Essay

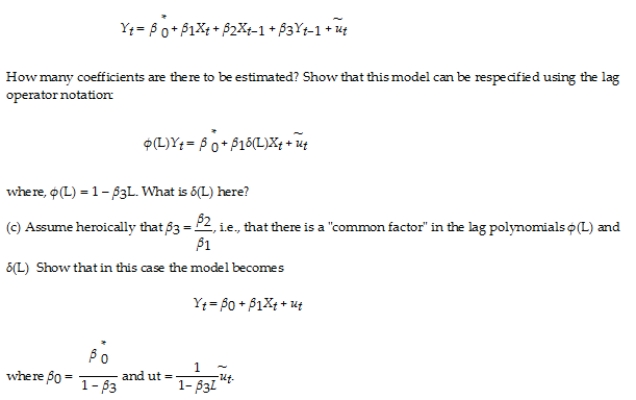

(Requires Appendix material)Your textbook states that in "the distributed lag regression model, the error term ut can be correlated with its lagged values. This autocorrelation arises, because, in time series data, the omitted factors that comprise ut can themselves be serially correlated."

(a)Give an example what the authors have in mind.

(b)Consider the ADL model, where the X's are strictly exogenous, and there is no autocorrelation (and/or heteroskedasticity)in the error term.  (d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

(d)Explain why autocorrelation in this model can be seen as a "simplification," not a "nuisance." Can you use the F-test to test the above hypothesis? Why or why not?

Correct Answer:

Verified

(a)Taking the textbook example of the pe...View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Correct Answer:

Verified

View Answer

Unlock this answer now

Get Access to more Verified Answers free of charge

Q9: Quasi differences in Y<sub>t</sub> are defined as<br>A)Y<sub>t</sub>

Q10: Sensitivity analysis of the results may include

Q11: To estimate dynamic causal effects, your textbook

Q12: A seasonal binary (or indicator or dummy)variable,

Q13: The long-run cumulative dynamic multiplier<br>A)cannot be calculated

Q15: A model that attracted quite a bit

Q16: In time series data, it is useful

Q17: Autocorrelation of the error terms<br>A)makes it impossible

Q18: You are hired to forecast the unemployment

Q19: Given the relationship between the two variables,