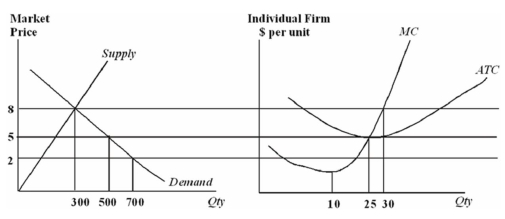

The following graphs depict a perfectly competitive firm and its market.

Assume that all firms in this industry have identical cost functions.

In the long run equilibrium in this market,

A) price will equal $5,and there will be 20 firms in the industry.

B) price will equal $5,and there will be 10 firms in the industry.

C) price will equal $8,and there will be 20 firms in the industry.

D) price will equal $5 and total output will equal 500 units,but there is not enough information to know how many firms there will be.

Correct Answer:

Verified

Correct Answer:

Verified

Q2: An example of an implicit cost is:<br>A)interest

Q25: Economic profits are:<br>A)the same as accounting profits.<br>B)equal

Q29: Subsidies are most likely to:<br>A)reduce consumer surplus.<br>B)increase

Q40: Assume that all firms in this industry

Q41: Assume that all firms in this industry

Q41: The economic theory of business behavior assumes

Q65: Chris was the business manager for a

Q82: Economic rent is:<br>A)the amount you pay for

Q84: Adam Smith coined the term "invisible hand"

Q103: Which of the following is NOT guaranteed