Multiple Choice

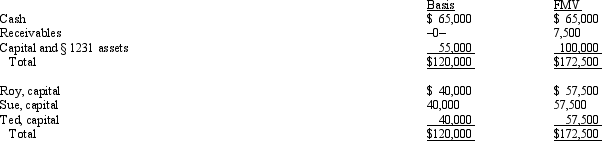

The December 31, 2011, balance sheet of the RST General Partnership reads as follows.  The partners share equally in partnership capital, income, gain, loss, deduction and credit. Ted's adjusted basis for his partnership interest is $40,000. On December 31, 2011, he retires from the partnership, receiving a $60,000 cash payment in liquidation of his interest. The partnership agreement states that $2,500 of the payment is for goodwill. Which of the following statements about this distribution is false?

The partners share equally in partnership capital, income, gain, loss, deduction and credit. Ted's adjusted basis for his partnership interest is $40,000. On December 31, 2011, he retires from the partnership, receiving a $60,000 cash payment in liquidation of his interest. The partnership agreement states that $2,500 of the payment is for goodwill. Which of the following statements about this distribution is false?

A) If capital is NOT a material income-producing factor to the partnership, the § 736(a) payment will be $2,500.

B) If capital IS a material income-producing factor, the entire $60,000 payment will be a § 736(b) property payment.

C) The payment for Ted's share of goodwill will create $2,500 of ordinary income to him.

D) The partnership can deduct any amount that is a § 736(a) payment because it will be determined without regard to partnership profits.

E) All statements are false.

Correct Answer:

Verified

Correct Answer:

Verified

Q18: In the year a donor gives a

Q57: Nicholas is a 25% owner in the

Q85: At the beginning of the year, Elsie's

Q86: The Crimson Partnership is a service provider.

Q88: Partner Jordan received a distribution of $80,000

Q92: Normally a distribution of property from a

Q92: For income tax purposes, proportionate and disproportionate

Q94: In a proportionate liquidating distribution in which

Q95: Anthony's basis in the WAM Partnership interest

Q110: Nick sells his 25% interest in the