Multiple Choice

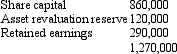

Fan Ltd acquired a 60 per cent interest in Dance Ltd on 1 July 2002 for a cash consideration of $780,000.At that date the fair value of the net assets of Dance Ltd was represented by:  On 30 June 2005 Fan Ltd sold all its shares in Dance Ltd for $880,000.At this date the fair value of the net assets of Dance Ltd was represented by:

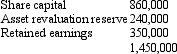

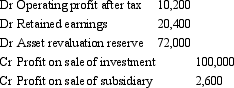

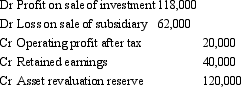

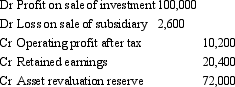

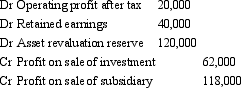

On 30 June 2005 Fan Ltd sold all its shares in Dance Ltd for $880,000.At this date the fair value of the net assets of Dance Ltd was represented by: The retained earnings of $350,000 include operating profit after tax of $20,000 from the current period.Impairment of goodwill was assessed at $5,400,the impairment having been incurred evenly across the last three years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?

The retained earnings of $350,000 include operating profit after tax of $20,000 from the current period.Impairment of goodwill was assessed at $5,400,the impairment having been incurred evenly across the last three years.The investment has not been marked to market during the period that the shares were held.What is the elimination entry required for the consolidated accounts?

A)

B)

C)

D)

E) None of the given answers.

Correct Answer:

Verified

Correct Answer:

Verified

Q1: Dolly Ltd acquired a 60 per cent

Q2: AASB 3 specifies that where a parent

Q3: The following consolidation adjusting journal entries appeared

Q5: Fish Ltd acquired an 80 per cent

Q6: On 1 July 2004,Horse Ltd acquired 80

Q7: The profit or loss on the sale

Q8: Which of the following is not a

Q9: AASB 127 "Consolidated and Separate Financial Statements"

Q10: When additional shares in a subsidiary are

Q11: Spock Ltd acquired a 10 per cent